Presentation

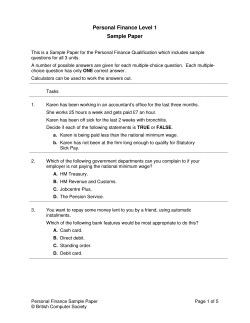

FWA HSBC Financial Backpack Program Understanding Credit All materials are on FWA.ORG Follow us on FACEBOOK Top Lessons • Credit has many advantages and disadvantages • Understand costs of credit: principal, interest, term • Know why a bank will offer you credit: credit report, credit score, credit history • Learn how credit impacts many areas of your life from interest rates to jobs Copyright © 2014 by FWA of New York Educational Fund. All rights reserved. Page 2 Why do people borrow money? • Why do people borrow money? • When is OK to borrow money? • When should you not borrow money? Copyright © 2014 by FWA of New York Educational Fund. All rights reserved. Page 3 Case Study William, a junior in college, is putting together his financial goals. On his list are a new computer and a car. He has an old laptop that has been temperamental but holding on. He plans to buy a car for after college for getting to his job. He has been diligent in putting money into his savings account. William finds a sale on a laptop. It normally $650, but this special weekend sale has it for only $500. The website says that a buyer can just pay $10 per month to pay off the bill. The fine print has the store’s financing details: The interest rate is 18% with monthly payments of $10, or 3% of balance. Using an online loan payment calculator, William sees that it would take 6 years and 2 months to pay off the laptop. Interest charges would be $299 so the laptop would end up costing him $799 for the $500 laptop. • What can William do instead of financing the laptop? • What if his computer had crashed and he needed the new laptop for school? If he decided to go with financing, what could he do so it does not cost $799? Copyright © 2014 by FWA of New York Educational Fund. All rights reserved. Page 4 Credit and Debt Credit is the ability to obtain goods or services before paying for them based on a promise to pay later. It is not free money, it is a loan. Debt is money that you borrow and must repay Debt‐to‐Income (DTI) ratio is the percentage of your income that goes toward paying your debt. It gives lenders an idea of how likely that borrower will repay loan. Copyright © 2014 by FWA of New York Educational Fund. All rights reserved. Page 5 Types of Credit • Revolving credit (example: credit card) • Borrow for multiple purchases without going over credit limit • Repay what is owed each month • Installment credit (example: car loan) • Borrow a specific amount of money to buy something now • Make regular payments to repay over time by a set date • Cash loans • Borrow a specific amount of cash to repay later by a set date • Service credit (example: cell phone, electricity) • Promise to pay for services used each month • Student Loans • Borrow while a student to pay tuition and fees • May have no interest or payments due while in school • Usually lower interest rate than other credit options • Interest and repayment due after you graduate. • Can repay over longer period of time than other credit. Copyright © 2014 by FWA of New York Educational Fund. All rights reserved. Page 6 Credit Cards Credit cards are a form of revolving credit • Payments are deferred, you can charge to a set limit • Used primarily for purchases but can provide cash advances for an extra fee and higher interest rate • Repay in full or over time with monthly payments • Interest is charged on your outstanding balance • APR is an Annual Percentage Rate that you pay in a single year on the money you borrow. Copyright © 2014 by FWA of New York Educational Fund. All rights reserved. Page 7 Choosing the Right Credit Card There are different types of credit cards. Key features to consider in choosing any credit card are: • Interest rate/APR • Grace period Have greatest effect on cost of credit • Number of days before the bank starts charging you interest for new purchases • No charges or interest expense if you pay in full prior to the due date • Annual fee http://www.creditcards.com/college‐students.php Copyright © 2014 by FWA of New York Educational Fund. All rights reserved. Page 8 Activity: Analyze a real credit card offer Copyright © 2014 by FWA of New York Educational Fund. All rights reserved. Page 9 Credit Card Management Tips • Use one card for all your charges to keep your charging in check. • Review your spending at the end of the year to plan next year’s budget. • Collect reward points if you have a rewards card and redeem them. But, make sure the card fees are worth it! A high annual fee might offset any benefits. • Pay your balance off in full every month or even every week to make sure you can afford your purchases. • Never spend over your credit limit. Some cards allow this, but then charge you additional exorbitant fees. • Use a prepaid card to limit your spending. Check the fine print to ensure the fees are sensible and affordable. Copyright © 2014 by FWA of New York Educational Fund. All rights reserved. Page 10 Credit Card Smarts If you charge an item, be ready to pay it off when you receive your credit card bill. • If you purchase an iPod for $100 on your credit card with 17% APR and make the minimum card payment, it will take you 5 months to pay for it and it will cost an extra $4, or $104 total. • If you purchase an iPhone for $500 on your credit card with 17% APR and make the minimum card payment, it will take you 2 years to pay for it and it will cost an extra $92, or $592 total. http://www.creditcards.com/calculators/minimum‐payment.php Copyright © 2014 by FWA of New York Educational Fund. All rights reserved. Page 11 Case Study You are a brand new loan officer. Your boss gives you two customer files to analyze and decide who should receive a loan from the bank. • File #1: Peter needs to purchase a car for his new job. His salary will be $5,000 monthly. He has $15,000 in his savings account. The car he wants to purchase will cost him $15,000 with 3% interest and 4‐year term, and his monthly payment would be $322. His credit report shows he pays on time and only has one credit card. • File #2: Amanda has been unemployed for the past six months. She only has $7,000 in her savings account. She needs a new car to go for job interviews. The car Amanda wants to purchase will cost her $20,000 with 3% interest and 4‐year term, her monthly payment would be $442. Her credit report shows a few late payments during the past six months and she has three credit cards. Use the table to help you analyze each case. Copyright © 2014 by FWA of New York Educational Fund. All rights reserved. Page 12 Credit Report Your credit report represents your trustworthiness and affects your credit score. It contains four parts: 1. Personal information. Your name, past and current addresses, date of birth, social security number, and past and current employers. 2. Credit History. All credit card and loan information, including payment activity, how much you borrowed, and whether you paid on time or not. 3. Inquiries. A list of people who have requested to see your credit report. You can prevent access by placing a security freeze on your file. 4. Public records. Information on bankruptcies, foreclosures, lawsuits, wage attachments, liens, judgments, and debt information provided by debt collection agencies. Credit reporting agencies keep track of your debt and how you pay your bills. Often, they provide this information to businesses when you apply for a loan, apply for a job, or look for an apartment. Copyright © 2014 by FWA of New York Educational Fund. All rights reserved. Page 13 Check Your Credit Report • When you begin to use credit, each of the three major U.S. credit reporting agencies (Equifax, Experian, and TransUnion) compiles a report on you. Check these reports regularly to make sure there are no errors and no suspicious activity. • By law, you are entitled to one free copy of your credit report from each of these companies each year. • To get a credit report when you start using credit, just visit www.annualcreditreport.com or call 877‐322‐8228. • Beware of many sites with similar names that offer “Credit Reports” but charge for them. Some sites are fraudulent and are just looking to obtain your personal information. Copyright © 2014 by FWA of New York Educational Fund. All rights reserved. Page 14 Credit Score The following allocations are used to determine your FICO credit score: • • • • • 35% Payment history 30% Amount of debt 15% Length of credit history 10% New credit accounts and inquiries 10% Types of credit used (amount of available credit used) Copyright © 2014 by FWA of New York Educational Fund. All rights reserved. Page 15 Steps for Building Good Credit Good credit means that you pay your bills on time and you repay your loans as promised. A good credit record will enable you to take out a loan if you want to buy a car or house, or start a business someday. To build good credit: Pay all basic expenses, such as rent and utilities, on time. Make loan and credit card payments on time. Pay loans before you spend money on other purchases. Apply only for the credit you need. If you apply too often, lenders might think you are in financial trouble. • Do not bounce checks. • • • • Copyright © 2014 by FWA of New York Educational Fund. All rights reserved. Page 16 Summary Credit is the ability to borrow money with the promise to repay it at a later date. Debt is money that you borrow and must repay. Debt and credit go hand in hand. • Credit is used to get debt, and debt can affect your credit. • If you manage your credit well, you can get better rates for your debts. • If you manage your debts well, you can build up your credit and improve your credit history. Copyright © 2014 by FWA of New York Educational Fund. All rights reserved. Page 17 Assessment and Evaluation Thank you for your participation. Please complete the evaluation form. All materials and resources are available on the FWA Website: WWW.FWA.ORG Follow us on Facebook at FWA Financial Backpack Copyright © 2014 by FWA of New York Educational Fund. All rights reserved. Page 18

© Copyright 2026