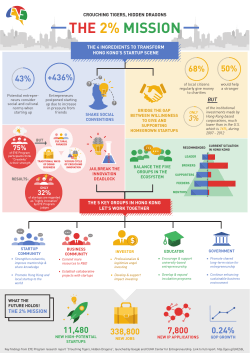

Understanding growth and non-growth in entrepreneurial