Morningstar`s Dividend Playbook

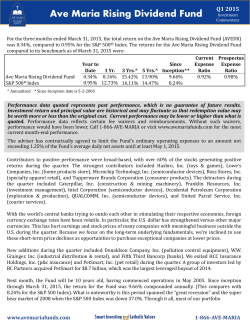

Morningstar’s Dividend Playbook Josh Peters, CFA Director of Equity-Income Strategy Editor, Morningstar DividendInvestor ©2015 Morningstar, Inc. All rights reserved. Introduction to Morningstar DividendInvestor g Josh Peters, CFA is Morningstar’s director of equity-income strategy, the founding editor of DividendInvestor, and manager of its Dividend Select model portfolio g Launched in January 2005 g Released companion book in 2008: The Ultimate Dividend Playbook g Received over 1,200 dividends thus far from our active portfolio holdings—all of which reflect actual, trades in real money, Morningstar-funded brokerage accounts g Received 398 dividend increases since inception; just 16 dividend cuts 2 Why Dividends? gPractical advantages for investors /For retirees, cash to fund regular portfolio withdrawals without having to sell shares /For savers, cash funds income growth/wealth accumulation through reinvestment /Better class of companies—typically well-established, defensive, financially healthy /Makes stocks easier to analyze and easier to own gMuch-needed discipline for issuers /Demonstrates ability willingness to reward shareholders directly /Represents a long-term commitment, enabling investors to return the favor /Helps block potentially self-serving or dubious allocations of capital gDividends are the ultimate source of security values /Bottom line is cash flow—not just to the firm, but directly to the investor 3 Best Reason of All: Superior Performance g Numerous academic studies show that high-yielding stocks outperform the market over the long run g Our study: Highest 30% of yields beat the market in 53 of 60 rolling 10-year CAGRs beginning in 1945 /Average beat of 206bp per year—or an extra $575 after 10 years on each $1,000 invested U.S. Market Total Return 30% Highest Dividend Yields 24% 19% 14% 9% 4% -1% 1955 1965 1975 1985 1995 Annual data 1945-2014. Source: Data from Kenneth R. French (http://mba.tuck.dartmouth.edu/pages/faculty/ken.french/data_library.html), Morningstar analysis. 4 2005 Step 1: Defining an Investable Universe g While the S&P 500 pays only 2.0%, much higher yields are available, especially in certain sectors— consumer staples (2.6%), energy (2.9%), utilities (3.6%) and telecommunications (4.9%) g Heavy share buybacks and/or rapid dividend growth without a decent yield are no substitute for adequate current income g Our basic stock screening parameters: Premium Stock Screener available at http://screen.morningstar.com/AdvStocks/Selector.html#AnchorSelector, results as of 3/19/2015. 5 Step 2: The Dividend Drill 6 The Dividend Drill: Is It Safe? g Dividend safety is the number-one priority for income investors— more than interest rates, changes in economic trends, even valuations g How to avoid dividend cuts: /Economic moats, which defend profitability and cash generation /Healthy balance sheets /Payout ratios that balance income against internal reinvestment needs and a cyclical safety margin /Continued dividend growth is the best indicator of safety, though even this isn’t perfect ... Our Record: Outcomes by Dividend Action Increased Dividends (89% positive returns) Flat Dividends (71% positive returns) 350% 300% 250% 200% 150% Reduced Dividends (19% positive returns) 100% 50% 0% -50% -100% Outcomes reflect realized total returns for full holding periods of each active DividendInvestor portfolio position. Data through 3/19/2015. Source: Morningstar 7 The Dividend Drill: Will It Grow? g Dividend growth drives total return by: /Furnishing additional income over time /Encouraging long-term capital appreciation g Key drivers of dividend growth: /Earnings growth: Consider volume expansion, pricing power, future for operating margins, role of acquisitions/share repurchases /Dividend policy: Will dividends rise faster/slower/equal to per-share earnings? g Useful approach: “extend the trend” /Latest 5- or 10-year rate as a stepping-off point for consideration of future performance Data as of 3/19/2015. Source: Morningstar, company reports 8 General Mills GIS Stock Px (LH) Div. Rate (RH) 60 1.90 48 1.52 36 1.14 24 0.76 12 0.38 1995 2000 2005 2010 2015 10-Year Earnings and Dividend Summary CoreEPS DivPaid Payout CoreEPS DivPaid Payout FY04 1.43 0.55 39% FY11 2.48 1.12 45% FY05 1.37 0.62 45% FY12 2.56 1.22 48% FY06 1.45 0.67 46% FY13 2.69 1.32 49% FY07 1.59 0.72 45% FY14 2.82 1.55 55% FY08 1.76 0.79 45% CAGR: 7.1% 10.9% FY09 1.99 0.86 43% FY10 2.30 0.96 42% FY15e 2.82 1.67 59% The Dividend Drill: What’s the Return? g Total return is always the bottom line, not income alone or growth/capital gains alone Realty Income O 60 3.70 g Is the absolute return indicated by a safe current yield plus sustainable long-run dividend growth acceptable? 48 2.96 36 2.22 24 1.48 12 0.74 /Hurdle returns of 7.5% for low risk companies with above-average yields; g Am I paying a sustainable valuation: will total return = dividend yield + dividend growth? /Consider valuation: Our main indicator is price/fair value (preferred below 1.0) g Preferred outcome is total return > yield+growth, valuation discipline necessary to avoid shortfalls 1995 2000 Stock Px (LH) 2005 Johnson & Johnson JNJ 2010 Stock Px (LH) Div. Rate (RH) 2015 Div. Rate (RH) 140 2.80 112 2.24 84 1.68 56 1.12 28 0.56 0.00 1995 Data as of 3/19/2015. Source: Morningstar 9 2000 2005 2010 2015 Dividend Drill in Action: Verizon Communications g The Dividend: Is It Safe? /Free cash flow is the best indicator; covers dividends about 1.5 times /Economically defensive business; narrow moat and BBB credit rating g The Dividend: Will It Grow? Verizon VZ Stock Px (LH) Div. Rate (RH) 70 3.10 56 2.48 42 1.86 28 1.24 14 0.62 1995 2000 2005 2010 2015 /Dividend increases each year since 2005 /Modest but accelerating growth recently g The Dividend: What’s the Return? /Trading slightly below $50 fair value /4.5% yield plus 4%-5% estimated dividend growth suggests roughly 9% total returns Data as of 3/19/2015. Source: Morningstar, company reports 10 10-Year Earnings and Dividend Summary CoreEPS DivPaid Payout CoreEPS DivPaid Payout FY04 2.59 1.54 59% FY11 2.15 1.96 91% FY05 2.56 1.60 63% FY12 2.32 2.02 87% FY06 2.54 1.62 64% FY13 2.84 2.08 73% FY07 2.34 1.65 70% FY14 3.35 2.14 64% FY08 2.54 1.75 69% CAGR: 2.6% 3.3% FY09 2.40 1.86 77% FY10 2.21 1.91 87% FY15e 3.66 2.22 61% Step 3: Portfolio Management g What drives an individual stock’s returns works even better for a portfolio as a whole /Our Dividend Select portfolio targets 3%-5% yields, 5%-7% dividend growth, 9%-11% total returns /Currently yielding 3.9% with 6.1% long-run income growth profile g Earning yields that are double the market average requires embrace of different results: We go where the (safe and growing) dividends are ... S&P 500 Dividend Select 30 25 20 15 10 5 0 Data as of 3/18/2015. Source: Morningstar 11 Our Results: Beating the Market Without Even Trying Cumulative Total Return: DividendInvestor Portfolios vs. S&P 500 200 150 100 Standard & Poor's 500 (CAGR: 7.9%) Combined DividendInvestor Portfolios (CAGR: 9.2%) 50 0 -50 2005 2006 2007 2008 2009 2010 2011 Cumulative Price Appreciation 80 60 40 S&P 500 DividendInvestor 19.4 percentage point disadvantage (-1.2%/year) 2012 2013 2014 2015 Cumulative Dividend Return 80 60 40 S&P 500 DividendInvestor 20 20 0 0 -20 -20 -40 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 -40 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 Data from inception (1/7/2005) through 3/19/2015. Source: Morningstar 12 32.8 percentage point advantage (2.4%/yr) Josh Peters, CFA, owns all of the stocks held in the Dividend Select portfolio, including GIS, JNJ, O, VZ.

© Copyright 2026