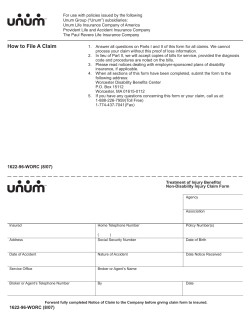

2014 Annual Report - Investors