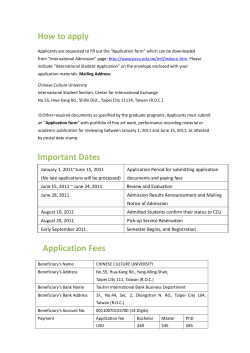

F I R