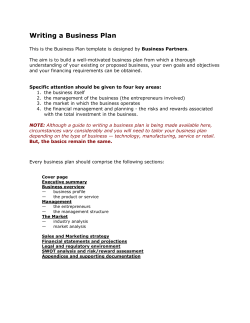

The Art of the Start