H t St t f T

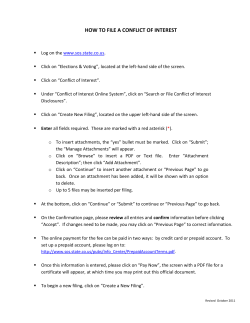

2009 Finance & Business Operations Symposium (FBOS) How to H t Stay St outt off T Trouble bl with Local and State Tax Authorities! Anna Hofmeister, Hofmeister CPA Brent Woods, Esq., CAE Al Thomson, EA, CFP Thursday, May 14, 2009 Connecting Great Ideas and Great People Agenda Common miss-conceptions Federal filing g requirements q State filing requirements Local filing requirements Common Miss Miss-Conception Conception #1 We have a letter of exemption from the IRS, therefore we are not required to file anything. anything Common Miss Miss-Conception Conception #2 We are a 501(c)(3), 501(c)(3) so we are exempt from all taxes. Federal Filing Requirements Federal Form 990 Federal Form 990-T, if applicable Federal Group Exemptions IRS Pub. P b 4573 Benefit: Each chapter does not have to file for its own exemption (save $) “Parent” org must file annual update. Must list: Chapters who have changed names or addresses Chapters no longer included in GE Chapters to be added to GE GE Chapters must still comply with 990 requirements Consider “opt out” policy State Filing Requirements Sales and Use Tax Unclaimed Property Charitable Registration Sales & Use Tax Unless specifically exempt from sales and use tax,, a nonprofit p f organization g must p payy sales tax on products/services it buys/receives, collect and remit sales taxes on certain products it sells, and/or use tax for purchases when the vendor did not charge sales tax. Sales & Use Tax What is taxable? In general general, tangible goods bought (exemption possible) and sold Warning! Some jurisdictions tax services! Where are you liable? “Nexus” concept Selling S lli via i iinternet/mail t t/ il nott sufficient ffi i t nexus (Q (Quill ill C Corp v. N North th Dakota) Indirect physical presence may create nexus (Borders v. State Board of Equalization [CA]) Due date VA Monthly ST-9 (by 20th/can iFile online) MD Monthly by 20th (State sends form or can bFile online) DC Monthly by 20th (Form FR 800M, online via eTSC) (Info - FR 379) Discussion Unclaimed Property Tangible or intangible property that has remained unclaimed by its owner for an extended period of time. Unclaimed Property Savings and checking accounts Wages or commissions Customer deposits Credit balances Refunds And more Unclaimed Property Exemptions – Account credits credits, rebates rebates, gift certificates certificates, checks in normal course of business. Check jurisdiction! Due diligence – letter sent to owner’s last known address Dormancy period Electronic or paper VA – Either (CD or upload – NAUPA 2 format) MD – Online O li ((upload l d NAUPA 2 format f or fill fill-in i online) li ) Due date VA – Varies by type of property MD – 3 years DC – Varies by type of property VA – Nov. 1 MD – Oct. 31 DC – Oct. Oct 31 Discussion Charitable Registration Requires that anyone that solicits funds in a particular state must initially register with that state and file an annual report thereafter. thereafter Charitable Registration What to file Unified Registration Statement Federal Form 990 State form Due date Electronic or paper Fee Local Filing Requirements Business License Personal Property Business License A business must file for a business license to operate in a specific j i di ti jurisdiction. Most M t nonprofits fit pay a fee f equal to a percentage of gross unrelated business receipts in the prior year. year Business License What is filed Electronic or paper Due date Discussion Personal Property All businesses must pay business personal property taxes on tangible property they own, such h as ffurniture, it computer t hardware, equipment, and vehicles. Personal Property Exemptions What is filed Electronic or paper What is covered Due date Discussion Questions and Answers Contact Information: Anna Hofmeister, CPA Phone: 202-419-5103 E-mail: [email protected] Brent Woods , Esq., CAE Phone: 703-736-8900 E-mail: [email protected] Al Thomson, EA, CFP Phone: 703-524-1595 E-mail: [email protected] www.asaecenter.org Connecting Great Ideas and Great People

© Copyright 2026