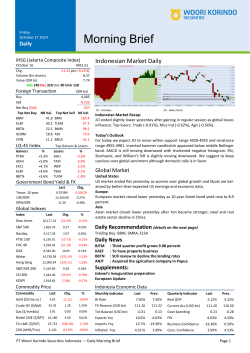

full report - Profindo International Securities

COMPANY NOTES PT Telekomunikasi Indonesia TBK (TLKM:IJ) Bayu Cahyadi [email protected] MARKET CAP IDR 285.77 TRILLION SHARES OS 100.8 BILLION SHARES CURRENT PRICE IDR 2835/SHARE TARGET PRICE IDR 3338/SHARE UP/DOWNSIDE +17.74% RATING BUY SUSTAINING THE SUPPLY LEADER POSITION FY14 Revenue increased 8.1% yoy to IDR 89.7 tn while Bottom Line up slightly by 3% yoy to IDR 14.6 tn. The result was quite amazing, mention that XL and Indosat inked negative result. Look forward, the company stays optimistic in 2015 in beating the industry, which now becomes more addictive to the Data & Internet. In a slow growth industry, it is rare to have growing company like Telkom. Recent market correction gives investors a buying opportunity with a Target Price of 3338/share, 21.8x PE FY15F. FY14 Result: Higher than Industry Telekomunikasi Indonesia Tbk, the biggest telecommunication company in Indonesia, has been successfully expanding its business on the back of intense competition in the industry. Consolidated FY14 revenue grew by 8.1% yoy to IDR 89.7 tn while Telkomsel Revenue grew by 10.4% yoy to IDR 66.3 tn. Moreover, EBITDA margin stayed strong at 51.1% (consolidated). While revenue was growing better than the industry, the company has been attracting more users. Full Year 2014, Broadband users grew 12.1% yoy to 71.3 million, cellular subscriber grew 6.9% to 140.6 million and mobile data user grew by 12.1% yoy to 67.9 million. The company stated the optimism that the subscribers number will grow even more in the future due to high quality service provided. At the end of the day, market will look wisely on the bottom line. Telkom’s net profit was up 3% yoy to IDR 14.6 tn while EBITDA increased by 9.7% yoy to IDR 45.8 tn. Jump to the conclusion, we believe that the result is quite satisfying investors as the other players in the market such as Indosat and XL stated negative bottom line. Source: Company April 2, 2015 www.profindo.com Focusing on Data & Internet in 2015 Since we are now facing 2015, enough for 2014 result discussion. In 2015, the company believes that revenue from data, internet and IT growth will boost the overall revenue. The optimism comes from rapid increase smart phone users in Indonesia. While cellular revenue is predicted to be stagnant, overall revenue is projected to be higher than the industry. Last time, Telkom forecasted IDR 100 Trillion PT Telekomunikasi Indonesia Tbk FY15 revenue, +11.5% yoy. During our visit to the company, the corporate secretary did not confirm the forecast number. But, he said that Telkom is very optimistic to grow above the market growth. We estimate that the bottom line FY15F should be around IDR 15.45 tn, +5.56% due to lower profit margin by ~1% due to higher transportation, depreciation and space rental costs. Those higher costs are for expanding company’s infrastructure in order to maintain company’s status as “Supply Leader” in the industry. Jump to valuation, we estimate that the equity fair value should be at IDR 336.5 tn or 3338/share, valued at PER 21.8x FY15F. Page |2 PT Telekomunikasi Indonesia Tbk KANTOR PUSAT KANTOR CABANG BANDUNG http://www.profindo.com Gedung Permata Kuningan, Lt. 19 Jl. Kuningan Mulia, Kav. 9C, Guntur Setiabudi Jakarta Selatan 12980 Phone : +62 21 8378 0888 Fax : +62 21 8378 0889 Jl. Sunda No. 50B Bandung, Jawa Barat Phone : +62 22 420 2678 Fax : +62 22 420 2676 EMAIL : [email protected] [email protected] DISCLAIMER This research report is prepared by PT PROFINDO INTERNATIONAL SECURITIES for information purposes only and is not to be used or considered as an offer or the solicitation of an offer to sell or to buy or subscribe for securities or other financial instruments. The report has been prepared without regard to individual financial circumstance, need or objective of person to receive it. The securities discussed in this report may not be suitable for all investors. The appropriateness of any particular investment or strategy whether opined on or referred to in this report or otherwise will depend on an investor’s individual circumstance and objective and should be independently evaluated and confirmed by such investor, and, if appropriate, with his professional advisers independently before adoption or implementation (either as is or varied). Page |3

© Copyright 2026