Tourist Refund Scheme â Issuing Solution Guide for

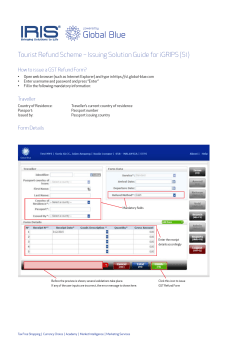

Tourist Refund Scheme – Issuing Solution Guide for GRIPS!Now(S3) How to issue a GST Refund Form? • Fill in the following mandatory information accordingly: Traveller *Ask if traveller has a Global Blue Card. If yes then fill in the Global Blue Card number and press enter key. The traveller data will be auto-filled upon validation of the Global Blue Card. Country: Traveller’s current country of residence Detailed Amounts Receipt Number: Receipt number Receipt Date: Receipt date Goods Description: Goods description Quantity: Quantity of the goods purchased Gross Amount: Total purchase sales amount on receipt • Click on “Print Cheque” button • GST Refund Form is printed successfully Mandatory fields Click this icon to issue GST Refund Form Tax Free Shopping | Currency Choice | Academy | Market Intelligence | Marketing Services MY_S3_A4_150324.indd 1 2015-03-24 15:03:11 Frequently Asked Questions(FAQs) Question Answer What is the minimum purchase amount? Minimum purchase amount is MYR 300. If total purchase amount for a single receipt is less than MYR300 then you may combine more than one receipt belonging to same store. Who should I contact if the system is faulty? Or if I am not able to print GST Refund Form? Please contact IRIS Global Blue Technical Helpdesk Hotline: 03-89960466. How to order Global Blue Contingency Forms? Send an email to [email protected] or call the Global Blue office: 03 2776 6927 to place orders for Contingency GST Refund Forms. Tourist Refund Scheme (TRS) Rules A tourist shall be entitled to the refund of GST under the TRS if s/he satisfies the following conditions: • • • • • • • • • • S/he is neither a citizen nor a permanent resident of Malaysia and holds a valid international passport. S/he is 18 years of age or above on the date of export validation. S/he is a foreign diplomat leaving the country after completion of service in Malaysia and is in possession of a document from the relevant diplomatic or consular mission stating that s/he is permanently leaving Malaysia. S/he is not nor has been employed in Malaysia at any time in the 3 months preceding the date of purchase of the eligible goods. S/he departs Malaysia by means of air transportation from one of the 8 international airports in the scope of the TRS. S/he is not a member of the cabin or flight crew of the aircraft on which s/he is departing out of Malaysia. S/he must have purchased the eligible goods within 3 months prior to the date of departure. S/he must spend at least three-hundred Malaysian Ringgit (MYR300) (GST inclusive) at the same Approved Outlet. Accumulation of purchases is allowed if purchases are made from the same Approved Outlet on different days. S/he must take the eligible goods out of Malaysia to another country as accompanied (hand carried) or unaccompanied (checked-in) luggage. If s/he is entering or staying in Malaysia on a student pass, your entitlement under the TRS is like any other foreign tourist. Non-eligble goods are: • • • • • • Wine, spirits, beer and malt liquor Tobacco and tobacco products Precious metal and gem stones* Goods wholly or partially consumed in Malaysia (except for clothing/tax invoices to be maintained) Goods which are absolutely prohibited from export under the written law Goods which are not taken out as accompanied (hand carried) or unaccompanied (checked-in) luggage *All Approved Outlets selling jewellery will be provided with Customs approved security bag with serial number. Security bag to be provided by Federation of Goldsmiths And Jewellers Association of Malaysia (FGJAM). For more detailed information please refer to Royal Malaysian Customs Department website: Guidelines - http://gst.customs.gov.my/en/cp/Pages/cp_trst.aspx Frequently Asked Questions - http://gst.customs.gov.my/en/rg/Pages/rg_trst.aspx Version 2 Tax Free Shopping | Currency Choice | Academy | Market Intelligence | Marketing Services MY_S3_A4_150324.indd 2 2015-03-24 15:03:11

© Copyright 2026