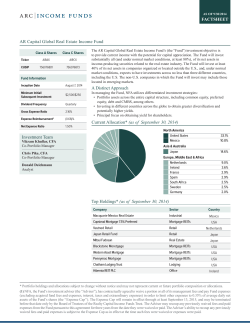

Pioneer Funds