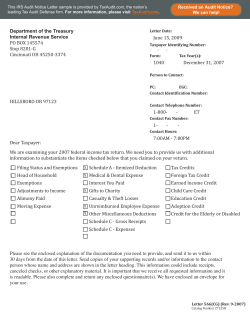

HOW TO FACE AUDIT UNDER CENTRAL EXCISE AND SERVICE TAX?