ABC

docz

Explore

Log in

Create new account

Download

Report

business and industrial

company

annual report

Nok Airlines (NOK TB) แนวโน้มฟื้นตัวในปี 2558

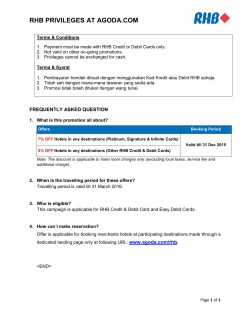

RHB PRIVILEGES AT AGODA.COM

Sembcorp Marine Buy

OUE Hospitality Trust Neutral Potential Competition From Hotel Jen

Ezion Holdings Buy

Vard Holdings Sell

China South City Buy 2QFY15 Contracted Sales On Track

Regional Daily Ideas Troika Top Stories

Regional Daily Ideas Troika

Morning Matters - RHB OSK Securities (Thailand)

Regional Daily Ideas Troika

© Copyright 2026

About abcdocz

DMCA / GDPR

Report