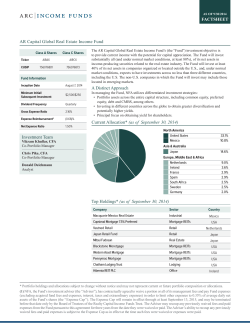

ANNUAL REPORT - Brown Capital Management