TEXAS RETAIL SURVEY 2013 EDITION

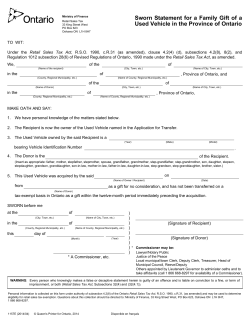

TEXAS RETAIL SURVEY 2013 EDITION COPYRIGHT 2013 BY EUREKA GROUP TEXAS RETAIL SURVEY INQUIRIES REGARDING THE TEXAS RETAIL SURVEY SHOULD BE DIRECTED TO THE EUREKA GROUP, PUBLISHERS OF THE SURVEY THE TEXAS RETAIL SURVEY C/O THE EUREKA GROUP 3976 GARNET ROAD POLLOCK PINES, CALIFORNIA 95726 TEL: (530) 647-1219 FAX: (530) 647-1257 Also available from Eureka Group CALIFORNIA RETAIL SURVEY 2013 EDITION WASHINGTON STATE RETAIL SURVEY 2013 EDITION Complete coverage of California & Washington State retail markets. All counties and cities included. 500 pages softbound. $160 The Texas Retail Survey is published annually by the Eureka Group, for the sole use of its customers. Reprint by permission only. Factual material contained in the Survey obtained from sources believed to be reliable. Rights of reproduction and distribution are reserved to the publisher. Copyright 2013 by Eureka Group. COPYRIGHT 2013 BY EUREKA GROUP TEXAS RETAIL SURVEY TABLE OF CONTENTS HOW TO USE THE SURVEY I INTRODUCTION What is the Survey? What is it Designed to Do? Unique Features Organization II EVALUATING A MARKET Choosing the Markets Interpreting the Data Rankings and Indices Recent Performance Long-Term Performance Future Prospects III COUNTY & CITY REPORTS IV STATISTICAL METHODS Growth Persistence Index Retail Sales Forecasts V GLOSSARY OF TERMS HIGHLIGHT SCREENS County Retail Market Highlights City Retail Market Highlights SECTION A Texas Composite Sales Report County Sales Reports SECTION B Large Cities Sales Reports SECTION C Summary - County Rankings & Indices SECTION D Summary - City Rankings & Indices COPYRIGHT 2013 BY EUREKA GROUP TEXAS RETAIL SURVEY HOW TO USE THE SURVEY COPYRIGHT 2013 BY EUREKA GROUP TEXAS RETAIL SURVEY HOW TO USE THE SURVEY I Introduction * What is the Survey? * What is it Designed to Do? * Unique Features * Organization II Evaluating a Market * Choosing the Markets * Rankings and Indices III County and City Reports * Sample Reports * Contents of County and City Reports IV Statistical Methods * Growth Persistence Index * Relative Strength Ratio V Glossary of Terms COPYRIGHT 2013 BY EUREKA GROUP TEXAS RETAIL SURVEY I. Introduction What is the Retail Survey? The Retail Survey is an independent market research advisory publication that focuses solely on the Texas retail market. In terms of geographical coverage, retail sector coverage, and sales trend data and analysis, it is believed to be the most comprehensive service of this type available on the Texas $300 billion retail marketplace. The Survey is completely revised and updated annually. What is the Retail Survey Designed to Do? The Retail Survey is designed to provide a comprehensive review of retail sales activity in every county in the State of Texas, plus over 300 of the largest cities in the state. In total, the Survey reports on the historical sales trends in each of over 550 individual market areas in Texas, based on sales activity of over 312,000 individual retail outlets. In addition to historical sales trend data, the Survey also includes a wide range of statistical measurements that evaluate the past performance of individual markets and the prospects for future growth. The Retail Survey has been designed so that it can be used productively by a wide range of customers that find it necessary to track and analyze retail markets in Texas. Using the Survey, business executives with varied backgrounds and objectives can substantially improve their ability to make informed decisions. (1) The Independent Retailer, who needs to know how his or her local market is performing, can rely upon the Retail Survey to provide a detailed examination of sales activity by type of retail store, and what the prospects are for growth in the future. Using these sales data, market indices and rankings, the independent retailer is better prepared to forecast his/hers store’s future performance. (2) The New-To-Market Retailer, who needs to know the size of the market, and long-term trends, can rely upon the Retail Survey to provide the market research that will to be needed to help launch a new business. Before the new-to-market retailer opens the door, short-term and long-term trends will have been identified and factored into the company’s business plan. Fewer surprises substantially increase the chance of launching a successful new venture. COPYRIGHT 2013 BY EUREKA GROUP (3) The Marketing Manager for a wholesaler or manufacturer, who wants to pinpoint the fastest growing markets, can rely upon the Retail Survey to decide where to concentrate advertising and promotion efforts to guarantee greatest impact. Assigning sales staff to geographical territories can be accomplished with a greater degree of confidence, and distribution channels can be reviewed and modified based on changing market conditions and trends. (4) Bankers and Financial Advisers use the Retail Survey data and analytical measurements as benchmarks to evaluate how their individual retail clients are performing compared to market averages, and identify problem areas at an earlier stage. (5) Government Officials, with responsibilities for urban planning, tax revenue forecasting and economic development, can quickly utilize the Retail Survey to compare the performance of their community with neighboring cities and counties, identify areas of weakness and competitive advantage, and develop more effective policy initiatives. (6) Providers of Business Services, such as accounting firms, real estate brokers, and advertising firms, can efficiently track retail trends in their market area, and identify retail sectors offering the best opportunities for new client development. (7) Chain store and Supermarket Executives, who need to plan site location strategies, can quickly narrow down the list of potential expansion locations, identify market areas that are presently under-served, and easily track their store’s sales performance compared to the overall market. (8) Real Estate Appraisers, who are responsible for analyzing local market trends and their impact on real estate values for retail properties, use the Survey’s extensive data and analysis to accurately identify supply and demand conditions that have important affects on property values. (9) Media Executives, in television, radio, and newspapers who are responsible for marketing and advertising strategies, use the Survey to keep track of their local retail market, identify fast-growing retail sectors to target for new advertising revenue, and compare local retail trends with surrounding areas. TEXAS RETAIL SURVEY The Survey’s Unique Features The Texas Retail Survey has been designed with several objectives in mind: (1) comprehensive coverage of the market (2) ease of use by a wide range of customers regardless of their professional background, and (3) the use of objective analytical measurements that improve the ability of customers to understand the retail sales trends in each market, and to quickly compare growth performance among various areas. These objectives have resulted in the Retail Survey containing a number of unique features that deserve to be highlighted: (1) Broad Coverage The Texas Retail Survey provides detailed report on each of 254 counties and 323 cities in Texas. Retail sales data are broken down in detail for 14 separate retail store categories. This is believed to be the most comprehensive coverage of the Texas retail marketplace available anywhere. (2) Four Key Market Measurements Performance Index Relative Strength Ratio Growth Persistence Index Star Rating These four key market measurements allow Survey users to quickly understand the relative trends in each geographical market, and to accurately compare past performance and future prospects for growth among the markets of interest. The Performance Ranking provides an easily understood measurement of one market’s growth rate in the current year compared to all other markets in Texas. The rankings for each market range from 1 to 5, with 20% of the markets with the highest recent growth rate being assigned the 1 ranking. The Relative Strength Ratio measures the long-term retail sales growth trend in one local market compared to growth fluctuations in statewide retail sales. Since the Ratio covers a period of the last five years, it provides Survey users with an easily understood comparison of longer-term sales growth trends, relative to statewide averages. The ratio is derived by dividing the percentage increase in retail sales in a specific county or city over the past five years by comparable percentage increases for total statewide retail sales. market each year. This measurement is used to differentiate markets with steady, above average growth from those that experience wide fluctuations in their relative growth performance. The Star Ratings provide Survey users with a clear assessment of a market’s growth compared to all other markets in Texas. Markets that have grown the fastest over the last five years are given the five-star rating. (3) Retail Sales & Outlet Data Individual market reports appearing in the Texas Retail Survey contain nine years of sale data for up to 14 individual retail store categories. The Retail Survey also contains data on retail outlets in each of the past nine years for these same 14 retail store categories. These data provide the basis for preparing the analysis and rankings of each local market. Lastly, a Texas State Composite report is included in the Survey to provide an overview of aggregate retail sales activity for the entire state over the last nine years, and can be used as a reference point when comparisons of statewide and local retail conditions are desired. The Texas State Composite report can be found in Section A of the Survey. (4) Retail Sales Forecasts Lastly, the Survey provides a one-year forecast of retail sales for each of Texas’ 254 counties and 323 of the state’s largest cities. Organization The Survey is organized so that users can easily find and use the data they require with a minimum of time and effort. The Survey is divided into the following sections: * How to Use the Survey * Section A- Counties Retail Sales Reports * Section B- Large Cities Retail Sales Reports * Section C- Summary County Rankings &Indices * Section D- Summary City Rankings &Indices For new customers we recommend that the How to Use section be reviewed prior to using the Survey so as to become familiar with the terms and analytical measurements appearing in the Survey. Next, customers should spend about fifteen minutes reviewing each of the sections to become familiar with the various types of reports and their characteristics. The Growth Persistence Index measures the ability of a local market to consistently out-perform the overall COPYRIGHT 2013 BY EUREKA GROUP TEXAS RETAIL SURVEY RATING (AVG) LONE STAR COUNTY SALES REPORT & RANKINGS PERFORMANCE RANK GROWTH PERSISTENCE RELATIVE STRENGTH SALES RANK PER CAPITA SALES RANK STATE SALES% 3 57.1% 1.06 19 7 1.23% OUTLET GROWTH LAST 5 YRS OUTLETS RANK % STATEWIDE OUTLETS POP. RANK PER OUTLET SALES RANK 2.6% 8 1.17% 10 15 Market Share Gen Mrch 42.9% 36.5 12% 10% 8% Other 16.1% Apparel 2.0% 6% 4% Gas Stn 9.2% Build Matrl 5.7% TOTAL 2% Motor Vehicle 15.1% 06 07 Furn 1.8% 08 09 COUNTY 10 11 12 % STATEWIDE POPULATION 1.17% 2.50 $SALES PER HOUSEHOLD MOTOR VEH. & PARTS ELECTRONICS & APPL FURNITURE BUILDING MATRL GAS STATIONS APPAREL & ACCESSORY GEN MERCHANDISE RESTAURANTS & BARS 14% 2.0% 7.1% MEDIAN HSHOLD AGE SIZE Annual Retail Growth Rest & Bars 7.1% 5 YR GROWTH RATES SALES POPULATION #HOUSEHOLDS LOCAL MKT 8,278 $1,099 $1,000 $3,139 $5,045 $1,069 $23,489 $3,868 TEXAS NORM $6,982 $54,716 $50,052 $2,258 $1,198 $2,970 $4,916 $1,909 $8,575 $4,238 108,363 0% OUTLETS PER 10K POP 115 117 STATE PER CAPITA RETAIL SALES ($000) 05 06 07 08 09 10 11 12 13 GROWTH SALES MOTOR VEH. & PARTS 693,434 686,902 761,495 909,801 891,316 901,056 823,465 868,308 897,039 2.7% $3,126 FURN & HOME FURN ELECTRONICS & APPL. BUILD. MATERIALS 51,955 63,396 219,567 53,028 66,950 234,043 63,627 74,076 259,741 83,499 85,733 285,512 92,475 93,835 309,349 101,386 105,208 306,153 99,435 109,304 312,273 104,850 115,256 329,278 108,319 119,070 340,173 10.5% 9.2% 4.9% $378 $415 $1,186 FOOD & BEV. STORES 312,167 328,596 348,694 359,862 350,590 376,709 408,400 430,640 444,889 4.3% $1,550 DRUG/HEALTH STORES GASOLINE STATIONS APPAREL & ACCES. SPECIALTY STORES GEN MERCH. STORES MISC RETAILERS NONSTORE RETAILERS RESTAURANTS & BARS 80,116 227,896 89,793 56,077 1,299,327 93,345 22,502 237,474 94,080 249,145 94,919 58,545 1,645,358 94,732 25,947 247,588 98,470 279,417 101,752 63,423 1,623,528 93,544 31,201 270,820 105,718 343,859 97,974 67,949 1,772,237 97,619 26,081 305,519 115,800 390,971 103,482 68,900 1,755,498 108,532 22,910 318,471 121,012 431,337 105,634 63,702 2,051,388 107,995 30,507 345,492 142,752 501,895 106,365 68,426 2,336,587 112,698 36,471 384,781 150,525 529,226 112,157 72,152 2,463,830 118,835 38,457 405,734 155,506 546,737 115,868 74,540 2,545,353 122,767 39,729 419,159 8.9% 13.6% 2.0% 2.6% 8.7% 4.9% 4.3% 8.4% $542 $1,905 $404 $260 $8,871 $428 $138 $1,461 RETAIL SALES TOTAL 3,447,050 3,879,833 4,069,787 4,541,362 4,622,128 5,047,580 5,442,850 5,739,250 5,929,150 7.1% $20,664 PER OUTLET RETAIL OUTLETS 05 06 07 08 09 10 11 12 13 GROWTH SALES MOTOR VEH. & PARTS FURN & HOME FURN ELECTRONICS & APPL. BUILD. MATERIALS 174 67 64 85 177 70 66 91 179 84 65 93 183 95 84 96 190 96 94 96 188 92 93 101 180 86 84 105 188 90 88 110 191 91 89 111 1.0% 1.3% 6.2% 3.4% $4,618,659 $1,167,302 $1,313,711 $3,002,538 FOOD & BEV. STORES DRUG/HEALTH STORES GASOLINE STATIONS APPAREL & ACCES. SPECIALTY STORES GEN MERCH. STORES MISC RETAILERS NONSTORE RETAILERS RESTAURANTS & BARS 98 57 162 255 225 74 632 84 563 103 65 161 273 224 78 658 90 599 116 73 169 298 218 86 706 111 611 133 79 168 293 206 95 743 123 630 137 88 158 286 169 107 852 133 654 144 90 154 277 166 116 847 173 670 145 94 157 277 167 113 777 187 688 151 98 164 289 174 118 812 195 719 154 100 166 293 177 120 823 198 729 5.5% 6.1% -0.6% -0.6% -4.4% 6.5% 2.8% 12.0% 3.3% $2,843,551 $1,533,192 $3,227,428 $387,670 $413,665 $20,875,986 $146,432 $196,900 $564,635 2,540 2,655 2,809 2,928 3,060 3,111 3,060 3,196 3,242 2.6% $1,795,760 RETAIL OUTLETS TOTAL CITY TREND (YR) POPULATION SALES PER OUTLET($) 05 06 07 08 09 11 12 13 5 YR GROWTH 250,321 252,001 260,526 269,073 274,881 277,743 277,743 277,743 2.0% 1,357,106 1,461,331 1,448,838 1,551,012 1,510,499 1,622,494 1,778,709 1,795,760 1,828,856 4.4% Summary: The Performance Rank of 3, measuring sales growth in the most recent year, is average. Over the past 10 yrs, the Growth Persistence Index (57.1%) has been average, while the 5 yr Relative Strength Ratio of 1.06 is above the state norm of 1.0. In total sales, the county's rank is 19, while the Per Capita Sales Rank is 7. Population Growth has averaged 1.96% over the past 5 yrs, compared to statewide norm of 1.31%. TEXAS RETAIL SURVEY 10 246,685 Per Outlet Sales Rank is 285, representing avg sales per outlet of $1,795,760. The annual growth rate over the past 5 yrs for Per Outlet Sales has been 4.4%. Note: Growth Rates are annual for period 2007-2012. Sales & outlet data for 2013 are forecasts and subject to future adjustment. COPYRIGHT 2013 BY EUREKA GROUP II. Evaluating A Retail Market The Texas Retail Survey’s principal goal is to present as much accurate and relevant data and analysis as possible on each local retail markets so that our customers can make informed and intelligent decisions based on their particular interests. Since each customer has his or her own specific needs, the manner in which the Survey will be used will take many forms. Even though individual needs and interests will vary among customers, all can benefit from using the Retail Survey. Choosing the Markets The first step in putting the Texas Retail Survey to practical use is to choose the market area or areas you wish to examine. The selection of the market(s) will of course depend upon the customer’s particular objective. If your interests lie in only one specific market (one city, for example), your choice is simple...just turn to the appropriate page that contains that particular city’s report. However, if your interests are broader, you can choose the markets to examine based on one or more criteria, such as by size (the top ten markets by volume of retail sales), or by various measurements of growth (all markets ranked No.1 or 2 for Performance). By using Section C and Section D, you’re able to easily identify county and city markets that meet various types of selection criteria. These are but a few of the ways Survey users can narrow their field of interest. Since the Texas Retail Survey contains such a wide range of data, analysis, and cross comparisons among individual markets, users frequently develop their own unique methods to use the market reports to meet their individuals objectives. Interpreting The Data - An Example At first glance, an individual market report may appear overwhelming, but one does not need any specific professional background to put the data to productive use. To get a better grasp on how to use and interpret a typical market report, one will be examined step-bystep. For this exercise, we have developed a hypothetical market report called "Lone Star County". This fictitious report, used only for illustration, contains in every detail the type of information, data and analysis that can be found in an actual county report contained in the Texas Retail Survey. Please refer to the previous page containing this Lone Star County report. COPYRIGHT 2013 BY EUREKA GROUP Rankings and Indexes Starting at the top of the page, we first see that Lone Star County has a Sales Rank of 19. This means that based on actual volume of total retail sales, Lone Star County is the nineteenth largest among the 254 counties in Texas. In other words, the retail market in this county is among the largest in the state, measured in absolute terms. Next, we find that the Per Capita Sales Rank is 7, or seventh highest among the 254 counties. From this ranking, we learn that, on average, retail sales are much higher than one would expect based on the county’s population size. Several reasons could account for this high per capita sales activity. One, it could be due to residents from adjacent counties spending their income in retail stores in Lone Star County, thereby pushing up the level of per capita sales, since Lone Star County’s per capita sales is calculated only on its own population base. Another reason may be that the income level in Lone Star County is significantly higher that those found in most other counties, allowing local residents to spend more on a per person basis. Recent Performance On the far left hand side of the top section, we find that Lone Star County’s Performance Rank is 3-average. The Performance Rank measures the growth rate in 2012 relative to all other counties. Rankings range from 1 to 5, with 1 assigned to the top performers. With a Performance Rank of 3- average, we are told that Lone Star County has experienced retail sales growth that falls within the midpoint range during the most recent year in which actual sales data are available. Although an important measurement of current performance, it does not tell anything about how Lone Star County has fared over the longer term. Long-Term Performance Now go to the Relative Strength Ratio. The Relative Strength Ratio for Lone Star County is 1.06. This is interpreted as meaning that the county’s retail sales have grown 6 percentage points faster than statewide retail sales over the five-year period from 2007 through 2012. From the Relative Strength Ratio, we can determine how well or poorly Lone Star County’s growth has been compared to statewide trends over this five-year period. TEXAS RETAIL SURVEY Future Prospects Although the Relative Strength Ratio is an important measurement in assessing long-term trends, we also want to know how consistent is the growth in Lone Star County. Put another way, in any given year, what has been the likelihood that Lone Star County would experience a growth a rate in retail sales that exceed the statewide average growth rate? To answer this question, refer to the Growth Persistence Index for Lone Star County. We find that the Index is 57.1%, compared to a perfect score of 100%. From this we learn that Lone Star County has done reasonably well in out-performing statewide growth rates over a period of years. For a complete description of interpreting the Growth Persistence Index, please refer to the Statistical Methods section appearing later in this section. To complete our review of the uppermost section of the report, we now turn to the graphic presentation on the left of the page, entitled Market Share. Here, we see that the General Merchandise sector in Lone Star County is the leading sector, accounting for 42.9% of all retail sales in the county, based on actual 2012 sales data. The next graphic section provides an historical comparison of Lone Star County and statewide sales growth rates from 2006 through 2012. To the far right of the page is a table comparing dollar retail sales per household for Lone Star County (Local Market Column) to comparable data for the state as a whole. This table tells us that total retail sales per household in Lone Star County amount to $54,716, compared to a statewide norm of $50,052. Overall, Lone Star County household retail spending is much higher than statewide norms. Differences in individual categories are likely due to some combination of higher income levels of local residents and more attractive pricing/selection and marketing in the local market relative to statewide norms, encouraging out-of county residents to travel to Lone Star County for shopping. Star Rating System Each county and city market report includes a composite star rating at the top of the page. This composite rating reflects the individual market’s sales growth rate relative to all other markets, over the past five years. COPYRIGHT 2013 BY EUREKA GROUP The top 20% of markets, ranked by sales growth, receive the five star rating. The next 20% of markets earn four stars (above average), followed by three stars (average), two stars (below average), and one star (lowest), in increments of 20% based on the fiveyear sales growth ranking. With the star rating system, Survey users receive a clear view of how a specific local market compares with all other markets in terms of long-term sales growth. From this quick review of the first page of Lone Star County report, we have a much better understanding of this market’s size, growth trends, spending patterns, and overall standing relative to other counties in Texas. It is one of the largest counties in terms of absolute sales volume and per capita sales. It has a long-term tendency to grow faster than statewide averages, and its persistence to out-perform the statewide growth is rated average. Further, retail sales per household are much higher than the state norm, indicating that Lone Star County is pulling retail spending into the local area from adjacent counties. Per Capita Retail Sales To round out our overall understanding of the Lone Star County retail market, we must now examine several additional data in the report. Based on 2012 data, Lone Star County has the 7th highest level of per capita sales, amounting to $20,664. The leading category of per capita sales is the General Merchandise Store sector ($8,871). Also, note that the Median Age (36.5 yrs. old) and Household Size (2.50). Both these data can be valuable in better understanding the buying habits and preferences of local area consumers, especially when compared to statewide norms found in the Texas Composite report (Section A). Outlet Data th Based on 2012 data, Lone Star County has the 8 highest number of retail outlets (Outlets Rank) among the 254 counties, even though its population base is tenth in the state (Population rank). This is not surprising. The solid long-term retail sales growth has understandably attracted more retail outlets than would be otherwise expected given its population size. TEXAS RETAIL SURVEY We also see that the number of retail outlets is increasing at an annual rate of 2.6%. New retailers are being attracted to the market due to its above average household spending and its average growth performance. Although the number of retail outlets is growing, the number is surely not excessive. If you refer to the data on “outlets per 10,000 population”, you learn that Lone Star County has 115 retail outlets for each 10,000 of population in this market, compared to a state norm of 117. Since the number of outlets per population base is somewhat lower than the norm, the market can likely absorb additional retail outlets, especially considering the relatively high sales per outlet. column providing a calculation of the average annual growth rate for each category over the past 5 years of actual data (2007-2012). Using these data one can quickly track the number of new entrants in each market sector, allowing Survey customers to quickly identify those sectors that are attracting new retail store locations and increased competition. For example, we see that restaurant/bar outlets have expanded from 611 to 719 between 2007 and 2012, a 3.3% increase in competitors per year during this five year period. The report also shows that restaurant/bar outlets are forecasted to reach 729 in 2011. The lower section of the Lone Star County report contains a year-by-year history of the number of retail outlets for each of the 14 retail sectors, with the last III. County and City Report Each county and city report contains a wide range of data, market rankings and indices, all of which can be used to gain a better understanding of the trends that exist in each market area. The following briefly outlines the various components included in the Retail Survey Reports. Sales Rank - A ranking based on the total retail sales in the county or city, as of the most recent year in which actual data are available. Forecasted data are not used to determine rankings. For counties, the rankings range from 1 (highest) to 254 (lowest). For cities ranking ranges from 1(highest) to 323 (lowest). Relative Strength Ratio - A measurement of the fiveyear sales growth (2007-2012) trend in a city or county compared to the sales growth trend statewide. An index of 1.25 can be interpreted as meaning that during the past five years, retail sales in the county or city grew 25 percentage points faster than the statewide average. An index of 2.35 would be interpreted to mean that retail sales in that local market have grown 135 percentage points faster than the state norm. Conversely, a Ratio of .85 would mean that the local market grew slower than the statewide average...in this example 15 percentage points lower than the statewide average. Per Capita Sales Rank- A ranking based on total 2012 retail sales in the county or city, divided by the 2012 population in that county or city. For counties, the rankings range from 1(highest) to 254(lowest). For cities ranking ranges from 1(highest) to 323 (lowest). Growth Persistence - An evaluation of a county/city’s ability to consistently out-perform statewide growth trends. This index ranges from 100% (highest) to 0% (lowest). Please see the Statistical Measures section for detailed explanation. Percent Statewide Sales- Calculated by dividing total retail sales in the county or city by the total retail sales in Texas, as of the most recent year in which actual data are available. This measures the "market share" of a county or city relative to total retail sales in the state. Performance Rank- A ranking of the percentage growth in retail sales for the most recent year that actual data are available. The rankings range from 1(highest) to 5 (lowest). After all markets are ranked based on percentage growth, numerical rankings are assigned as follows: Sales Growth-Last 5 Years- Calculation of the compound annual rate of retail sales growth for the period 2007 through 2012. COPYRIGHT 2013 BY EUREKA GROUP TEXAS RETAIL SURVEY PERFORMANCE RANKINGS PERFORMANCE RANKS-COUNTIES PERFORMANCE RANKS-CITIES TOP 50 RANK 1 (HIGHEST) TOP 65 RANK 1 (HIGHEST) NEXT 50 RANK RANK 2 (ABOVE AVERAGE) NEXT 65 RANK 2 (ABOVE AVERAGE) NEXT 50 RANK RANK 3 (AVERAGE) NEXT 65 RANK 3 (AVERAGE) NEXT 50 RANK RANK 4 (BELOW AVERAGE) NEXT 65 RANK 4 (BELOW AVERAGE) LOWEST 54 RANK 5 (LOWEST) LOWEST 63 RANK 5 (LOWEST) Retail Sales (Actual) - Presented for an eight-year time frame, for each type of retail store. Note that the column immediately to the right of the retail sales data provides compound annual growth rates for the past 5 years in which actual data are available, for each retail store category. When there are no sales data for a particular category, it is due to no sales in that particular year, or that data are suppressed to avoid divulging data for a particular retailer. Retail sales data are derived from sales data reported by all retailers to the Texas Comptroller’s Office. For most retail categories, sales data represent retail sales subject to the Texas sales tax. The two exceptions are the motor vehicle & gasoline stations sectors. Data for these two categories are derived from gross sales reported on state sales tax returns. Retail Sales (Forecasts) - For each county & city, retail sales forecasts are prepared for the most recent year under review. These sales forecasts are not used to calculating the growth rates appearing in the far right column of each sales report. Population Growth - The actual compound annual rate of growth in population in a city or county for the most recent five-year period 2007-2012. Per Capita $ Sales - A measurement of the per-person retail sales for each county or city. It is calculated by dividing 2012 sales data by the 2012 population in the county or city. This measurement provides a means to compare sales volumes between two market areas that have significantly different populations, since it puts each market area on a relatively equal basis, regardless of population size. Data are rounded to the nearest dollar. Median Age - The median age of the county or city’s population. Household Size - The average number of people in each household in the county or city. Population Rank - A ranking based on the 2012 total population of each county or city. County rankings range from 1(highest) to 254 (lowest). City rankings range from 1(highest) to 323 (lowest). Population Trend Data - A statistical summary of county and city population data for the past nine years. Sales Per Outlet Trend Data -A statistical summary of county & city sales per outlet data for the past nine years. Market Share Graph - A graphic breakdown of retail sales by eight major retail categories. The percentage breakdowns are based on actual retail sales for the current year. Per Capita Sales Column - By retail category, a column on the far right side of the page showing $ amounts for 2012. Sales Growth Graph - A history of the percentage change in a county or city’s actual retail sales compared to statewide growth rates. Percent Statewide Population –Measures the percentage of statewide population that is located within the particular city or county. Growth Rate - A calculation of the annual compound rate of growth of retail sales during the most recent five years in which actual data are available. Growth rate calculations do not include sales projections. County Identifiers - Immediately following the name of each city in the top line of each city report is the name of the county or counties in which that city is located. When a city is located in more than 2 counties, the identifier section may be followed by a plus (+), indicating that one ore more county names are not listed due to space limitations. COPYRIGHT 2013 BY EUREKA GROUP TEXAS RETAIL SURVEY Sales Per Household Table - For each major retail sector, this table measures the dollar retail sales per household. The table compares these data for the local market with comparable data representing the statewide norm. They are calculated by dividing 2013 sector retail sales in a market by the current number of households within that market. By comparing the statewide data to the local market data, Survey users can identify important local market imbalances that point to either strengths or weaknesses in the local market. For example, if the table shows that a local market’s furniture store sales per household are significantly lower than the state norm, it may indicate that the existing local furniture stores are not adequately serving the local population, and thereby encouraging these consumers to shop outside this local market. Conversely, if furniture store sales per household are much higher than the state norm, it may indicate that the local market is attracting large numbers of shoppers from outside the immediate local market. IV. Statistical Methods Using what is believed to be the most timely, accurate and unbiased data available on retail trends, the Texas Retail Survey analyzes these data and presents a number of rankings and indices that have proven to be important measurements of market performance. Due to their uniqueness and analytical importance, two of these deserve special attention. To insure that customers can fully understand the rationale and construction of these analytical techniques, each one is described below. Growth Persistence Index - Growth can be measured in many ways, depending on the specific analytical objective. With this index, the objective is to identify those retail markets that have a consistent ability to grow faster than the state as a whole, based on yearby-year performance. Some markets show strong surges in retail sales growth in one or two years, followed by periods of below average growth. Conversely, other markets experience moderate (but still above average) growth year after year. When analyzing any specific retail market, Survey users will undoubtedly want to examine not only its ability to grow, but also the consistently of that growth. If a market is prone to wide and unpredictable swings in growth, a Survey user will want to be alerted to this fact. Using the past seven years growth rates for county/city markets and the statewide market, a calculation is made to determine the number of subsequent years in which a county, city, or retail sector market out-performed the statewide growth rate. COPYRIGHT 2013 BY EUREKA GROUP The result of these calculations is the basis for the Growth Persistence Index. Therefore, a local market that has experienced sales growth above the statewide average for every one of the last seven years would be given a perfect score of 28. Conversely, the example of Lone Star County used here shows a score of 12 out of a possible perfect score of 21. The Growth Persistence Index, in this example, is then calculated by dividing the actual score (12) by the highest possible score (21). The resulting Index becomes 57.1%. Among Texas’ 323 cities and 254 counties, it is rare for a specific local market to out-perform the statewide average growth rate for seven years in a row, earning a Growth Persistence Index of 100%. From a practical standpoint, a local market that earns a Growth Persistence Index of 70% and above is performing extremely well, and is characterized as a "strong" market. Markets with Growth Persistence Index’s between 60% and 69% are considered "above average", while markets with indexes ranging from 40% to 59% are characterized as "average". Markets with an index between 20% and 39% are "below average", while markets with indexes below 20% are termed "low" for this measurement. Using our fictitious Lone Star County as an example, we can demonstrate the calculation of the index: TEXAS RETAIL SURVEY CALCULATION OF GROWTH PERSISTENCE INDEX YEAR STATEWIDE GROWTH RATES LONE STAR CO. GROWTH RATES NUMBER OF SUCCEEDING YEARS COUNTY GROWTH GREATER THAN STATE 2006 5.47% 12.56% 3 2007 7.34% 4.90% 3 2008 9.11% 11.59% 2 2009 6.26% 1.78% 2 2010 6.97% 9.20% 1 2011 8.22% 7.83% 2012 2.56% 5.45% 1 0 Total = 12 Retail Sales Forecasts - Using the statistical forecasting technique referred to as exponential smoothing, historical trends over the most recent tenyear period are evaluated using six computerforecasting models, and the resulting trend characteristics are then extrapolated into the future. In using the forecasts contained in the Survey, customers should keep in mind that forecasts are never perfect. In the Survey, the forecasts rely upon historical trend characteristics. The Survey makes no attempt to predict future events that may have a significant impact on retail sales volume. Each county and city report contains detailed one-year forecasts of retail sales for each retail category. The forecast data are rounded, which may cause column data not to equal totals. V. Glossary of Terms Apparel & Accessory Stores: This broad group includes outlets primarily engaged in the retail sale of new clothing and accessories. Included in this category are retailers engaged in the sale of women’s, men’s, children’s, and or family apparel and/or shoes. Electronics & Appliances : Retail Outlets that offer household appliances, consumer electronics, computers and software, radios and other audio equipment are included in this category. Motor Vehicles & Parts: Retailers that are predominantly involved in the sale of new and used automobiles are included here. Often, these retailers also sell automobile parts. Building Materials: Outlets primarily retailing lumber, building materials, door and window products, and masonry materials to both consumers and construction contractors are included in this category. City: An area that has officially been incorporated under the laws of Texas as a city. From time to time, city boundaries do change, causing some change in the amount of retail activity, and population credited to a particular city. COPYRIGHT 2013 BY EUREKA GROUP County: Texas has 254 counties, which are the primary political and administrative subdivisions of the state. Current Year: Refers to that year in which actual (as opposed to forecasted) sales and outlet data are available for a particular city or county market. Drug & Health Care Store Group: These outlets are engaged in the retail sale of prescription drugs, proprietary drugs, and non-prescription medicines. These outlets usually also offer a range of related products, such as personal care items, stationery, and novelties. Due to data collection limitations, sales of prescription drugs are not included. As such, total retail sales for this category are understated. Food & Beverage Stores: Retailers primarily engaged in retailing food and beverages merchandise from fixed point-of-sale locations. Includes food stores offering a wide range of grocery products for retail sale, as well as smaller stores offering a limited line of food products. Due to data collection limitations, sales of food for home consumption are not included. As such, total retail sales for this category are understated. TEXAS RETAIL SURVEY General Merchandise Stores: Includes department stores, discount dept stores, and warehouse clubs. Non-Store Retailers: Included within this category are mail order houses, vending machine operators, direct selling establishments, and electronic shopping. Growth Rate: In city and county reports, growth rate figures in the far right column refer to the compound annual rate of change over the last five years in which actual data are available. The growth rate calculation does not include forecasted data. Food & Beverage Stores: This category includes retailers offering a line of food items, such as fruit & vegetable stores, meat markets, fish & seafood markets, bakeries, & liquor stores Furniture & Home Furnishings: Included within this category are retailers engaged in retailing new furniture, such as household furniture (e.g., baby furniture, box springs and mattresses) and outdoor furniture; home furnishings, or floor coverings. Misc. Retailers: This broad category includes stores with unique characteristics like florists, used merchandise stores, office supplies, gift stores, and pet and pet supply stores as well as other store retailers. N.A.: Data not available because the city had not yet been incorporated, or because publication of data may result in the release of confidential information on a specific retail firm, or for other reasons that make data unavailable. COPYRIGHT 2013 BY EUREKA GROUP Restaurants/Bars: Eating and drinking places offering either/or alcoholic beverages (beer, wine, spirits and meals for on-premises consumption. Gasoline Stations: Retailers primarily engaged in the sale of gasoline and/or diesel fuel are included in this category. These retailers also frequently sell related auto parts and offer repair service. They may also offer a line of packaged and prepared convenience food. Specialty Stores: This broad category includes such retailers as sporting goods, toy stores, or other specific leisure activities, such as needlework and musical instruments. Book stores are also included in this group. TEXAS RETAIL SURVEY HIGHLIGHT SCREENS CITY & COUNTY MARKETS COPYRIGHT 2013 BY EUREKA GROUP TEXAS RETAIL SURVEY COUNTY MARKET HIGHLIGHTS GROWTH PERSISTENCE TOP TEN 1 2 3 4 5 6 7 8 9 10 RELATIVE STRENGTH BOTTOM TEN FRIO UPTON COMAL DENTON GOLIAD KINNEY MCMULLEN WILLIAMSON ATASCOSA GLASSCOCK 10 9 8 7 6 5 4 3 2 1 POTTER KAUFMAN DALLAS BAILEY STARR LAMPASAS HIDALGO BAYLOR WICHITA TITUS TOP TEN 1 2 3 4 5 6 7 8 9 10 MCMULLEN GLASSCOCK DIMMIT DUVAL LIVE OAK FRIO KARNES HALL MEDINA SWISHER RETAIL SALES RANK TOP TEN 1 2 3 4 5 6 7 8 9 10 10 9 8 7 6 5 4 3 2 1 BORDEN KENT ROBERTS TERRELL ARMSTRONG IRION FOARD MOTLEY COTTLE BRISCOE CROSBY BRISCOE WALLER BORDEN FREESTONE GRAY IRION BAYLOR STEPHENS BAILEY POPULATION SIZE BOTTOM TEN HARRIS DALLAS TARRANT BEXAR TRAVIS COLLIN EL PASO HIDALGO DENTON WILLIAMSON BOTTOM TEN 10 9 8 7 6 5 4 3 2 1 TOP TEN 1 2 3 4 5 6 7 8 9 10 HARRIS DALLAS TARRANT BEXAR TRAVIS COLLIN EL PASO HIDALGO DENTON FORT BEND BOTTOM TEN 10 9 8 7 6 5 4 3 2 1 LOVING KING KENEDY BORDEN MCMULLEN KENT ROBERTS TERRELL STERLING MOTLEY CITY MARKET HIGHLIGHTS GROWTH PERSISTENCE TOP TEN 1 2 3 4 5 6 7 8 9 10 RELATIVE STRENGTH BOTTOM TEN Beeville Corpus Christi Kyle Pflugerville San Juan Atlanta Little Elm Pearsall Pleasanton Rockwall 10 9 8 7 6 5 4 3 2 1 Pittsburg Pantego No. Richland Hills Mesquite Marshall Mabank Liberty Lewisville Humble Coppell TOP TEN 1 2 3 4 5 6 7 8 9 10 Murphy San Juan Little Elm Pflugerville Crowley Leander Carrizo Springs Highland Village Pearsall Pecos RETAIL SALES RANK TOP TEN BOTTOM TEN 10 9 8 7 6 5 4 3 2 1 Hempstead Burkburnett Slaton Pantego Gatesville Alvin Hidalgo Bedford Gonzales Kennedale POPULATION SIZE BOTTOM TEN TOP TEN BOTTOM TEN 1 Houston 10 Slaton 1 Houston 10 Sunset Valley 2 3 4 5 6 7 8 9 10 San Antonio Dallas Austin Fort Worth El Paso Plano Arlington Lubbock Corpus Christi 9 8 7 6 5 4 3 2 1 Royse City Bandera Early Pinehurst Cameron Hewitt Port Neches Burkburnett Sachse 2 3 4 5 6 7 8 9 10 San Antonio Dallas Austin Fort Worth El Paso Arlington Corpus Christi Plano Laredo 9 8 7 6 5 4 3 2 1 Bandera Clear Lake Shores Kemah Beverly Hills Shenandoah Pinehurst Waller Pantego Woodville Note: A market rank of #1 in Top Ten column represents the highest ranking. A market ranking of #10 in the Bottom Ten Column represents the lowest ranking. COPYRIGHT 2013 BY EUREKA GROUP TEXAS RETAIL SURVEY SECTION A TEXAS COMPOSITE REPORT & COUNTY RETAIL SALES REPORTS COPYRIGHT 2013 BY EUREKA GROUP TEXAS RETAIL SURVEY TEXAS STATE SALES REPORT & RANKINGS PERFORMANCE RANK GROWTH PERSISTENCE RELATIVE STRENGTH SALES RANK PER CAPITA SALES RANK STATE SALES% N.A. 0.0% 1.00 N.A. N.A. 100% OUTLET GROWTH LAST 5 YRS OUTLETS RANK % STATEWIDE OUTLETS POP. RANK PER OUTLET SALES RANK 1.7% N.A. 100% N.A. N.A. Market Share Gen Mrch 13.1% Apparel 5.5% 20% Rest & Bars 13.4% 10% Other 18.0% Gas Stn 14.4% 0% 1.7% 3.5% MEDIAN HSHOLD AGE SIZE 34 Annual Retail Growth 5 YR GROWTH RATES SALES POPULATION % STATEWIDE POPULATION 100% 2.75 $SALES PER HOUSEHOLD MOTOR VEH. & PARTS ELECTRONICS & APPL FURNITURE BUILDING MATRL GAS STATIONS APPAREL & ACCESSORY GEN MERCHANDISE RESTAURANTS & BARS TEXAS NORM $8,448 $980 $858 $2,045 $4,598 $1,772 $4,199 $4,269 TOTAL $31,955 -10% Build Matrl 6.4% Motor Vehicle 26.4% Furn 2.7% OUTLETS PER 10K POP 06 07 08 09 10 11 12 120 -20% PER CAPITA RETAIL SALES ($000) 10 11 SALES 81,389,590 8,266,501 9,440,245 19,704,081 3.0% 0.4% -2.4% 2.0% $2,958 $300 $343 $716 16,503,681 4,345,557 44,294,684 17,068,818 8,203,967 40,452,071 12,206,703 4,850,439 41,131,452 5.1% 3.7% 8.5% 3.9% 4.0% 0.7% 0.3% 15.8% 4.9% $600 $158 $1,610 $620 $298 $1,470 $444 $176 $1,495 291,531,997 307,857,789 3.5% $11,187 06 07 08 MOTOR VEH. & PARTS FURN & HOME FURN ELECTRONICS & APPL. BUILD. MATERIALS 61,136,199 6,324,039 8,894,491 15,478,909 62,767,941 7,304,456 9,547,635 16,857,707 66,331,530 7,690,805 10,099,086 16,868,407 61,429,031 7,378,960 9,869,626 17,261,973 52,454,287 6,546,020 8,136,976 15,326,660 61,349,041 6,679,016 8,389,146 15,756,099 67,718,480 7,098,398 9,310,219 16,728,206 77,073,475 7,828,126 8,939,626 18,659,167 FOOD & BEV. STORES DRUG/HEALTH STORES GASOLINE STATIONS APPAREL & ACCES. SPECIALTY STORES GEN MERCH. STORES MISC RETAILERS NONSTORE RETAILERS RESTAURANTS & BARS 10,485,576 3,255,776 23,501,597 11,685,109 5,936,418 30,225,822 11,463,551 1,380,174 26,293,443 11,260,482 3,294,178 26,155,951 12,792,603 6,273,461 33,914,947 11,193,724 1,757,568 28,483,291 12,179,760 3,430,608 27,837,979 13,372,337 6,399,176 37,024,615 11,401,675 2,205,992 30,594,988 13,103,094 3,650,801 32,276,367 13,438,492 6,703,270 37,775,793 10,429,438 2,530,365 32,344,798 13,569,793 3,472,918 26,000,019 12,823,432 6,693,859 36,233,055 10,537,161 2,613,235 32,077,470 13,857,262 3,502,550 30,298,647 13,498,240 6,851,968 36,283,352 10,957,887 2,890,049 33,373,417 14,670,103 3,817,800 35,938,449 14,696,494 7,284,431 36,958,645 11,000,555 3,282,759 35,743,098 15,628,486 4,115,110 41,945,723 16,163,653 7,768,908 38,306,886 11,559,378 4,593,219 38,950,238 216,061,105 231,603,944 245,436,958 248,192,011 226,484,884 243,686,674 264,247,639 RETAIL SALES TOTAL 09 GROWTH 05 12 13 PER OUTLET SALES 1.5% -0.9% -2.2% -0.7% $4,348,047 $748,673 $838,929 $1,996,060 17,162 9,810 13,470 33,368 18,268 14,282 53,863 32,382 71,628 17,488 9,996 13,726 34,002 18,615 14,553 54,886 32,997 72,989 2.4% 1.6% -0.6% 2.2% 2.0% 1.7% -2.2% 11.8% 3.1% $910,645 $419,481 $3,114,011 $484,406 $425,274 $2,682,179 $214,607 $141,845 $543,785 307,618 312,419 318,355 1.7% $933,144 11 12 13 06 07 08 MOTOR VEH. & PARTS FURN & HOME FURN ELECTRONICS & APPL. BUILD. MATERIALS 15,399 10,536 11,827 9,449 15,779 10,829 12,048 9,589 16,481 10,945 11,880 9,665 16,206 10,507 11,283 9,496 16,562 10,276 11,079 9,396 16,791 10,109 10,796 9,298 17,599 10,347 10,873 9,446 17,726 10,456 10,656 9,348 FOOD & BEV. STORES DRUG/HEALTH STORES GASOLINE STATIONS APPAREL & ACCES. SPECIALTY STORES GEN MERCH. STORES MISC RETAILERS NONSTORE RETAILERS RESTAURANTS & BARS 13,769 7,910 15,392 28,530 17,660 10,940 67,687 11,515 58,294 14,679 8,635 14,542 29,262 16,758 12,059 63,200 13,602 59,709 15,210 9,041 13,916 29,877 16,566 13,154 60,249 18,515 61,507 15,436 9,194 13,636 29,225 16,100 12,898 55,927 21,051 62,097 15,923 9,467 13,450 29,726 16,820 13,264 54,657 23,629 64,152 16,374 9,074 13,280 30,269 17,288 13,279 53,335 25,933 66,337 16,907 9,554 13,262 32,614 18,087 14,054 54,818 30,408 69,649 RETAIL OUTLETS TOTAL 278,908 280,691 287,006 283,056 288,400 292,163 CITY TREND (YR) 05 06 07 08 09 10 POPULATION (000) 22,880 23,525 23,902 24,308 24,706 $774,668 $825,121 $855,163 $876,830 $785,315 Summary: During the past 5 yrs, statewide retail sales have grown 3.5%. In 2006 & 2007, sales growth experienced steady increases. In 2008, the growth rate fell to 1.1%. By 2009, growth turned negative, with retail sales declining by 8.7%. In 2010, sales bounced back with an increase of 7.6%, followed by a 8.4% increase in 2011 and 10.3% in 2012. Over the past 5 years, the number of retail outlets have increased by 1.7% annually. TEXAS RETAIL SURVEY SECTION A 10 18,063 10,655 10,858 9,526 05 SALES PER OUTLET($) 09 GROWTH RETAIL OUTLETS 25,146 $834,078 11 25,632 $859,012 12 26,059 $933,144 13 26,494 $967,027 5 YR GROWTH 1.7% 1.8% The highest market share sector is Motor Vehicles & Parts, accounting for 26.4% of retail sales, followed by the General Merchandise sector, with a market share of 13.1% of total retail sales. Note: Growth Rates are annual for period 2007-2012. Sales & outlet data for 2013 are forecasts and subject to future adjustment. COPYRIGHT 2013 BY EUREKA GROUP RATING (ABOVE AVG) ANDERSON COUNTY SALES REPORT & RANKINGS PERFORMANCE RANK GROWTH PERSISTENCE RELATIVE STRENGTH SALES RANK PER CAPITA SALES RANK STATE SALES% 2 71.4% 1.05 67 128 0.14% OUTLET GROWTH LAST 5 YRS OUTLETS RANK % STATEWIDE OUTLETS POP. RANK PER OUTLET SALES RANK -0.1% 74 0.17% 56 65 Market Market Share Share OTHER 11.0% GAS STN Build 16.8% Matrl Furn 9.0% BUILD. MATRL1.2% FURN 10.7% 1.2% 39 Other 9.6% Motor MOTOR VehicleVEHICLE 31.4% 23.2% 03 06 04 07 05 08 06 09 07 10 08 11 09 12 COUNTY % STATEWIDE POPULATION 0.22% 2.57 $SALES PER HOUSEHOLD MOTOR VEH. & PARTS ELECTRONICS & APPL FURNITURE BUILDING MATRL GAS STATIONS APPAREL & ACCESSORY GEN MERCHANDISE RESTAURANTS & BARS 10% 12% 10% 8% 8% 6% 6% 4% 4% 2% 2% 0% 0% -2% -2% -4% -4% -6% -6% -8% -8% -10% -10% 0.6% 4.4% MEDIAN HSHOLD AGE SIZE Annual Annual Retail Retail Growth Growth GEN Gen MRCH Mrch 22.7% 18.0% REST. & Rest & BARS Bars 12.2% 10.5% APPARE Apparel L 1.6% 2.3% Gas Stn 18.7% 5 YR GROWTH RATES SALES POPULATION TOTAL #HOUSEHOLDS LOCAL MKT $6,083 $191 $239 $1,740 $3,618 $319 $3,484 $2,030 TEXAS NORM $8,448 $19,377 $31,955 $980 $858 $2,045 $4,598 $1,772 $4,199 $4,269 22,578 OUTLETS PER 10K POP 93 120 STATE COUNTY STATE PER CAPITA GROWTH SALES 137,334 5,395 4,312 39,278 11.3% 6.6% 2.6% 0.7% $2,274 $89 $71 $650 15,064 4,554 78,701 6,943 2,252 75,785 13,431 1,090 44,152 15,636 4,727 81,691 7,207 2,338 78,665 13,942 1,131 45,829 2.6% 3.3% 5.4% -3.4% 8.4% 0.9% -5.4% 35.7% 2.0% $259 $78 $1,352 $119 $39 $1,302 $231 $19 $759 380,865 421,469 437,484 4.4% $7,243 11 12 13 RETAIL SALES ($000) 05 06 07 08 09 10 11 12 13 MOTOR VEH. & PARTS FURN & HOME FURN ELECTRONICS & APPL. BUILD. MATERIALS 72,462 3,969 3,150 36,634 78,129 3,821 3,349 37,124 77,594 3,776 3,648 36,608 83,291 3,253 3,793 37,615 75,916 3,991 3,266 34,974 103,395 4,249 3,104 35,509 114,277 4,627 4,075 35,461 132,306 5,197 4,154 37,840 FOOD & BEV. STORES DRUG/HEALTH STORES GASOLINE STATIONS APPAREL & ACCES. SPECIALTY STORES GEN MERCH. STORES MISC RETAILERS NONSTORE RETAILERS RESTAURANTS & BARS 12,293 3,653 56,354 8,074 1,493 65,865 18,584 340 33,698 11,768 3,457 55,199 8,168 1,427 73,290 21,014 214 36,847 13,234 3,876 60,366 8,247 1,508 72,567 17,772 237 39,988 14,427 4,032 63,458 8,188 1,452 76,488 17,949 301 41,647 14,827 4,188 54,833 7,563 1,467 74,178 11,560 561 39,921 14,699 4,000 61,192 7,965 1,762 73,761 11,680 612 40,666 15,483 4,163 62,271 6,775 2,008 73,920 14,896 780 42,131 316,569 333,807 339,421 355,894 327,246 362,593 09 10 RETAIL SALES TOTAL PER OUTLET RETAIL OUTLETS 05 06 07 08 GROWTH SALES MOTOR VEH. & PARTS FURN & HOME FURN ELECTRONICS & APPL. BUILD. MATERIALS 38 15 12 28 36 14 11 25 37 13 10 22 35 15 9 23 35 15 8 23 34 17 7 20 34 16 9 19 35 17 10 17 36 17 11 18 -1.1% 5.5% 0.0% -5.0% $3,780,169 $305,708 $415,409 $2,225,880 FOOD & BEV. STORES DRUG/HEALTH STORES GASOLINE STATIONS APPAREL & ACCES. SPECIALTY STORES GEN MERCH. STORES MISC RETAILERS NONSTORE RETAILERS RESTAURANTS & BARS 23 17 43 34 23 19 187 17 91 23 18 41 34 23 22 179 19 98 25 21 38 33 26 23 167 36 90 28 21 34 32 29 25 148 42 88 31 16 35 29 26 26 147 40 88 29 14 35 30 29 30 129 45 87 30 14 32 36 25 31 136 54 96 29 12 36 40 26 26 131 54 106 30 12 35 41 26 27 132 55 107 3.0% -10.6% -1.1% 3.9% 0.0% 2.5% -4.7% 8.4% 3.3% $519,447 $379,517 $2,186,127 $173,571 $86,629 $2,914,804 $102,530 $20,180 $416,525 RETAIL OUTLETS TOTAL 547 543 541 529 519 506 532 539 547 -0.1% $781,945 CITY TREND (YR) 05 06 07 08 09 10 11 12 13 POPULATION 55,965 56,202 56,353 56,445 56,610 58,458 58,356 58,190 58,024 0.6% $578,736 $614,746 $627,395 $672,768 $630,531 $716,587 $715,912 $781,945 $799,789 4.5% SALES PER OUTLET($) Summary: The Performance Rank of 2, measuring sales growth in the most recent year, is above average. Over the past 10 yrs, the Growth Persistence Index (71.4%) has been high, while the 5 yr Relative Strength Ratio of 1.05 is above the state norm of 1.0. In total sales, the county's rank is 67, while the Per Capita Sales Rank is 128. Population Growth has averaged 0.6% over the past 5 yrs, compared to statewide norm of 1.7%. TEXAS RETAIL SURVEY 5 YR GROWTH Per Outlet Sales Rank is 65, representing avg sales per outlet of $781,945. The annual growth rate over the past 5 yrs for Per Outlet Sales has been 4.5%. Note: Growth Rates are annual for period 2007-2012. Sales & outlet data for 2013 are forecasts and subject to future adjustment. SECTION A COPYRIGHT 2013 BY EUREKA GROUP SECTION B LARGE CITIES RETAIL SALES REPORTS COPYRIGHT 2013 BY EUREKA GROUP TEXAS RETAIL SURVEY RATING (BELOW AVG) ABILENE (Jones) SALES REPORT & RANKINGS PERFORMANCE RANK GROWTH PERSISTENCE RELATIVE STRENGTH SALES RANK PER CAPITA SALES RANK STATE SALES% 4 4.8% 0.90 31 170 0.54% OUTLET GROWTH LAST 5 YRS OUTLETS RANK % STATEWIDE OUTLETS POP. RANK PER OUTLET SALES RANK -0.2% 27 0.47% 26 94 Apparel 4.2% Gen Mrch 18.0% Market Share 32 10% 5% Other 16.3% 0% Gas Stn 12.0% -5% Build Matrl 8.8% Motor Vehicle 24.5% Furn 2.2% 06 07 08 09 10 CITY 11 12 0.46% TOTAL -10% % STATEWIDE POPULATION 2.46 $SALES PER HOUSEHOLD MOTOR VEH. & PARTS ELECTRONICS & APPL FURNITURE BUILDING MATRL GAS STATIONS APPAREL & ACCESSORY GEN MERCHANDISE RESTAURANTS & BARS 15% 0.4% 1.4% MEDIAN HSHOLD AGE SIZE Annual Retail Growth Rest & Bars 13.9% 5 YR GROWTH RATES SALES POPULATION #HOUSEHOLDS LOCAL MKT 8,204 $709 $750 $2,945 $4,026 $1,413 $6,012 $4,666 TEXAS NORM $8,448 $33,489 $31,955 $980 $858 $2,045 $4,598 $1,772 $4,199 $4,269 48,884 -15% OUTLETS PER 10K POP 124 120 STATE PER CAPITA RETAIL SALES ($000) 05 06 07 08 09 10 11 12 13 MOTOR VEH. & PARTS FURN & HOME FURN ELECTRONICS & APPL. BUILD. MATERIALS 363,344 35,051 39,593 101,717 361,207 36,066 41,526 112,746 427,516 37,503 43,316 122,799 351,006 44,039 43,139 127,752 265,548 34,722 36,904 113,614 307,960 35,690 36,906 121,441 362,832 30,876 35,689 137,871 388,584 35,532 33,574 139,521 401,019 FOOD & BEV. STORES DRUG/HEALTH STORES GASOLINE STATIONS APPAREL & ACCES. SPECIALTY STORES GEN MERCH. STORES MISC RETAILERS NONSTORE RETAILERS RESTAURANTS & BARS 66,817 26,488 82,195 52,796 55,174 252,312 49,395 9,663 163,086 70,394 29,385 88,583 55,767 54,190 269,460 29,481 10,176 174,835 67,559 28,823 111,476 54,505 48,209 295,249 49,169 10,349 182,877 62,347 30,908 146,966 53,159 52,418 306,117 45,044 10,431 194,861 64,207 23,908 132,503 49,262 52,746 286,274 55,676 8,179 194,825 65,104 26,164 160,312 54,848 54,207 284,343 58,111 4,554 202,866 70,327 30,539 189,597 60,371 55,939 284,193 57,913 4,723 208,993 71,475 32,425 190,718 66,921 58,478 284,786 58,088 5,182 221,003 73,763 33,462 196,820 69,063 60,349 293,899 59,946 5,348 228,076 1,297,629 1,333,815 1,479,351 1,468,187 1,318,369 1,412,506 1,529,864 1,586,287 1,637,048 RETAIL SALES TOTAL 36,669 34,649 143,986 GROWTH SALES -1.9% -1.1% -5.0% 2.6% $3,260 $298 $282 $1,171 1.1% 2.4% 11.3% 4.2% 3.9% -0.7% 3.4% -12.9% 3.9% $600 $272 $1,600 $562 $491 $2,390 $487 $43 $1,854 1.4% $13,310 PER OUTLET RETAIL OUTLETS 05 06 07 08 09 10 11 12 13 GROWTH SALES MOTOR VEH. & PARTS FURN & HOME FURN ELECTRONICS & APPL. BUILD. MATERIALS 104 49 50 44 107 47 48 49 112 45 45 48 109 48 44 45 105 46 46 41 94 49 49 42 94 47 50 45 93 47 49 46 94 48 50 47 -3.6% 0.9% 1.7% -0.8% $4,178,323 $755,989 $685,193 $3,033,071 FOOD & BEV. STORES DRUG/HEALTH STORES GASOLINE STATIONS APPAREL & ACCES. SPECIALTY STORES GEN MERCH. STORES MISC RETAILERS NONSTORE RETAILERS RESTAURANTS & BARS 88 61 69 149 129 47 338 50 299 91 65 71 145 118 48 321 63 310 76 62 81 155 108 54 319 83 307 60 58 89 156 99 50 315 88 313 60 54 90 149 98 45 330 80 309 58 49 91 143 94 45 316 73 309 61 50 94 148 97 47 327 81 323 64 48 93 150 92 43 327 88 341 65 49 94 152 93 44 332 89 346 -3.4% -5.0% 2.8% -0.7% -3.2% -4.5% 0.5% 1.2% 2.1% $1,116,802 $675,517 $2,050,726 $446,141 $635,631 $6,622,938 $177,638 $58,884 $648,104 1,477 1,483 1,495 1,474 1,453 1,412 1,464 1,481 1,503 -0.2% $1,071,092 RETAIL OUTLETS TOTAL 05 CITY TREND (YR) POPULATION SALES PER OUTLET($) 06 07 08 09 10 11 115,792 115,914 116,670 116,732 116,818 117,063 118,117 $878,557 $899,403 $989,532 $996,056 $907,343 $1,000,358 $1,044,989 Summary: The Performance Rank of 4, measuring sales growth in the most recent year, is below average. Over the past 10 yrs, the Growth Persistence Index (4.8%) has been low, while the 5 yr Relative Strength Ratio of 0.90 is below the state norm of 1.0. In total sales, the city's rank is 31, while the Per Capita Sales Rank is 170. Population Growth has averaged 0.4% over the past 5 yrs, compared to statewide norm of 1.7%. TEXAS RETAIL SURVEY 12 119,180 13 5 YR GROWTH 120,254 0.4% $1,071,092 $1,089,187 1.6% Per Outlet Sales Rank is 94, representing avg sales per outlet of $1,071,092. The annual growth rate over the past 5 yrs for Per Outlet Sales has been 1.6%. Note: Growth Rates are annual for period 2007-2012. Sales & outlet data for 2013 are forecasts and subject to future adjustment. SECTION A COPYRIGHT 2013 BY EUREKA GROUP SECTION C SUMMARY COUNTY RANKINGS & INDICES COPYRIGHT 2013 BY EUREKA GROUP TEXAS RETAIL SURVEY COUNTY RETAIL MARKETS SUMMARY OF RANKINGS & INDICIES PERFORMANCE RANK GROWTH PERSISTENCE SALES RANK PER CAPITA SALES RANK % STATEWIDE SALES SALES GROWTH LAST 5 YRS POP GROWTH LAST 5 YRS ANDERSON 2 71.4% ANDREWS 5 57.1% 1.05 67 128 0.145% 4.43% 0.64% 1.26 126 89 0.050% 8.35% ANGELINA 3 14.3% 3.89% 0.90 41 63 0.306% 1.26% ARANSAS 3 1.15% 23.8% 1.00 98 83 0.075% 3.53% ARCHER 0.50% 3 52.4% 0.76 176 165 0.017% -1.99% -0.89% ARMSTRONG 5 14.3% 0.86 247 249 0.001% 0.51% -1.37% ATASCOSA 1 90.5% 1.39 68 98 0.139% 10.58% 1.52% AUSTIN 5 47.6% 0.92 108 151 0.062% 1.87% 1.10% BAILEY 3 0.0% 0.68 207 220 0.007% -4.25% 1.34% BANDERA 5 9.5% 0.73 166 215 0.022% -2.69% 0.29% BASTROP 1 52.4% 0.98 46 71 0.249% 3.05% 0.67% BAYLOR 3 4.8% 0.66 213 185 0.006% -4.72% -1.19% BEE 1 85.7% 1.18 88 115 0.087% 7.07% 0.91% BELL 1 76.2% 1.07 15 42 1.277% 4.87% 3.28% BEXAR 2 76.2% 1.02 4 32 7.509% 3.87% 2.49% BLANCO 5 61.9% 1.09 170 172 0.020% 5.21% 1.88% BORDEN 2 61.9% 0.61 251 251 0.000% -6.13% -2.52% BOSQUE 5 14.3% 0.80 175 224 0.018% -1.09% -0.26% BOWIE 4 23.8% 0.95 38 28 0.400% 2.40% 0.19% BRAZORIA 3 28.6% 0.94 20 105 0.934% 2.29% 2.06% BRAZOS 4 28.6% 0.95 28 68 0.682% 2.55% 2.28% BREWSTER 5 23.8% 0.93 163 132 0.023% 2.01% 0.13% BRISCOE 5 28.6% 0.34 242 240 0.001% -16.42% -0.19% BROOKS 5 33.3% 0.93 171 111 0.020% 1.94% -0.93% BROWN 5 19.0% 0.84 80 104 0.109% -0.05% 0.08% BURLESON 3 57.1% 0.94 142 157 0.036% 2.22% 0.17% BURNET 1 66.7% 0.95 54 31 0.184% 2.42% 0.94% CALDWELL 2 85.7% 1.21 79 106 0.111% 7.47% 1.61% CALHOUN 4 28.6% 1.03 117 117 0.057% 4.09% 0.67% CALLAHAN 1 81.0% 1.47 167 182 0.022% 11.85% -0.05% CAMERON 4 23.8% 0.95 16 126 1.044% 2.38% 1.21% CAMP 3 14.3% 0.80 153 154 0.027% -1.11% -0.22% CARSON 4 52.4% 1.02 188 155 0.013% 3.84% 0.08% CASS 3 66.7% 1.21 95 122 0.078% 7.59% -0.24% CASTRO 3 38.1% 1.05 200 207 0.010% 4.51% 1.59% CHAMBERS 3 23.8% 0.94 102 168 0.070% 2.33% 1.90% CHEROKEE 5 19.0% 0.86 85 166 0.100% 0.47% 0.95% CHILDRESS 1 42.9% 1.16 154 51 0.026% 6.64% -0.49% CLAY 2 28.6% 0.85 160 149 0.024% 0.12% 0.85% COCHRAN 4 14.3% 0.91 233 236 0.002% 1.46% -1.58% COKE 5 23.8% 1.09 227 225 0.003% 5.40% -0.52% COLEMAN 4 19.0% 0.91 177 171 0.016% 1.48% -0.02% COLLIN 2 76.2% 1.03 6 19 3.879% 4.11% 2.68% COLLINGSWORTH 3 28.6% 0.95 226 219 0.003% 2.54% 0.13% COLORADO 3 23.8% 0.98 110 97 0.062% 3.13% 0.00% COMAL 2 95.2% 1.21 33 33 0.476% 7.50% 1.52% COMANCHE 3 14.3% 0.93 162 181 0.023% 2.03% -0.58% CONCHO 3 57.1% 1.13 211 190 0.006% 6.01% 1.38% COOKE 2 71.4% 1.02 58 24 0.171% 3.88% 0.33% CORYELL 5 33.3% 0.80 76 191 0.117% -1.11% 0.46% COTTLE 4 23.8% 1.18 243 239 0.001% 7.07% -0.71% CRANE 5 57.1% 1.08 210 200 0.006% 5.17% 3.12% CROCKETT 1 57.1% 1.23 202 143 0.009% 7.96% -2.22% CROSBY 5 33.3% 0.10 220 238 0.004% -34.40% -1.06% CULBERSON 4 57.1% 1.06 137 1 0.042% 4.79% -2.20% DALLAM 4 38.1% 0.99 151 40 0.028% 3.24% 2.27% DALLAS 4 0.0% 0.85 2 38 9.823% 0.18% 0.74% DAWSON 2 66.7% 1.03 149 153 0.029% 4.20% -0.54% DE WITT 1 81.0% 1.65 103 76 0.047% 14.40% 0.14% DEAF SMITH 4 33.3% 0.94 130 131 0.002% 2.25% 0.72% DELTA 1 42.9% 1.01 234 248 2.061% 3.78% -0.06% DENTON 2 95.2% 1.03 9 103 0.067% 4.03% 2.84% DICKENS 5 28.6% 0.75 231 222 0.002% -2.24% -2.75% DIMMIT 1 81.0% 2.40 124 15 0.051% 23.27% 1.08% DONLEY 4 33.3% 1.22 216 195 0.005% 7.74% -1.97% DUVAL 1 85.7% 2.32 140 77 0.038% 22.46% -1.09% COUNTY TEXAS RETAIL SURVEY RELATIVE STRENGTH SECTION C COPYRIGHT 2013 EUREKA GROUP SECTION D SUMMARY CITY RANKINGS & INDICES COPYRIGHT 2013 BY EUREKA GROUP TEXAS RETAIL SURVEY CITY RETAIL MARKETS SUMMARY OF RANKINGS & INDICIES CITY PERFORMANCE RANK Abilene Addison Alamo Alamo Heights Alice Allen Alpine Alvin Amarillo Andrews Angleton Aransas Pass Arlington Athens Atlanta Austin Azle Balch Springs Balcones Heights Bandera Bastrop Bay City Baytown Beaumont Bedford Bee Cave Beeville Bellaire Bellmead Belton Benbrook Beverly Hills Big Spring Boerne Bonham Borger Bowie Brady Brazoria Breckenridge Brenham Bridge City Bridgeport Brownfield Brownsville Brownwood Bryan Buda Bulverde Burkburnett Burleson Burnet Caldwell Cameron Canton Canyon Carrizo Springs Carrollton Carthage Castle Hills Cedar Hill Cedar Park Center Childress Clear Lk. Shores Cleburne TEXAS RETAIL SURVEY GROWTH PERSISTENCE RELATIVE STRENGTH SALES RANK PER CAPITA SALES RANK % STATEWIDE SALES SALES GROWTH LAST 5 YRS POP GROWTH LAST 5 YRS 4 4.8% 0.90 31 170 0.54% 1.41% 0.43% 1 57.1% 1.02 79 24 0.19% 3.94% 2.02% 2 57.1% 1.07 172 226 0.07% 5.01% 1.53% 3 0.0% 0.79 288 255 0.02% -1.36% 0.08% 3 52.4% 1.06 119 122 0.11% 4.75% 0.43% 3 71.4% 1.49 54 222 0.32% 12.06% 3.15% 5 28.6% 0.95 295 237 0.02% 2.38% 1.02% 5 19.0% 0.57 104 141 0.13% -7.48% 1.17% 5 33.3% 0.91 11 124 1.08% 1.65% 0.85% 5 57.1% 1.31 206 187 0.05% 9.30% 4.32% 3 28.6% 0.88 157 199 0.08% 1.00% 1.08% 2 57.1% 1.10 150 42 0.08% 5.52% 0.17% 4 19.0% 0.91 8 188 1.57% 1.52% 0.99% 2 52.4% 1.02 152 108 0.08% 4.01% 0.67% 2 95.2% 1.37 192 41 0.06% 10.23% -0.21% 2 23.8% 0.96 4 151 4.07% 2.62% 2.66% 3 23.8% 1.14 191 158 0.06% 6.24% 1.05% 5 28.6% 0.92 154 243 0.08% 1.70% 3.29% 5 57.1% 0.72 233 20 0.04% -3.11% -2.29% 3 23.8% 0.96 321 28 0.01% 2.73% -4.36% 2 52.4% 0.84 87 10 0.16% -0.12% 0.37% 4 38.1% 0.87 169 202 0.07% 0.63% 0.39% 2 66.7% 0.92 46 153 0.37% 1.87% 0.96% 4 23.8% 0.85 23 134 0.62% 0.26% 1.28% 5 38.1% 0.58 96 252 0.15% -7.19% 1.03% 1 76.2% 1.27 121 5 0.11% 8.56% 8.16% 1 100.0% 1.19 166 130 0.07% 7.09% 1.39% 4 23.8% 0.89 255 308 0.03% 1.11% 0.55% 5 23.8% 0.93 153 70 0.08% 2.10% 1.79% 1 38.1% 0.99 139 160 0.09% 3.24% 2.20% 3 57.1% 1.23 220 293 0.05% 7.95% 1.10% 4 9.5% 0.98 283 30 0.02% 3.00% 1.00% 2 85.7% 1.10 117 186 0.11% 5.56% 1.57% 2 61.9% 1.29 81 18 0.18% 8.89% 2.75% 5 9.5% 0.71 245 229 0.03% -3.36% -1.17% 2 9.5% 0.87 221 227 0.05% 0.69% 0.98% 4 33.3% 0.96 278 164 0.02% 2.56% -0.94% 3 47.6% 1.14 266 149 0.03% 6.16% 0.08% 5 33.3% 0.96 307 137 0.02% 2.68% 0.75% 5 23.8% 0.91 294 221 0.02% 1.49% -0.49% 4 23.8% 1.01 126 97 0.11% 3.73% 1.30% 3 14.3% 1.00 286 262 0.02% 3.46% 0.75% 4 52.4% 0.99 265 171 0.03% 3.36% 0.77% 1 52.4% 1.13 298 299 0.02% 6.06% 1.05% 3 0.0% 0.89 30 248 0.55% 1.18% 1.13% 5 19.0% 0.85 140 169 0.09% 0.25% -0.34% 4 42.9% 0.97 55 214 0.29% 2.92% 1.30% 1 71.4% 1.52 114 19 0.12% 12.53% 5.21% 3 52.4% 1.10 259 114 0.03% 5.41% 2.16% 5 33.3% 0.41 315 315 0.01% -13.52% -0.50% 3 52.4% 1.06 71 127 0.20% 4.79% 2.36% 5 38.1% 0.88 284 206 0.02% 0.83% 0.94% 1 66.7% 1.06 289 139 0.02% 4.65% 0.67% 4 14.3% 0.86 318 274 0.01% 0.32% -1.23% 3 9.5% 0.99 204 22 0.05% 3.20% 0.44% 4 28.6% 0.94 260 290 0.03% 2.34% 1.26% 1 81.0% 1.72 256 126 0.03% 15.32% 0.13% 5 23.8% 0.80 36 210 0.48% -1.07% 1.27% 3 52.4% 1.09 195 68 0.05% 5.37% 0.20% 4 14.3% 0.92 290 154 0.02% 1.72% 1.09% 5 23.8% 1.00 84 213 0.17% 3.52% 1.75% 2 81.0% 1.42 72 211 0.20% 11.00% 3.13% 5 28.6% 0.81 205 43 0.05% -0.86% -1.05% 1 42.9% 1.17 269 174 0.03% 6.87% -1.03% 4 28.6% 0.77 270 7 0.03% -1.87% -1.51% 5 28.6% 0.82 103 175 0.13% -0.46% 0.38% SECTION D COPYRIGHT 2013 EUREKA GROUP

© Copyright 2026