RBCO NEWSLETTER January 2015

RBCO NEWSLETTER January 2015

Preface

The Narendra Modi government is set to unleash

several big-ticket announcements over the next few

weeks, starting with changes in the land acquisition

law through an ordinance, setting the stage for the

budget that will be unveiled at the end of February by

the finance minister . To define the success of ‘Make in

India’ campaign, to ease the clearance process, the

government favours expansion of the list of exempted

sectors under the land law to include defence,

education, healthcare and infrastructure.

Added to it, the FDI Policy review has been made in

Defence, Railways & Construction Sector increasing

Foreign Investment cap under the Automatic Route.

We have included a detailed note on the same.

Compounding of offences under Direct Tax laws also

requires special mention. Companies have to be aware

of the various amendments and updates to be legally

compliant and conduct effective business. We hope our

newsletter serves the purpose.

CA V.Thiagarajan

Partner

Corporate Law

the calender year with a minimum gap of

ninety days between the two meetings.

(viii) A small company need not include Cash

Flow Statement as part of its financial

statement.

(ix) Provision regarding mandatory rotation of

auditor/maximum term of auditor being 5

years in case of an individual and 10 years in

case of a firm of auditors is not applicable to

an OPC will apply to a small company as

well.

(x) They still have to maintain statutory

registers, minutes Books, books of account,

common seal, hold an annual general

meeting, have a registered office, have

minimum of two directors and two

shareholders.

MINISTRY OF CORPORATE AFFAIRS - INITIATIVES

IN THE LAST SIX MONTHS

Enhancing Efficacy of Companies Act, 2013

(i)

SMALL COMPANIES – A brief note

(i)

“Small Company” newly introduced by the

Companies Act, 2013.

(ii) Qualification : Paid Up Capital not more

than Rs.50 lakhs (OR) Turnover as per last

statement of P&L not exceeding Rs.2 crore.

(iii) Not applicable to (A) a holding company or

a subsidiary company; (B) a company

registered u/sec 8 of the Act; or (C) a

company or body corporate governed by

any special Act (D) public company.

(iv) Eligibility may be differ each year according

to applicability.

(v) Priveleges & exemptions available as

applicable to a one person company/

(vi) The annual return of a Small Company can

be signed by the company secretary alone,

or where there is no company secretary, by

a single director of the company.

(vii) May hold only two board meetings in a

year, i.e. one Board Meeting in each half of

R.Bupathy & Co.,

(ii)

(iii)

40 clarifications/elaborations have been

made in the form of circulars to remove

doubts

and

facilitate

smooth

implementation of Companies Act, 2013.

Fifteen amendments in various Companies

Rules have also been carried out to achieve

similar objectives.

In seven instances statutory orders to

'remove difficulties' have been issued for

smooth implementation of Companies Act,

2013.

To derive greater benefits of outcomes of

CSR initiatives, relevant rules have been

amended enabling wider spread of CSR

funding; new items eligible for funding have

also been added to provide impetus to

sanitation

and

environment-related

concerns.{Contribution to Swach Bharat

Mission & Clean Ganga Project included)

Providing Greater Clarity in Companies Act, 2013

for Ease of Doing Business

(iv)

To make Company Law even more business

and growth friendly amendments have

Page 1

RBCO NEWSLETTER January 2015

been moved and already approved by the

Lok Sabha to:

a.Bring provisions for minimum capital and

company seal at par with international best

practices.

b.Make approval for related party

transactions simpler without unduly

diluting

safeguards

for

minority

shareholders.

c.Provide explicit penalties for failure to

honour terms and conditions of deposits.

d. To retain the stringent bail provision for

the serious offences of fraud.

Unregistered Directors of Dormant Companies

(i)

Filing of appointment of Cost Auditors

(ii)

Simplification of forms and procedures for Easy

Compliance

(v)

To make compliances and reporting easy

and convenient to companies following

major initiatives have been taken:

a. Four prescribed forms have been

discontinued along with substitution of a

simple declaration instead of affidavits for

several purposes.

b. Procedural requirements for foreign

nationals to be Directors in Indian

Companies have been drastically reduced.

c. Arrangements have been completed for

integration of Name Availability, allotment

of Direct Identification Number (DIN),

Company

Incorporation

and

Commencement of Business with the

unified e-business portal being developed

by the Ministry of Industries and

Commerce.

d. Fee payable by small companies for

various services significantly reduced.

e. Arrangements to enable Indian

companies to follow new Accounting

Standards, i.e. IndAS (compatible with the

International Financial Reporting Standards

- IFRS) completed. This will facilitate access

for Indian companies to international

capital markets.

[Source - PRESS RELEASE, DATED 24-12-2014]

R.Bupathy & Co.,

Companies which do not have any of their

Directors/Signatory details registered in the

MCA21 system and who are desirous of

filing DIR-3C Form have been requested to

get atleast one authorised signatory

registered by contacting the concerned

Registrar of Companies.

In response to representation received from

stakeholders the Government has issued

clarification under Rule 5(1) & 6(2) of

Companies Cost Records and Audit Rules,

2014 regarding maintenance of cost records

and filing of notice of appointment of Cost

Auditor in Form CRA 2. Date of filing of said

form has been extended upto 31.1.2015

without penalty and late fee. Further

Companies that had filed Form 23C for

appointment of Cost Auditor for financial

year 2014-’15 need not file Form CRA 2

afresh.

[MCA General Circular No.42/2014 dated

12.11.2014]

DIRECT TAXES

Income Tax

Registration under FATCA to avoid TDS

(i)

(ii)

(iii)

India has entered into an Inter-Government

agreement with the United States of

America under Foreign Accounts Tax

Compliance Act (FATCA).

Government of India, has now advised that

to avoid withholding tax, Foreign Financial

Institutions (FFIs) in Model 1 jurisdictions,

such as India, need to register with IRS and

obtain a Global Intermediary Identification

Number (GIIN) before January 1, 2015.

The FFIs who have registered but have not

obtained a GIIN should indicate to the

withholding agents that the GIIN is applied

for, which may be verified by the

Page 2

RBCO NEWSLETTER January 2015

(iv)

withholding agents in 90 days. In this

regard, the FAQ published on the IRS

website (updated as on December 22,

2014), as received from the Government of

India, is furnished in the Annex.

[CIRCULAR NO DBR. AML. No. 9644

/14.07.018/2014-15, DATED 30-12-2014]

Also refer Circular DBOD. AML. No. 20472

/14.07.018/2013-14 dated June 27, 2014 on

the captioned subject.

[NOTIFICATION

NO.

GSR

863(E)

[F.NO.2/3/2014.NS-II], DATED 2-12-2014]

GUIDELINES FOR COMPOUNDING OF OFFENCES

UNDER DIRECT TAX LAWS, 2014

c.

SECTION 80C – DEDUCTIONS

a.

(i)

Reliance Retirement Fund notified

Reliance Retirement Fund set up by the

Reliance Mutual Fund registered with SEBI

is notified under section 80C deduction for

the assessment year 2015-16 and

subsequent

assessment

years.

NOTIFICATION

NO.

90/2014

[F.NO.

178/63/2012-ITA-I], DATED 23-12-2014

Sukanya Samriddhi Yojna notified

Sukanya Samriddhi Yojna is an exclusive

deposit scheme for a girl child.

(ii) The deposit in the said scheme is eligible for

Section 80C deduction.

(iii) It can be started in any Post Office or Banks.

(iv) The scheme can be started any time after

the child birth or before completing ten

years and to be continued till completion of

14 years.

(v) Maturity date is 21 years from date of

opening or marriage date of girl child

whichever is earlier.

(vi) Withdrawal upto 50% allowed only when

18 years for higher education.

(vii) Minimum contribution Rs.1000 per annum

in multiples of Rs.100 per month and

maximum upto Rs,1,50,000 per annum.

(viii) Interest rate to be notified by the

Government.

(ix) Interest payment is compounded upto 14

yrs thereafter option for monthly payout.

(x) There is no special tax benefit available.

d.

e.

b.

(i)

R.Bupathy & Co.,

f.

g.

In super session of all including the

guidelines issued vide F.No. 285/90/2008IT(Inv.)/12 dated 16th May 2008, new

guidelines are now issued for compliance by

all concerned to be effective from

01.01.2015 applicable to all applications for

compounding received on or after the

aforesaid date.

The applications received before 01.01.2015

shall continue to be dealt with in

accordance with the guidelines dated

16.05.2008.

Section 279(2) of the Act provides that any

offence under chapter XXII of the Act may,

either before or after the institution of

proceedings, be compounded by the

CCIT/DGIT.

Nature of offences:

For detailed provisions kindly refer the

below Circular.

LETTER [F.NO.285/35/2013 IT

(INV.V)/108, DATED 23-12-2014]

First Bilateral Advance Pricing Agreement

(i)

CBDT has signed its first Bilateral Advance

Pricing Agreement with Japan on

19.12.2014.

TDS from Salaries during FY 2014-15 u/sec 192

(i)

(ii)

The CBDT has issued Circular providing the

detailed income tax slabs and TDS

procedures

applicable

to

Salaried

Employees for the FY 2014-15.

Kindly

refer

CIRCULAR

NO.

17/2014[F.NO.275/192/2014-IT(B)], DATED

10-12-2014 for detailed reference

Page 3

RBCO NEWSLETTER January 2015

officers, as the procedure prescribed for

audit is essentially a procedure for

verification mandated in the statute.

[Refer Circular No. 181/7/2014-Service Tax

dated 10.12.2014]

INDIRECT TAXES

Mandatory Production of records and audit

reports for Service Tax Audit

(i)

(ii)

(iii)

(iv)

(v)

Rule 5(A)(2) has been substituted in the

Service Tax Rules, 1994 vide notification no.

23/2014-Service Tax dated 5th December,

2014. This rule, interalia, provides for

scrutiny of records by the audit party

deputed by the Commissioner. Such

scrutiny essentially constitutes audit by the

audit party consisting of departmental

officers. An Assessee is required to produce

the statutory records required to be

maintained under the Service tax Rules, and

also cost audit reports and income tax audit

reports to the audit parties.

Verification of records mandated by the

statute is necessary to check the correctness

of assessment and payment of tax by

the assessee in the present era of selfassessment.

Earlier Hon’ble High Court of Delhi in the

judgment dated 04.08.2014 in the case of

M/s Travelite (India) [2014-TIOL-1304-HCDEL-ST] had quashed rule 5A(2) of the

Service Tax Rules, 1994 on the ground that

the powers to conduct audit envisaged in

the rule did not have appropriate statutory

backing.

Following this, a new clause (k) was added

to sub-section (2) of section 94 following

amendment dated 06.08.2014, which deals

with rule making powers of the Central

Government which is reproduced below –

“(k) imposition, on persons liable to pay

service tax, for the proper levy and

collection of tax, of duty of furnishing

information, keeping records and the

manner in which such records shall be

verified.”

It may be noted that the expression

“verified” used in section 94(2)(k) of the

said Act is of wide import and would include

within its scope, audit by the departmental

R.Bupathy & Co.,

RBI/FEMA

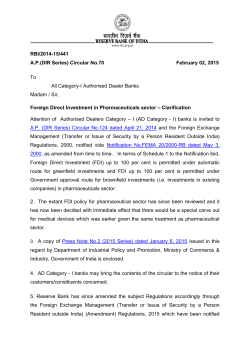

RBI HAS LIBERALISED OVERSEAS DIRECT INVESTMENT

BY INDIAN PARTY

(i)

(ii)

(iii)

(iv)

(v)

(vi)

Foreign Exchange Management (Transfer or

Issue of any Foreign Security) (Amendment)

Regulations, 2004 was issued under

Notification No. FEMA.120/RB-2004 dated

July 7, 2004 and further amended under

A.P. (DIR Series) Circular No. 96 dated

March 28, 2012.

In order to grant more flexibility to the

Indian party, it has been decided to further

liberalize certain regulations of the

Notification as detailed below.

Existing facility: Creation of charge on

shares of JV / WOS / step down subsidiary

(SDS) in favour of domestic / overseas

lender for the purpose of availing facilities

(funded or non-funded) by the Indian party

and / or the concerned JV / WOS is under

the automatic route.

Added facility: For the purpose of securing

the funded and / or non-funded facility to

be availed of by the Indian party or by its

group companies / sister concerns /

associate concerns or by any of its JV / WOS

/ SDS (irrespective of the level) under the

automatic route subject to the conditions

prescribed.

Creation of charge on the domestic assets in

favour of overseas lenders to the JV / WOS /

step down subsidiary which presently

requires prior approval of the Reserve Bank

has been added to the automatic route

subject to prescribed conditions.

Creation of charge on the overseas assets of

JV / WOS / SDS of an Indian party in favour

of a domestic lender to the Indian party or

to its group / sister / associate concern or to

Page 4

RBCO NEWSLETTER January 2015

any of its overseas JV / WOS / SDS which

presently requires prior approval of the

Reserve Bank has been added to the

automatic route subject to prescribed

conditions.

(vii) Important conditions: The loan / facility

availed by the JV / WOS / SDS from the

domestic / overseas lender shall be utilized

only for its core business activities overseas

and not for investing back in India in any

manner whatsoever;

(viii) A certificate from the Statutory Auditors’ of

the Indian party, to the effect that the loan

/ facility availed by the JV / WOS / SDS has

not been utilized for direct or indirect

investments in India, is to be obtained and

kept by the designated AD;

to the conditions specified in the Press Note

7 (2014 Series) dated August 26, 2014.

[A.P. (DIR SERIES 2014-15) CIRCULAR NO.

46, DATED 8-12-2014]

REVIEW OF FDI POLICY – SECTOR SPECIFIC

CONDITIONS- RAILWAY INFRASTRUCTURE

(i)

The extant Foreign Direct Investment (FDI)

policy for railways sector has also since

been reviewed. Department of Industrial

Policy and Promotion (DIPP) has now

permitted

100%

FDI

in

railway

Infrastructure sector under automatic route

subject to conditions. [A.P. (DIR SERIES

2014-15) CIRCULAR NO. 47, DATED 8-122014]

[Source: RBI/2014-15/371 A.P. (DIR Series)

Circular No.54 dated 29.12.2014]

REVIEW OF FDI POLICY – SECTOR SPECIFIC

CONDITIONS–CONSTRUCTION DEVELOPMENT

SECTOR

REPORTING ON NON-COOPERATIVE BORROWERS

(i)

(i)

RBI has issued advisory to all banks and

Financial Institutions to classify a borrower

as a co-operative or non-cooperative

borrower, to report and take stringent

measures on the latter.

[Circular DBR.NO.CID.BC.54/ 20.16.064/ 2014-15,

dated 22-12-2014]

FDI IN INDIA - REVIEW OF FDI POLICY - SECTOR

SPECIFIC CONDITIONS- DEFENCE

(ii)

The extant FDI policy for defence sector has

since been reviewed. Department of

Industrial Policy and Promotion (DIPP) has

now provided a list of defence items as

finalised by Department of Defence

Production, Ministry of Defence and has

clarified that items not in the list would not

require industrial license for defence

purposes. Further, on a review, effective

from

August

26,

2014,

foreign

investment i.e. FDI, FIIs, RFPIs, NRIs, FVCIs

and QFIs upto 49% under government route

shall be permitted in defence sector subject

R.Bupathy & Co.,

(ii)

(iii)

Under the Consolidated FDI Policy Circular

of 2014', effective from 17th April, 2014,

relating to Construction Development

Sector 100% equity participation under the

Automatic Route was allowed to FDI in

Townships, housing, built-up infrastructure

and construction-development projects

(which would include, but not be restricted

to, housing, commercial premises, hotels,

resorts, hospitals, educational institutions,

recreational facilities, city and regional level

infrastructure)

Under the revised FDI Policy review

Construction-development projects would

include development of townships,

construction of residential/commercial

premises, roads or bridges, hotels, resorts,

hospitals,

educational

institutions,

recreational facilities, city and regional level

infrastructure, townships.

Investment will be subject to the following

conditions:

A. Minimum area to be developed under

each project would be as under:

Page 5

RBCO NEWSLETTER January 2015

B.

C.

D.

E.

a. In case of development of

serviced plots, no minimum land

area requirement.

b. In

case

of

constructiondevelopment projects, a minimum

floor area of 20,000 sq. meter.

Investee company will be required to

bring minimum FDI of US$ 5 million

within six months of commencement

of the project. The commencement of

the project will be the date of approval

of the building plan/lay out plan by the

relevant

statutory

authority.

Subsequent tranches of FDI can be

brought till the period of ten years

from the commencement of the

project or before the completion of

project, whichever expires earlier.

(i) The investor will be permitted to

exit on completion of the project or

after

development

of

trunk

infrastructure i.e. roads, water supply,

street lighting, drainage and sewerage.

(ii) The Government may, in view of

facts and circumstances of a case

permit repatriation of FDI or transfer of

stake by one non-resident investor to

another non-resident investor, before

the completion of project. These

proposals will be considered by FIPB on

case to case basis inter-alia with

specific reference to Note (i).

The project shall conform to the norms

and standards, including land use

requirements

and provision of

community amenities and common

facilities, as laid down in the applicable

building control regulations, bye-laws,

rules, and other regulations of the

State

Government/Municipal/Local

Body concerned.

The Indian investee company will be

permitted to sell only developed plots.

For the purposes of this policy

"developed plots" will mean plots

R.Bupathy & Co.,

F.

G.

where trunk infrastructure i.e. roads,

water supply, street lighting, drainage

and sewerage, have been made

available.

The Indian investee company shall be

responsible for obtaining all necessary

approvals, including those of the

building/layout plans, developing

internal and peripheral areas and other

infrastructure facilities, payment of

development, external development

and other charges and complying with

all other requirements as prescribed

under

applicable

rules/byelaws/regulations

of

the

State

Government/Municipal/Local

Body

concerned.

The State Government/ Municipal/

Local Body concerned, which approves

the building/development plans, will

monitor compliance of the above

conditions by the developer.

NOTE: The following additional points need

attention

FDI not permitted in real estate/farm/TDRs

(iv)

(v)

It is clarified that FDI is not permitted in an

entity which is engaged or proposes to

engage in real estate business, construction

of farm houses and trading in transferable

development rights (TDRs).

Real estate business" will have the same

meaning as provided in FEMA Notification

No. 1/2000-RB dated May 03, 2000 read

with RBI Master Circular i.e. dealing in land

and immovable property with a view to

earning profit or earning income therefrom

and does not include development of

townships,

construction

of

residential/commercial premises, roads or

bridges,

educational

institutions,

recreational facilities, city and regional level

infrastructure, townships.

Page 6

RBCO NEWSLETTER January 2015

Minimum Area & Investment, Exit policy

not to apply to the following:

(vi)

(xii)

The conditions at (A) to (C) above, will not

apply to Hotels & Tourist resorts, Hospitals;

Special Economic Zones (SEZs); Educational

Institutions, Old Age Homes and Investment

by NRIs.

Minimum Area & Investment not applicable

if 30% invested in low cost affordable

housing

(vii)

100% FDI for maintenance

SEBI provides single registration for Depository

participants

(i)

The conditions at (A) and (B) above, will

also not apply to investee/joint venture

companies which commit at least 30

percent of the total project cost for low cost

affordable housing.

(ii)

Other points

(viii) An Indian company, which is the recipient

of FDI, shall procure a certificate from an

architect empanelled by any Authority,

authorized to sanction building plan to the

effect that the minimum floor area

requirement has been fulfilled.

(ix) 'Floor area' will be defined as per the local

laws/regulations of the respective State

governments/Union territories.

(x)

Completion of the project will be

determined as per the local bye-laws/rules

and

other

regulations

of

State

Governments.

It is clarified that 100% FDI under automatic

route is permitted in completed projects for

operation and management of townships,

malls/shopping complexes and business

centres.

(iii)

Notification

No.

LAD-NRO/GN/201415/18/1952 dated December 24, 2014

amending the SEBI (Depositories and

Participants) Regulations, 1996 (hereinafter

referred to as DP Regulations) providing for

single

registration

for

Depository

participants.

As per the amendment, the existing

requirement of obtaining certificate of

initialregistration to act as a participant and

subsequently permanent registration to

continue to act as a participant for each

depository has been done away with.

Henceforth, one certificate of initial

registration and subsequently permanent

registration through any depository shall be

required after commencement of the

Securities and Exchange Board of India

(Depositories

and

Participants)

(Amendment) Regulations, 2014.

[SEBI CIR/ MIRSD/5/ 2014 dated

30.12.2014]

Affordable Housing Projects

(xi)

Project using at least 40% of the FAR/FSI for

dwelling unit of floor area of not more than

140 square meter will be considered as

Affordable Housing Project for the purpose

of FDI policy in Construction Development

Sector. Out of the total FAR/FSI reserved for

Affordable Housing, at least one-fourth

should be for houses of floor area of not

more than 60 square meter.

R.Bupathy & Co.,

Page 7

RBCO NEWSLETTER January 2015

CLIENT AWARENESS CORNER

Refund of accumulatedCenvat Credit for export of

services/goods under Rule 5 of Cenvat Credit

Rules, 2004read with NotificationNo: 05/06 CE

(NT)dated 14.03.2006

1. Refund application in Form A as annexed with

the said notification.

2. Copy of the relevant Shipping Bills or Bills of

Export duly certified by the officer of customs to

the effect that the goods have in fact been

exported(in case of final products).

3. Copy of invoices issued by the input service

providers.

4. Copy of invoices for services exported.

5. Certificate from the bank certifying realization

of export proceeds (in caseof export of output

services).

6. Relevant extracts of the records maintained

under the Central ExciseRules, cenvat credit rules

or service tax rules, in original, evidencing taking

ofCENVAT credit, utilization of such credit in

payment of excise duty or servicetax and the

balance unutilized credit during the given period.

7. Statement of input invoices showing details of

payment of service tax andamount claimed.

8. The Table given in (DD) as provided under the

Notification 07/2010-CE(NT) dated 27.02.10, duly

certified by a person authorized by the Board

ofDirectors(in the case of a limited company) or

the proprietor or any partner(in case of

partnership firm) if the amount of refund claimed

is less than Rs. 5lakh, the Table shall also be

certified by the Chartered Accountant whoaudits

the annual accounts of the exporter for the

purposes of CompaniesAct, 1956 or the Income

Tax Act, 1961, as the case may be, if the amount

ofrefund claimed is more than Rs. 5lakh.

9. Declaration certifying the correctness of the

particulars given by the claimant.

Refund claim of service tax under section 11B of

CEA, 1944 read with section 83 of the Finance Act,

1994.

1. Application in prescribed Form –R.

2. Copy of TR-6/ GAR-7/PLA/ copy of return

evidencing payment of duty.

3. Copy of invoices (in original)

4. Documents evidencing that duty has not been

passed on to the buyer.

5. Any other document in support of the refund

claim.

6. Any other document as prescribed by the

Central Excise Officer.

“Courage is resistance to fear, mastery of

fear- not absence of fear”

- Mark Twain

Disclaimer: The contents of this newsletter do not constitute an opinion or professional advice. The information in

this publication has been obtained or derived from sources believed by RBCO to be reliable but does not guarantee

that it is accurate or complete. The users of this document are advised to seek independent professional opinion

before taking any course of action or decision. Also, the contents are not exhaustive. Kindly see the referred

provisions, Circulars/Notifications etc., for full text.

R.Bupathy & Co.,

Page 8

© Copyright 2026