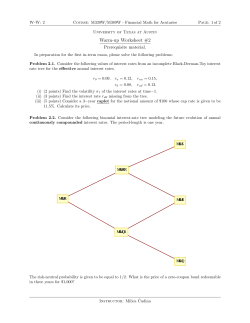

Paper - Erik Lehr

Modeling High-Frequency Returns: Empirical Evidence Using Google and PepsiCo Erik James Lehr Econ 589 Abstract In recent years, the volume and frequency of trading in equity markets has increased dramatically. As a result of this, along with the computerization of trading, researchers now have access to tick-by-tick data, with the trade time accurate up to the millisecond. This wealth of information has clear benefits for research, but also brings new problems, including microstructure issues that can bias estimates or cause data to be inaccurate. This paper will discuss ways to avoid these pitfalls in modeling highfrequency data by cleaning data and using various sampling frequencies, and then demonstrate by modeling return data from Google and Pepsico stocks with simple ARCH and GARCH models to estimate conditional return volatility. 1 I: Introduction Over the past several decades, trading in equity markets has increased exponentially. In January of 1990, about 181 million shares of companies in the Dow Jones Industrial Average (DJIA) were traded. By March 2009, traded volume on the DJIA was over 9 billion1. With this massive increase in volume, the frequency of trades has sharply risen as well, leading to a group of investors who trade with the specific intent of using the higher frequency per se to capture profits. As a result, it is not unusual for frequently traded stocks to be traded multiple times per second. This is understandably beneficial for financial research, as much more data than was previously available can now be used in the modeling of prices and returns. However, this additional data does not come without some negatives, the most prevalent being market microstructure issues. The purpose of this essay is to discuss these issues, and address possible ways to ameliorate negative effects they may have, and then demonstrate possible modeling techniques for this type of data. In this paper I used the Trades and Quotes (TAQ) database to download one month of tick data from Google and PepsiCo. These data are imported into the R programming language and cleaned using the RTAQ package. The cleaned price data are then converted into return data, and sampled at various frequencies. This return data are then moved to EViews, and modeled using basic ARCH and GARCH models in order to get a more accurate estimate of conditional volatility. The estimated conditional volatility is then compared to the absolute returns. The remainder of the paper is organized as follows: the next section presents some theoretical background of high-frequency modeling and market microstructure, as well as discussing relevant literature. Section III gives a description of the data used, and describes the process of cleaning the data. Section IV first tests some assumptions of classical finance theory, and then shows the results of the data modeling, and Section V concludes. II: Background and market microstructure discussion Market microstructure is defined as “the area of finance that is concerned with the process by which investors’ latent demands are ultimately translated into transactions.”2 In other words, microstructure involves analysis of how trades actually take place, and the issues related to this process. When dealing 1 2 Source: http://finance.yahoo.com Madhavan, A., 2000. “Market microstructure: A survey.” Journal of Financial Markets 3, 205–258. 2 with high-frequency data, the sheer number of trades can amplify some of the problems relating to microstructure. Thus, extra steps must be taken by researchers to ensure that the data used is valid. Some of the problems are from incorrect or nonsensical data, such as an incorrectly entered price, a price equal to zero, a price or spread well outside of the normal range for that asset at that particular time, or a corrected or abnormal trade. Other microstructure issues can be more systemic, such as different prices due to an asset being traded on different exchanges, or multiple trades occurring with identical timestamps (though this may become less of a problem with the new millisecond TAQ data). Similarly, measurement can be a problem with non-synchronous data, where a trade does not occur every single second. This can be problematic as it leads to an uneven time series of data, making modeling difficult. Even if all the above factors are dealt with, tick data is still susceptible to bid-ask bounce, or the price appearing to bounce around depending on whether the trade recorded was a purchase or a sale (meaning by the investor, as opposed to the market maker). A market maker will buy at the bid price, and sell at the ask price, which will invariably be higher. This difference is known as the bid-ask spread, and trading the spread is how market makers earn money. Unfortunately, this difference in prices of the asset depending on who bought and sold it causes measured volatility to diverge. Thus, in order to accurately model high-frequency data, these complications must be addressed. In cleaning my data, I follow the approach of Barndorff-Nielsen et al. (2008)3, which will be discussed further in the next section. In order to eliminate the effects of bid-ask bounce, the data must be sampled less frequently. Andersen and Bollerslev (1998)4 suggest sampling every 5 minutes, and show that doing so is nearly always more than sufficient to stabilize volatility measurements. This less frequent sampling also eliminates the problem of non-synchronous return data in any frequently traded asset.5 Following this approach, I sample both at 5 and 10 minute intervals, and compare the results. 3 Barndorff-Nielsen, O. E., Hansen, P. R., Lunde, A., Shephard, N., 2009. “Realised kernels in practice: Trades and quotes.” Econometrics Journal 12, 1_33. 4 Andersen, T.G., and Bollerslev, T. (1998), “Answering the Skeptics: Yes, Standard Volatility Models Do Provide Accurate Forecasts,” International Economic Review, 39, 885-905. 5 The obvious downside of this method is that it does throw away large amounts of data, and there are methods to incorporate all available data (e.g. Ait-Sahalia, Mykland, and Zhang (2005)), but those are outside the scope of this paper. 3 Once the data have been cleaned and sampled, I can proceed to modeling and estimation. When analyzing return data, perhaps the most important statistic measured is volatility6. Volatility is used in nearly all types of asset pricing and analysis, from simple mean-variance analysis and portfolio theory to value-at-risk or the mathematically intense Black-Sholes option pricing model. However, standard methods for calculating volatility can give misleading results, depending on the process that is followed by return data. For example, simple least squares regression of return data assumes both non-serially correlated data and constant variance (i.e. no heteroskedasticity). Neither of these assumptions holds in typical return data, and thus normal OLS estimates will be incorrect. With respect to volatility in particular, most asset returns display volatility clustering, meaning that a large change in returns is likely to be followed by another large change, and similarly with small changes. Perhaps the most widely used technique to account for this non-constant volatility is Robert Engle’s ARCH/GARCH framework. These conditional heteroskedasticity models allow the variance of the error term of the regression to follow an autoregressive process (as well as a moving process in the case of GARCH), accounting for empirical properties like fat-tailed error terms and volatility clustering. While many extensions have been made to these workhorse models (e.g. IGARCH, PGARCH, TGARCH), Hansen and Lunde (2001)7 show even the most complicated models do not significantly outperform a GARCH(1,1) model. With this in mind, I will use simple ARCH and GARCH models to estimate conditional volatility. Next, I will discuss the data used and describe in depth the cleaning process. III: Data In this study I used one month worth of tick data for Google and PepsiCo. The sample covered 20 days, from May 3 to May 28 of 20108. I downloaded the data from the TAQ database using the Wharton Research Data Services (WRDS) website. Next, I imported the data into R using the RTAQ package written by Jonathan Cornelissen and Kris Boudt. As mentioned above, I followed the cleaning procedure used by Barndorff-Nielsen, et al., addressing first the trades, followed by the quotes, and then merging the data. First, all trades and quotes outside of normal trading hours (9:30 AM - 4:00 PM EST) were eliminated. Next, any data point with a price equal to zero was removed. To avoid apparent price differences due to trading on various exchanges, only trades or quote from the most common exchange 6 Volatility in finance can be measured as either variance and standard deviation, with the latter being somewhat more common among practitioners. 7 Hansen, P. R. and Lunde, A. (2001), “A comparison of volatility models: Does anything beat a GARCH(1,1)?”, Working Paper Series No. 84, Aarhus School of Business, Centre for Analytical Finance, 1-41. 8 May 31 was technically a weekday, but markets were not open due to the Memorial Day holiday. 4 were retained (NASDAQ in the case of Google, and NYSE for Pepsi). When multiple trades or multiple quotes had the same time stamp, these observations were merged. For trades specifically, if any trade had an abnormal sale condition, or a corrected trade, it was deleted. For quotes, any quote with a negative bid-ask spread or with a spread that was much too large given the median spread for that day was eliminated as well. Finally, trades and quotes data were matched using the standard adjustment of matching the quotes to trades 2 seconds behind them (as quotes are registered faster than trades). Finally, with the TAQ data cleaned and matched, I was able to sample at different frequencies. The more infrequent the sampling, the smoother the data series appears, as can be seen using the price data for May 3rd for each asset. First, I graph the price of Pepsi using tick data: 65.0 65.2 65.4 65.6 65.8 66.0 Pepsi May 03 09:30:43 May 03 11:45:07 May 03 14:00:20 As can be seen from the above plot, there are numerous jumps at very small intervals over the course of the day, representing the movement caused by bid-ask bounce. This effect gives the price data a much 5 more choppy appearance than is actually representative of the change in prices. Compare this to the same data sample at 5 and 10 minute intervals: 65.0 65.2 65.4 65.6 65.8 66.0 Pepsi_5Min May 03 09:35 May 03 11:30 May 03 13:15 6 May 03 15:00 65.2 65.4 65.6 65.8 66.0 Pepsi_10Min May 03 09:40 May 03 11:20 May 03 13:00 May 03 14:50 The localized spots of volatility have been smoothed away, giving a more accurate representation of the path followed by the stock price. Similarly with Google, comparing the tick-by-tick prices to the 5 and 10 minute price data: 7 526 528 530 532 Google May 03 09:30:01 May 03 11:45:02 May 03 14:00:02 As with Pepsi, we notice a large amount of volatility over very short periods of time, giving the appearance of a price that experiences large jumps over small intervals. This effect is even more evident in the price of Google, as the bid-ask spread is larger due to a significantly higher stock price (at the time covered in this analysis, Google was trading at a price over 8 times the price of Pepsi). Once again, this effect can be smoothed away through less frequent sampling, as is shown in the following two graphs. 8 527 528 529 530 531 532 Google_5Min May 03 09:35 May 03 11:30 May 03 13:15 May 03 15:00 527 528 529 530 531 532 Google_10Min May 03 09:40 May 03 11:20 May 03 13:00 9 May 03 14:50 The next step is to move the cleaned data into EViews, where it can be modeled using the methods described above. IV. Modeling and estimation of volatility Now that the data have been cleaned, it can be modeled without having to account for possible biases caused by the market microstructure issues described above. However, before I begin model estimation, it is informative to make a quick detour and test a few assumptions of classical finance theory, particularly those of normally distributed returns as well as the Efficient Market Hypothesis9 (EMH). First, I plot the Pepsi returns in a histogram to see if the distribution appears to approximate a normal distribution10: PEP_5MIN 800 700 Frequency 600 500 400 300 200 100 0 -.04 -.03 -.02 -.01 .00 .01 .02 .03 The return distribution is very clearly not normal, with an extremely skinny center, and accordingly fat tails. To further confirm this non-normality, I use a quantile-quantile plot: 9 Fama, Eugene F. (1970). “Efficient Capital Markets: A Review of Theory and Empirical Work.” Journal of Finance XXV, no. 2 . 10 I use the returns sampled at 5 minutes for this analysis, as the sheer number of returns in the tick-by-tick data makes the graphs somewhat unreadable. 10 .008 .006 Quantiles of Normal .004 .002 .000 -.002 -.004 -.006 -.008 -.04 -.03 -.02 -.01 .00 .01 .02 .03 Quantiles of PEP_5MIN If the returns followed a normal distribution, the points on the plot should closely follow the line in the middle of the graph, which they obviously do not. There appear to be far too many outliers, both positive and negative, for us to conclude that this process is approximately normal. To put a final nail in the normal distribution coffin, I calculate the Jarque-Bera statistic. The J-B stat, which should be at or around 0 for normally distributed data, is 483171.5. Having resoundingly rejected normality of returns11, I now can test market efficiency. Market efficiency implies that asset prices (and therefore asset returns) are inherently unforecastable. Any new market information is instantly factored into the price of a security, thus no trader should be able to consistently make money by trading off public information. This conclusion essentially marginalizes fields like fundamental and technical analysis, so naturally there have been numerous tests of this hypothesis. The test I will be using is a variance ratio test. If markets are efficient, then return data should follow a random walk12, meaning the expectation of the price next period is equal to the price this period, and any change in price is from an unpredictable noise process. In its least restrictive form, the Random Walk hypothesis states: = + 11 (1) As an aside, it is important to note that returns tend to display aggregated normality, meaning the longer the sample period, the more likely returns are to be normal. My sample period is extremely short, and the return data is (appropriately) extremely non-normal. 12 Or more accurately, a martingale process. 11 Where rt represents the difference of logged prices, µ is the mean of returns, and εt is the random noise process, where observations of εt are uncorrelated across time. Using a variance ratio test13 I can estimate the ratio of the variance of two compounded returns q periods apart to q times the variance of a one-period return. This is far easier to understand in equation form: = − = ∗ ∗ (2) The VR test then calculates the value of VR(q) – 1, which is distributed N(0, 1) under the null hypothesis of returns following a martingale process. I perform this test on the Pepsi data: Null Hypothesis: PEP_5MIN is a martingale Date: 10/03/11 Time: 16:03 Sample: 1 1600 Included observations: 1559 (after adjustments) Heteroskedasticity robust standard error estimates User-specified lags: 2 4 8 16 Joint Tests Value df Probability Max |z| (at period 2)* 2.869702 1559 0.0163 As can be seen from the above table, the VR test returns a value of 2.8697, meaning I am able to reject the Random Walk hypothesis for Pepsi returns at the 5% level. Thus I am able to conclude that intraday Pepsi returns are non-normal, and do not follow a martingale process, which is somewhat at odds with classical finance theory. Next, I perform these same tests on Google return data. First, I again test normality with a histogram and QQ-plot: 13 Lo, A. W. and MacKinlay, A. C. (1988) “Stock market prices do not follow random walks: evidence from a simple specification test,” Review of Financial Studies, 1(1), 41-6 12 GOOG_5MIN 700 600 Frequency 500 400 300 200 100 0 -.03 -.02 -.01 .00 .01 .02 .03 .04 .05 .0100 .0075 Quantiles of Normal .0050 .0025 .0000 -.0025 -.0050 -.0075 -.0100 -.03 -.02 -.01 .00 .01 .02 .03 .04 .05 Quantiles of GOOG_5MIN As we saw with Pepsi earlier, Google returns are very clearly not normally distributed, though unlike before they seem to be somewhat skewed to the right. The Jarque-Bera statistic is 320218.6, further confirming the non-normality of the data. Next, I perform a variance ratio test: 13 Null Hypothesis: GOOG_5MIN is a martingale Date: 10/04/11 Time: 12:26 Sample: 1 1600 Included observations: 1568 (after adjustments) Heteroskedasticity robust standard error estimates User-specified lags: 2 4 8 16 Joint Tests Value df Probability Max |z| (at period 4)* 3.290357 1568 0.0040 This time, the value of the test is even higher, and we are able to reject the Random Walk hypothesis at the 1% level. Thus, like Pepsi, Google data is non-normally distributed, and the returns do not follow a random walk. Next, I proceed to model estimation14. The two types of models I will be testing are the ARCH(1) and GARCH(1,1). The choice for ARCH/GARCH terms may seem simplistic, but higher order terms in each model result in a poorer fit using the Akaike and Schwarz information criterion. First, I run each model on the Google data sampled at 5 minute intervals, and graph estimates for conditional volatility(standard deviation in this case)15: 14 To conserve space, I will only analyze Google in this section, but all the same graphs for Pepsi will be included in the appendix. The results of that analysis are nearly identical to those with Google in terms of the conclusions drawn in this essay. 15 As the focus of this paper is more on the cleaning and sampling of high-frequency data than model comparison, I will not spend much time describing the results of the model estimation beyond a comparison of conditional volatility graphs. 14 ARCH(1): .024 .020 .016 .012 .008 .004 .000 250 500 750 1000 1250 1500 1250 1500 Conditional standard deviation GARCH(1,1): .024 .020 .016 .012 .008 .004 .000 250 500 750 1000 Conditional standard deviation To see the effect of these models on volatility estimation, compare these graphs to that of absolute returns: 15 AGOOG_5MIN .05 .04 .03 .02 .01 .00 250 500 750 1000 1250 1500 As is instantly evident from a comparison of the graphs, the conditional volatility estimates from the ARCH and GARCH models are far smoother than the absolute returns. Next, I run the same tests with the Google data sampled at a 10 minute frequency. ARCH(1): .024 .020 .016 .012 .008 .004 .000 100 200 300 400 500 Conditional standard deviation 16 600 700 GARCH(1,1): .030 .025 .020 .015 .010 .005 .000 100 200 300 400 500 600 700 Conditional standard deviation Again, compare these conditional volatility estimates to absolute returns: AGOOG_10MIN .05 .04 .03 .02 .01 .00 100 200 300 400 500 600 700 800 As before, the model estimates are far smoother than the absolute returns. However, it is interesting to note that their does not appear to be much difference in the conditional volatility graphs of returns 17 sampled at 5 and 10 minutes. The implication of this is that the conditional volatility settles down at or before 5 minute intervals, meaning the market microstructure effects discussed above are no longer problematic at that sampling frequency. To get a better idea of these microstructure effects, I also estimated the ARCH and GARCH models on the cleaned tick data. ARCH(1): .020 .016 .012 .008 .004 .000 10000 20000 30000 40000 50000 Conditional standard deviation 18 60000 70000 GARCH(1,1): .028 .024 .020 .016 .012 .008 .004 .000 10000 20000 30000 40000 50000 60000 70000 Conditional standard deviation Again, the sheer number of data points (over 75000) makes these graphs somewhat hard to interpret, but even a perfunctory glance shows that this data is far less smooth than the estimates from less frequently sampled data, reflecting the issues discussed in section II (namely bid-ask bounce and nonsynchronous data). V: Concluding remarks In this paper I described the process of downloading high-frequency data, cleaning it with the R package RTAQ, and estimating conditional volatility with ARCH and GARCH models. Using return data from Google and PepsiCo, I tried to highlight certain issues inherent in the modeling of high-frequency data, including incorrectly recorded or nonsensical data points, problems with time stamps and nonsynchronous data, and bid-ask bounce. I showed how some of these problems could be solved by simple data cleaning, while others needed to be addressed with sampling frequency. Finally, I estimated conditional volatility using basic conditional heteroskedasticity models, and showed how they give much smoother estimates for volatility than using basic sample methods like absolute returns. It is important to be aware of alternative data modeling techniques such as the ARCH/GARCH framework when using return data, because the processes followed by typical return data are often not as simple as basic finance theory would imply. My findings that the return data was non-normal and did 19 not follow a martingale are certainly not unique, and it is important to account for this in model estimation. Classical finance often uses simplified models of returns to avoid extremely messy and inelegant math, but it is important when doing financial research that the models estimated are appropriate to the data, as opposed to simply fitting the theory. 20 References 1) Ait-Sahalia, Y., Mykland, P. A., and Zhang, L. (2005), "How Often to Sample a Continuous-Time Process in the Presence of Market Microstructure Noise," Review of Financial Studies, 18, 351416. 2) Andersen, T.G., and Bollerslev, T. (1998), “Answering the Skeptics: Yes, Standard Volatility Models Do Provide Accurate Forecasts,” International Economic Review, 39, 885-905. 3) Barndorff-Nielsen, O. E., Hansen, P. R., Lunde, A., Shephard, N., (2009), “Realised kernels in practice: Trades and quotes.” Econometrics Journal 12, 1_33. 4) Bollerslev, T. (1986), "Generalized Autoregressive Conditional Heteroskedasticity," Journal of Econometrics, 31, 307-327. 5) Engle, R. F. (1982), "Autoregressive Conditional Heteroskedasticity With Estimates of the Variance of United Kingdom Inflation," Econometrica, 50, 987-1008. 6) Fama, Eugene F. (1970), “Efficient Capital Markets: A Review of Theory and Empirical Work.” Journal of Finance XXV, no. 2 . 7) Hansen, P. R. and Lunde, A. (2001), “A comparison of volatility models: Does anything beat a GARCH(1,1)?”, Working Paper Series No. 84, Aarhus School of Business, Centre for Analytical Finance, 1-41. 8) Lo, A. W. and MacKinlay, A. C. (1988), “Stock market prices do not follow random walks: evidence from a simple specification test,” Review of Financial Studies, 1(1), 41-6 9) Madhavan, A., (2000), “Market microstructure: A survey.” Journal of Financial Markets 3, 205– 258. 10) Zivot, E. (2005), “Analysis of High Frequency Financial Data: Models, Methods and Software. Part II: Modeling and Forecasting Realized Variance Measures.” Unpublished. 21 Appendix Graphs of conditional variance from model estimation using Pepsi: 5 minute data ARCH(1): .040 .035 .030 .025 .020 .015 .010 .005 .000 250 500 750 1000 1250 1500 1250 1500 Conditional standard deviation GARCH(1,1): .036 .032 .028 .024 .020 .016 .012 .008 .004 .000 250 500 750 1000 Conditional standard deviation 22 Absolute returns: APEP_5MIN .032 .028 .024 .020 .016 .012 .008 .004 .000 250 500 750 1000 1250 1500 10 minute data ARCH(1): .035 .030 .025 .020 .015 .010 .005 .000 100 200 300 400 500 Conditional standard deviation 23 600 700 GARCH(1,1): .030 .025 .020 .015 .010 .005 .000 100 200 300 400 500 600 700 Conditional standard deviation Absolute returns: APEP_10MIN .032 .028 .024 .020 .016 .012 .008 .004 .000 100 200 300 400 24 500 600 700 800

© Copyright 2026