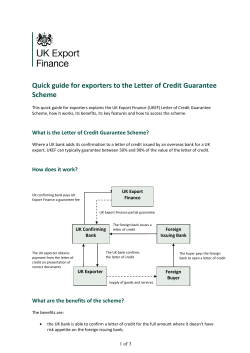

How to cope with the downturn Clothing & textiles industry overview