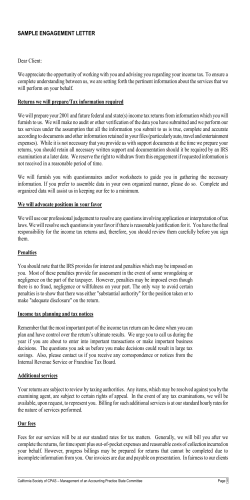

Circular 230: An Overview