Bonus work: 3 Course: M339W/M389W - Financial Math for Actuaries

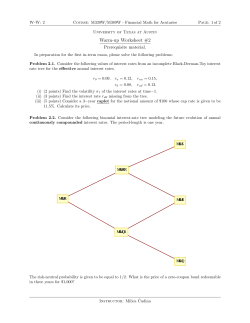

Bonus work: 3 Course: M339W/M389W - Financial Math for Actuaries Page: 1 of 2 University of Texas at Austin Quiz # 3 Log-normal stock prices. Provide your final answer only for the following problems. Problem 3.1. (5 pts) A non-dividend-paying stock is valued at $100.00 per share. The annual expected (rate of) return is 12.0% and the standard deviation of annualized returns is given to be 0.30. If the stock price is modeled using the lognormal distribution (as discussed in class), what is the probability that the time−2 stock price exceeds $95? (a) About 0.28 (b) About 0.50 (c) About 0.55 (d) About 0.68 (e) None of the above. Solution: (d) In our usual notation, it is given that S(0) = 100, α = 0.12 and σ = 0.30. As we have learned in class, the required probability can be expressed as P[S(2) > 95] = N (dˆ2 ) with N denoting the standard normal cumulative distribution function and S(0) 1 1 + (α − σ 2 ) · 2 = 0.474453. dˆ2 = √ ln 95 2 σ 2 Using the standard normal tables, we get N (dˆ2 ) = 0.682411. Problem 3.2. (5 points) A non-dividend-paying stock is valued at $100.00 per share. The annual expected (rate of) return is 12.0% and the standard deviation of annualized returns is given to be 0.30. If the stock price is modeled using the lognormal distribution (as discussed in class), what is the following conditional expectation? E[S(2) | S(2) > 95] (a) (b) (c) (d) (e) About 100 About 106 About 127 About 152 None of the above. Solution: (d) In our usual notation, it is given that S(0) = 100, α = 0.12 and σ = 0.30. As we have learned in class, the conditional expectation from above can be expressed as N (dˆ1 ) E[S(2) | S(2) > 95] = S(0)e2α . N (dˆ2 ) with N denoting the standard normal cumulative distribution function and 1 1 S(0) + (α + σ 2 ) · 2 = 0.898717, dˆ1 = √ ln 95 2 σ 2 √ ˆ ˆ d2 = d1 − σ 2 = 0.474453. Using the standard normal tables, we get N (dˆ1 ) = 0.815598 and N (dˆ2 ) = 0.682411. So, E[S(2) | S(2) > 95] = 151.936. Please, provide your complete solution to the following problem(s): ˇ Instructor: Milica Cudina Bonus work: 3 Course: M339W/M389W - Financial Math for Actuaries Page: 2 of 2 Problem 3.3. (10 points) A non-dividend-paying stock is valued at $75.00 per share. The annual expected (rate of) return is 16.0% and the standard deviation of annualized returns is given to be 0.30. If the stock price is modeled using the lognormal distribution (as discussed in class), what is the constant sU 1/2 such that P[S(1/2) > sU 1/2 ] ≤ 0.05. Solution: Note that the 95th percentile of the standard normal distribution equals 1.645. So, (0.16− 12 ×0.32 )× 12 +0.3× √12 ×1.645 sU 1/2 = 75e = 112.61. Problem 3.4. (10 points) A continuous-dividend-paying stock is valued at $75.00 per share. Its dividend yield is 0.03. The time−t realized (rate of) return is modeled as R(0, t) ∼ N (mean = 0.035t, variance = 0.09t) Find the probability that the time−4 stock price exceeds today’s stock price. Solution: We need to find P[S(4) > S(0)] with S(t) = S(0)eR(0,t) . Since R(0, t) follows the normal distribution with the above parameters, we have 0.035 × 4 R(0,4) P[S(4) > S(0)] = P[S(0)e > S(0)] = P[R(0, 4) > 0] = 1 − N − = N (0.23) = 0.591. 0.3 × 2 Problem 3.5. (10 points) A continuous-dividend-paying stock is valued at $75.00 per share. Its dividend yield is 0.03. The time−t realized (rate of) return is modeled as R(0, t) ∼ N (mean = 0.035t, variance = 0.09t) An investor purchases a single share of stock at time−0 and continuously and immediately reinvests any dividends received in the same asset. What are the mean and median values of the investor’s position at time−4? Solution: The expected rate of return (per annum) is 1 0.035 + × 0.09 = 0.035 + 0.045 = 0.08. 2 The mean is e4δ E[S(T )] = 75e4α = 75e0.32 = 103.285. Similarly, the median is 77e4×0.035 = 75 × 1.15027 = 86.2705. ˇ Instructor: Milica Cudina

© Copyright 2026