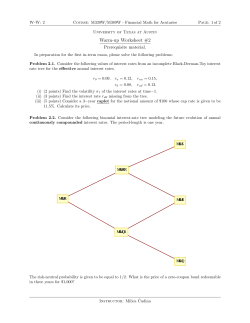

Lecture 4

c 2015 Juliusz Jablecki: Equity and Fixed Income Equity and Fixed Income Juliusz Jabłecki Banking, Finance and Accounting Dept. Faculty of Economic Sciences University of Warsaw [email protected] and Head of Monetary Policy Analysis Team Economic Institute, National Bank of Poland 1 c 2015 Juliusz Jablecki: Equity and Fixed Income Lecture 4: VIX and volatility derivatives Plain vanilla equity options, which we have discussed so far, allow investors to speculate on the movement in the price of the underlying stock. In this lecture we introduce an important new class of equity derivatives, in which investors speculate not on the price of the underlying instrument, but its volatility. In this lecture we will try to find answers to the following questions: • what is volatility? • what’s the rationale for investing in volatility (a priori)? • how to invest in volatility? • does it make sense to invest in volatility (ex post)? 2 c 2015 Juliusz Jablecki: Equity and Fixed Income What is volatility? We need to start with a philosophical observation. Unlike stock price, the volatility of stock price is unobservable – what we observe is the movement of prices with the flow of time. Volatility is merely a statistical metric by which we choose to describe this movement. And since volatility has to be estimated, this opens a Pandora’s box of nontrivial statistical dilemmas. Fortunately, in this lecture we take a market-oriented (rather than econometric) point of view and will associate volatility with one of two things: • realized volatility, i.e. annualized standard deviation of log-returns on a given stock/index in a certain time frame (calculated under the assumption of a zero mean) v u u u u u t 252 N Si+1 2 X ln σ= N − 1 i=1 Si • implied volatility, i.e. a parameter Σ(K, T ), which plugged into the Black-Scholes formula for the value of a European call option with strike K and expiration time T yields the market value of that option. 3 c 2015 Juliusz Jablecki: Equity and Fixed Income The difference between realized and implied volatility 4 c 2015 Juliusz Jablecki: Equity and Fixed Income Realized volatility is a backward-looking measure (historical) while implied volatility is forward-looking.Implied volatility is essentially the price one has to pay for gaining implicit or explicit exposure to volatility of a given index that will materialize over a certain future time horizon. This is clear if we consider a trader who writes a call option C on an underlying S with implied volatility Σ and hedges away the underlying (“delta”) risk by going long (∂C/∂S) units of the underlying instrument (typically a futures contract). If we strip the option off of its linear componet, we become long a quadratic payoff: 5 c 2015 Juliusz Jablecki: Equity and Fixed Income To understand this better Taylor-expand C(S, t): ∂C 1 ∂ 2C ∂C 2 +... (∆S) C (S + ∆S, t + ∆t) = C(S, t)+ ∆S+ ∆t+ ∂S ∂t 2 ∂S 2 Hence the profit-and-loss, P &L, on the delta hedged option is ∂C ∂C 1 ∂ 2C 2, P &L = d −C(S, t) + S ≈ − ∆t − (∆S) ∂S ∂t 2 ∂S 2 Since the option is written at Black-Scholes implied volatility Σ, it also satisfies the Black-Scholes differential equation, i.e.: ∂C ∂C 1 2 2 ∂ 2C + rS + Σ S = rC. 2 ∂t ∂S 2 ∂S Assuming that the risk free rate r is close to zero: ∂C 1 2 2 ∂ 2C Σ S ≈− , 2 ∂S 2 ∂t So that ∆S 2 1 2 2 P &L ≈ ΓS Σ ∆t − 2 S . 6 Reason #1: Volatility is negatively correlated with equity returns. c 2015 Juliusz Jablecki: Equity and Fixed Income Why invest in volatility? 7 c 2015 Juliusz Jablecki: Equity and Fixed Income Reason #2:Volatility tends to increase with market uncertainty. 8 c 2015 Juliusz Jablecki: Equity and Fixed Income Reason #3: Equity volatility is negatively correlated with credit returns (recall the Merton model!) 9 c 2015 Juliusz Jablecki: Equity and Fixed Income Hence, there are two typical reasons for investing in volatility • Expressing views on the most likely future path of volatility. This can be either a relatively simple strategy of betting on the future value of (expected) volatility by going outright long or short volatility, or a more sophisticated trade based on the whole term structure of volatility (e.g. going short near-term volatility and long medium-term volatility), as well as a relative value trade between implied/realized vol. • Risk mitigation. Many categories of investors hold positions that are explicitly or implicitly short volatility (e.g. bond and equity investors are short volatility because of the negative correlation between equity and credit returns and volatility). 10 c 2015 Juliusz Jablecki: Equity and Fixed Income How to invest in volatility? 11 c 2015 Juliusz Jablecki: Equity and Fixed Income Instrument 1: Variance swaps Variance swaps are bets on future realized volatility. The payoff of a variance swap at maturity can be expressed as: V = N otional × (RV 2 − Σ2) s 2 n ln (S /S ) is the realized volatility, i.e. where RV = N t t−1 t=1 n standard deviation of log-returns (with an assumed zero mean) during the n days until maturity, N is the number of trading days, and Σ is the strike value of the swap. What is the fair strike Σ of a variance swap? P V = 0 ⇐⇒ Σ2 = E RV 2 ! It turns out that: Σ2 ≈ 2erT T M C(T, Ki) X P (T, Ki ) X N ∆K + ∆K i i , 2 2 Ki Ki i=1 i=N +1 where K1 < ... < KN < ... < KM are the successive strikes of N puts worth P (T, Ki) and M calls worth C(T, Ki). 12 c 2015 Juliusz Jablecki: Equity and Fixed Income Instrument 2: Implied volatility (VIX) futures Implied volatility futures allow betting on future implied volatility of a stock or, more commonly, an index. But implied volatility of which option? CBOE has made investors’ lives easier by introducing an implied volatility index called VIX which is defined as the strike of a one month variance swap: V IX = v u u u u u u t 2erT T N P (T, Ki ) M C(T, Ki) X + ∆K + ∆K i i 2 2 Ki Ki i=1 i=N +1 X 13 c 2015 Juliusz Jablecki: Equity and Fixed Income VIX represents the market’s expectation of volatility over the next month. VIX futures are futures contracts on the VIX. E.g. on 17 April 2015 the price of May 2015 VIX futures expiring on May 20, 2015 was 15.685. This means that the market was pricing the volatility over the period May 20 to June 17, 2015 at 15.685%. 14 c 2015 Juliusz Jablecki: Equity and Fixed Income Instrument 3: VIX options Two years after the launch of VIX futures, in February 2006, plain vanilla call and put options on the VIX index began trading on the CBOE. Options are European style – i.e. can be exercised only on the expiration date – and settle to the T -day opening quotation of the VIX. On the settlement date T the payoffs are: call: $100×max(0, V IXT −K), put: $100×max(0, K−V IXT ) where K is the strike price quoted in volatility points. The contracts are structured so that the value of one volatility point is $100. Although there are currently only 6 listed expiries for VIX options, corresponding to six following months (versus 8 expiries for VIX futures), VIX options are the second most liquid group of option contracts listed on CBOE, slowly approaching SPX options in terms of open interest. 15 c 2015 Juliusz Jablecki: Equity and Fixed Income The benefits of investing in volatility To analyze the benefits of investing in volatility consider the effects of adding volatility exposure to a benchmark portfolio of stocks and bonds. Volatility exposure is defined in three different ways: (i) a long position in implied volatility; (ii) short position in realized volatility; and (iii) a combination of a short position in realized volatility and a long position in implied volatility. The analysis uses daily data for the period 2003-2013. Benchmark portfolio (40% equity + 60% bonds) 16 c 2015 Juliusz Jablecki: Equity and Fixed Income Long volatility strategy: adding VIX futures to benchmark 17 c 2015 Juliusz Jablecki: Equity and Fixed Income Short realized volatility strategy: adding variance swap to benchmark 18 Return Std. dev Sharpe ratio 99% VaR 1. Benchmark 0.068 0.080 0.602 -0.307 2. Long vol 0.092 0.073 0.993 -0.169 3. Short vol 0.100 0.107 0.748 -0.440 4. Long/short vol 0.147 0.080 1.586 -0.116 Adding any kind of volaility exposure improves the performance of the benchmark portfolio on a risk-adjusted basis. However, the most beneficial strategy – in the sense of maximizing return and minizming value-at-risk – combines exposure to both implied volatility and realized volatility. c 2015 Juliusz Jablecki: Equity and Fixed Income Performance of the strategies: 19 c 2015 Juliusz Jablecki: Equity and Fixed Income Exam-like problems 1. Please explain the difference between implied and realized volatility. 2. Please list and briefly describe the main volatility derivatives. 3. Please list the main reasons for investing in volatility. 4. Explain why a delta-hedged option contains exposure to volatility. 20

© Copyright 2026