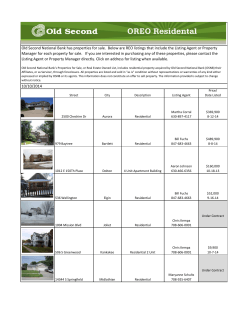

Residential