ABC

docz

Explore

Log in

Create new account

Download

Report

society

work

unions

P A R T I I Classical Theory: The Economy

What Is Economics? Economic Choices & Scarcity

Answer Key for Sample Questions for Midterm 2010

How To Save Smarter $AVINGS SURVIVAL GUIDE

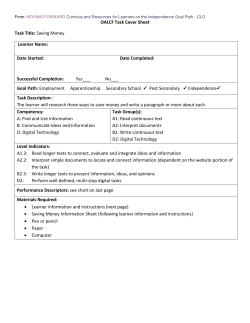

OALCF Task Cover Sheet Task Title: Learner Name:

Economics 151 Development Economics Sample Exam Questions

Solutions for Econ 290 Sample Midterm One

Math 112 Review: Probability & Calculus Problems

Document 221536

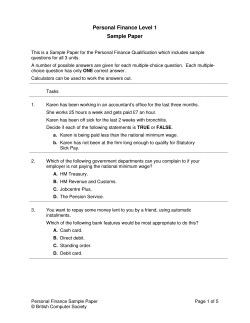

Personal Finance Level 1 Sample Paper

Access H-drive on Home or Public Library Computer

© Copyright 2026

About abcdocz

DMCA / GDPR

Report