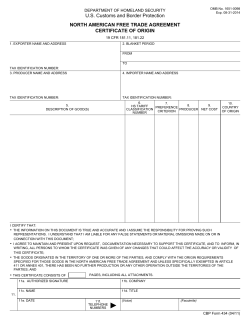

SINGAPORE-AUSTRALIA FREE TRADE AGREEMENT July 2009