Agent’s Voice the

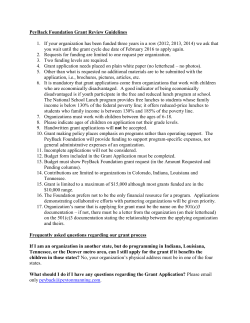

the Agent’s Voice October 2011 Vol. XXXVIII, No. 8 7 Ways To Kill Your Future Without Even Knowing It pg 13-14 How To Stay Top-of-Mind with Insurance Clients and Prospects pg 15-16 LWCC: BECAUSE A HARD HAT JUST ISN’T ENOUGH. Joe Cain (second from right), President and owner of Coral Marine Services, meets on-site with his LWCC account team: (from left) Hardy Zeigler, Senior Loss Prevention Consultant; David Posner, Underwriting Account Executive; and Becky Causey, Senior Claims Representative. At right is diver David Martin. Coral Marine Services specializes in the employing some of the most knowledgeable and challenging and inherently dangerous work of experienced salvage crews and divers in the industry. marine salvage, tank cleaning, oil-spill cleanup, “Our LWCC loss prevention consultant comes out and related industrial services. They have been and spends time with us,” says owner Joe Cain. “He’ll a policyholder with us, the Louisiana Workers’ look at our operations and discuss any hazards he Compensation Corporation, since 1993 while might see. He adds real value to our safety program, working with Paul’s Agency, their insurance broker. and we collaborate on the appropriate changes.” Together, our three companies share a dedication to workplace safety. Based in Amelia, Louisiana—near Morgan General Manager Ronnie Kinchen says, “LWCC’s claims service is also outstanding. Their staff does what’s necessary to help injured workers, City—Coral Marine Services has earned a and they assist us in getting our valued employees well-deserved reputation over the years by back on the job.” www.lwcc.com Inside This Issue The Agent’s Voice Published by the Professional Insurance Agents of Louisiana, Inc. DEPARTMENTS President’s Message………………………………...........4 Commissioner’s Column.........................................6-7 No material may be reproduced in whole or in part without written consent of PIA of Louisiana, Inc. Statements of fact and opinion in The Agent’s Voice are the responsibility of the authors alone and do not imply an opinion on the part of the officers or the members of the Professional Insurance Agents. Participation in PIA events, activities and/or publications is available on a non-discriminatory basis and does not reflect PIA endorsement of the products and/ or services. The Agent’s Voice is published ten times a year by the Professional Insurance Agents of Louisiana, Inc. Free subscription is included in PIA membership. Non-member subscription is $2.50 per copy, $25 per year. Contact the Editor for more details. Passing It On..........…………….………….........…..........8 PIA Errors & Omissions...........................................9-10 FEATURES 7 Ways to Kill Your Future Without Even Knowing It........................................13-14 How to Stay Top-of-Mind with Insurance Clients and Prospects ...........................15-16 Louisiana Legal Updates..........................................25 IN EVERY ISSUE All communications for publications, including news, features, advertising copy, cuts, etc. must reach publisher by 1st of month prior to month of publication. Advertising rates furnished upon request. Member News.........................................................11 Address inquiries to: EDITOR, THE AGENT’S VOICE 8064 Summa Avenue, Suite C Baton Rouge, LA 70809 Index of Advertisers ………….………….…....................26 Partner News............................................................12 2011 CISR Schedule ....................……………............18 Editorial Cartoon ......................................................26 Member Benefit in Focus .……...………….……...........26 Phone: (225) 766-7770 Watts: (800) 349-3434 Fax: (225) 766-1601 Email: [email protected] Website: www.piaoflouisiana.com Mission Statement Promoting the professional insurance agency system, leading through support, representation and fellowship. OFFICERS President’s Message Gene Galligan, Monroe President Manuel DePascual, Metairie President-Elect Darryl Frank, Metairie Secretary/Treasurer Duane Dimattia, Baton Rouge Immediate Past President Richie Clements, Chalmette PIA National Director DIRECTORS Karen Bryant, Denham Springs Lisa Donlon, Lafayette Dawn Duhé, Hammond John Erny, Lafayette Patrick LeBoeuf, Westwego Joe Lohman, Baton Rouge Jim Moore, Destrehan Al Pappalardo, Jr., Mandeville Barry White, West Monroe Kevin Woods, Monroe PIA OF LOUISIANA STAFF Jody M. Boudreaux Executive Vice President & Editor Natalie S. Cooper Director of Industry Affairs Laurie Whipp Director of Marketing Coleen Brooks Director of Member Services D uring the week of September 22-24 your Executive Committee was in San Francisco attending the National Fall Governance Meetings & PIAPAC Event. Yes, we worked. Duane, Manuel, Darryl, Richie, Jody and I attended meetings Thursday through Saturday. November 18. PIA is supporting a 5 year extension. We have been against adding wind coverage to the program. However, Sen. Roger Wicker, R-MS, has added an Amendment to the Senate Bill reviving the Wind-vs-Water debate. The Wicker amendment utilizes data currently colIt is always interesting to attend Nationlected by the National Oceanic and Atal PIA Events. We learn what the other mospheric Administration, academic State Associations’ probinstitutions, and private lems are and what they entities to allocate windPresident, PIA of Louisiana are doing to solve them. vs-water damages followOne problem that is Naing a hurricane. The bill Gene Galligan Insurance Agency tional in scope is “How to creates a “standardized reach Gen Y?”. You hear [email protected] loss-allocation” system to the term, but what does distribute losses between it mean. Gen Y is anyone born in the the NFIP and private or residual-market 1980’s to early 1990’s. The PIA Nationwind insurers. If the bill passes with the al website has an informative program 5 year extension and with Sen. Wicker’s on Gen Y members. PIA National ran amendment, the PIA will revisit our poa survey that showed that 83% of Gen sition and support the bill. It was felt Y use the internet to price shop. Howthat the bill holds out the possibility of ever, 97% would prefer to buy from a lodeveloping a fair, equitable system that cal store, 96% felt that it was important serves everyone’s interest. to speak to a knowledgeable person, and 60% wanted phone contacts after In the Government Affairs Committee, a sale compared to 33% wanting an ethe importance of the State Affiliates mail. Consensus was that we need a Grass Roots efforts was stressed not presence on the internet, but we must only on the State level, but also, on return to providing personal service. the National level. The Congressional Management Foundation ran a survey As I sat listening to the conversation, I of Congress and found that 97% of the noted that there was no one of Gen Y legislators respond to constituent visits, age in the meeting. 88% to customized e-mails and 51% to Another continuing problem is the National Flood Insurance Program, set to expire on September 30, and since extended to October 4, and lastly to Page 4 • October 2011 Continued on page 22 October 2011 • Page 5 Commissioner’s Column By James J. Donelon NIMA Has Strong Kick-Off I Effective July 21, 2011, n July’s Commissioner’s Column on the 2011 Regular Legislative the home state has exclusive tax and regulaSession I discussed the Nonadmittory jurisdiction over ted Insurance Multi-State Agreesurplus lines insurance ment (NIMA) legislation that passed in Louisiana. At that time five states policies—even for policies covering properties, risks, or had joined NIMA. located Currently, 12 juris- Commissioner of Insurance exposures in multiple states. dictions have joined Louisiana Department of NIMA, representing Insurance The test for the home 22 percent of the [email protected] state of the insured surplus lines marhas several layers. The ketplace based on first is the principal place of business 2009 data. I would like to discuss further this landmark agreement or principal residence, for an individual, when there is a portion of the inand its significance for our state. sured properties, risks, or exposures The Nonadmitted and Reinsurance in that state. If the policy does not cover properties, risks, or exposures Reform Act of 2010 (“NRRA”) is the in the principal place of business or subtitle of the Dodd-Frank Wall Street Reform and Consumer Protection Act residence, then the state to which the (“Dodd-Frank”) that makes changes greatest percentage of taxable premium is allocated is the home state. In in the state-based system of regulating insurance. The first part of the all cases of policies covering properties, risks, or exposures in only one NRRA mandates a single-state system of surplus lines regulation based state, that state will be the home state. on the statutory home state of the surplus lines insurance policyholder. Contact the Louisiana Department of Insurance at www.ldi.state.la.us or call 1-800-259-5300 Page 6 • October 2011 The exclusive premium tax jurisdiction of the home state is a truly novel provision of the NRRA. Congress assigned tax jurisdiction to one state but expressly intends the sharing of taxes through the adoption of uniform nationwide procedures, such as a compact, that provide for the reporting, payment, and allocation of surplus lines premium taxes. There is an incentive for some states with large surplus lines premiums to join such a compact and avoid the loss of premium taxes, but those states that are home to large multistate companies may have a fiscal incentive to go it alone on premium taxes. In response to the NRRA and the intent of Congress, Louisiana participated in drafting through the National Association of Insurance Commissioners (NAIC) and, on July 1, 2011, joined the NIMA. Bulletin 2011-01 addresses Louisiana’s participation in NIMA and the implementation of the NRRA’s requirements in Louisiana. This bulletin may be found on the Department of Insurance Web site at www. ldi.la.gov under the Companies tab. The placement of surplus lines insurance is now subject solely to the statutory and regulatory authority of the insured’s home state. The NRRA provides relief from multiple states’ regulation of a policy covering multistate properties, risks, or exposures. A broker will only have to meet the diligent search requirements, if any, and the surplus lines licensing requirements of the insured’s home state. The NRRA further provides for the preemption of any state law, regulation, provision, or action that conflicts with the exclusive home state authority over taxing and regulating surplus lines insurance and licensing of surplus lines brokers. Federal preemption does not extend to the placement of surplus lines insurance for workers’ compensation or excess insurance for self-funded workers’ compensation plans. The NRRA preempts state eligibility rules for surplus lines insurers and applies different criteria for U. S.-domiciled and alien insurers. Insurers domiciled in a U.S. jurisdiction need only possess a license to write a certain line of business in its domiciliary state and have capital and surplus of at least $15 million. States could compact to establish uniform nationwide standards that are different, but a nationwide uniform compact will be difficult given that several states have laws or policies prohibiting the delegation of legislative powers. Alien surplus lines insurers need only be on the NAIC Quarterly Listing of Alien Insurers. In compliance with the NRRA, Louisiana now has a much shorter application for white listing surplus lines insurers that focuses on their meeting the NRRA criteria. The agreement allows state authorities to work cooperatively to collect and allocate premium taxes for multi-state surplus lines insurance transactions based on the risk or exposure in each state as has been done in the past. These premium taxes provide support to the states’ general funds. Without this agreement, several states could potentially lose surplus lines tax revenues to the “home state” as defined in the NRRA (Louisiana has about $25 million per year at risk). We are expecting more states to join NIMA now that the July 21 effective date of NRRA has passed. Contrary to what some have said, there is a surplus lines tax allocation system legally in force—NIMA. While it is true that the clearinghouse is not yet operational, NIMA is accepting memberstates and organizing them to build an effective system for tax allocation. On the other hand, the Surplus Lines Insurance Multi-State Compliance Compact (SLIMPACT) has yet to come into force under its own terms with only nine of the needed ten member states. The participating states and territories now include Alaska, Connecticut, Florida, Hawaii, Louisiana, Mississippi, Nebraska, Nevada, Puerto Rico, South Dakota, Utah and Wyoming. NIMA members plan to elect officers and select a clearinghouse to administer the funds. The State of Florida has agreed to temporarily house the NIMA website (http://www. floir.com/Sections/PandC/NIMA.aspx), which will contain the signature documents from member states. I encourage you to follow the progress of NIMA here. October 2011 • Page 7 Passing It On! By Jody M. Boudreaux L a sales pitch when ast month at our PIA National calling for a quote meetings, we were introduced to or service. a new deliverable offered by the PIA Partnership. In the past, this is the The objective is for you and your staff group that put together the programs to take this quiz together and then assisting with perpetuation planning, see how your answers match with the reaching Gen Y and successful planning. results of the survey Now, they have completed performed by The a national consumer survey Executive Vice President, Partnership. As you and I’d like to provide you PIA of Louisiana can imagine, there with a general preview of the results in this article. [email protected] are a few surprises for you. I don’t want to spoil the fun for Questions that were asked you, so I encourage you to go to www. to general consumers of insurance agencytouchpoints.com to check it out. included the following: It’s a great exercise and this web site not only provides you with the survey 1. True or False? Prospects care mostly results, but it then provides you with about price…not what we can do for tools you can use to respond to these them as an agency. results in your business plan. 2. True or False? Customers don’t want or have time for coverage reviews. 3. True or False? The biggest advantage for people doing business with our agency is that we represent more than one company. 4. True or False? Customers believe that most personal lines home and auto coverage is the same. 5. True or False? Customers prefer to be left alone and pestering customers make them go away. 6. True or False? Customers don’t want Page 8 • October 2011 Let me say a little more about this process. If your answers don’t agree with your customers, your competitors are probably gaining the advantage. Carefully review this Website to help you: • Consider changes you could make • Make decisions about how to make changes • Use tools specifically designed for agencies • Monitor and measure results Without spoiling the results, I’ll give you a little teaser to maybe get you interested in seeing the full results. The results show that customers do not view insurance (PL auto in the case of this research) as a purely price-driven Continued on page 22 Mark your calandar for PIA of Louisiana’s 69th Annual Convention July 28-31, 2012 Moody Gardens Galveston, Texas PIA Errors & Omissions By Curtis M. Pearsall, CPCU, AIAF, CPIA Excess & Surplus Lines: uniqueness that could spell Errors & Omissions trouble W that the risk be bound. ith many industry journals and In some cases, they may experts indicating a firming of not even have the authorthe marketplace, activity to the Excess ity to bind the risk and & Surplus Lines marketplace could inmay need to contact the carrier. crease. While this segment of our industry plays a vital role, it is important Bottom line: as the retailer, do not adto understand the uniqueness it presvise the client that covents. Failure to do so erage is bound until you could spell Errors & Special Consultant have confirmation from Omissions trouble. Utica Nat’l E&O Program the wholesaler. There are a number of Utica Mutual Insurance Co. Binding requirements issues to lookout for, If you deal with mulso let’s review some tiple wholesalers, chances are the of the main ones. procedures and expectations to bind among those wholesalers differ. Let’s Lack of authority to bind say you want to bind a risk at 4 p.m. In the standard marketplace, carriers on a Friday. Can you do it or will the typically spell out the types and sizes wholesaler advise you that they need of risks agencies can bind. This adds premium payment and the necessary to the efficiency of the process. Conaffidavit forms before they can bind? versely, in the Excess & Surplus marClearly know the rules of engageketplace, accessing these carriers ment when working with wholesalers. typically requires you to deal with an Professional wholesalers will make it agency that has an E&S license, tradiclear on the proposals what is needed tionally referred to as a wholesaler. to bind coverage. Be aware of these “rules” and factor them into your hanThe wholesaler’s job – which most do dling of the risk. Look for wholesalers very well – is to provide your agency who will provide you with an account with access to additional carriers that current for your business. This will write more specialized risks and potake away some of the potential headtentially some hard-to-place risks. The aches. wholesaler is technically the agent for that carrier and will have some type of Classification Limitation endorsebrokerage contract. Your retail agency ment/other unique endorsements is not an agent for these carriers and Do you know if the E&S carriers in your thus you do not have binding authorstate include the Classification Limitaity. To bind a risk, you would need to tion endorsement on their policies? advise the wholesaler of your desire You need to know because this form has the potential to be your biggest headache. What this endorsement essentially does is restrict coverage under that policy to only those classifications noted on the policy. For example, if you insure a painter who only performs inside painting, the coverage would state only claims arising from inside painting would be covered. If the painter gets the opportunity to paint the outside of a house, there would be no coverage unless the policy was modified accordingly. Look out for this form and, if it is included on that particular policy, advise your customer in writing of this limitation. Explain that if they perform any work outside the stated classifications, they have no coverage and should contact the agency before undertaking this additional work. There is also the possibility the proposal/policy may contain other unique endorsements that could severely limit the coverage actually provided. Watch for these forms. It is highly recommended advising your client of these various limiting endorsements or exclusions at proposal time and when you send them the policy. Note in your cover letter to them that they should read their policy carefully and contact the agency with any questions. October 2011 • Page 9 Don’t expect the renewal policy to look like the expiring one – it probably doesn’t When your E&S accounts come up for renewal, there is a good chance you will need a renewal application as automatic renewals are not the norm on the E&S side. When you receive the renewal proposal from the wholesaler, review it carefully, identifying any changes or new endorsements being added. When a carrier wants to modify coverage in the E&S industry they do not need to issue a conditional renewal notice, unlike the standard marketplace. The E&S carrier may add new exclusions or even reduce the limits. No Guaranty Fund With the exception of New Jersey, the State Guaranty Fund does not provide any protection if an E&S carrier is declared insolvent. As a result – and even for agents in New Jersey – it is highly recommended to know the financial condition, the A.M. Best rating, of the carrier. When you receive proposals, know who the carrier is. It may be a new carrier you have never heard of or a carrier you have dealt with. Carrier ratings change, so know the carrier’s current rating. It is not a bad idea to ask the wholesaler, don’t rely strictly on their feedback. It is very easy to check carriers’ ratings through the A.M. Best website (www.ambest.com). Compliance with state regulations on accessing the E&S market There are a number of states requiring that a risk be declined by a specific number of admitted markets before business can be placed in the E&S marketplace. Continued on page 19 ONE STANDS ALONE AT THE TOP While it’s hoped they will give you advance notice, they are typically are not required to. It is wise to ask your wholesaler ahead of time if they expect any changes on the renewal policy. There is a chance the coverage changes could be significant. In some cases, the customer may not be agreeable to the changes, so make it part of your process to contact the client and review the renewal proposal with them to get their approval on whether they want coverage bound. No backdating It is critical that the agency’s staff clearly understands there is no backdating of coverage in the E&S market. As account executives prioritize their work, special attention should be given to accounts in the E&S market. If there is an account that renews on a Saturday and you leave the office on Friday not having bound the account, there is a very good chance that when you call on Monday to bind, the account will be bound as of Monday – once again, no backdating. If there was a loss over the weekend, there will probably be no coverage in effect. This could be a significant issue with property coverage. Page 10 • October 2011 ACTIVE LOSS CONTROL PROMPT CUSTOMER SERVICE LOCAL CLAIMS HANDLING COMPETITIVE IN ALL CLASSES Phone: 318-628-6730 Fax: 318-628-6737 SUBMIT APPLICATIONS TO: [email protected] Information to share with your insureds… Auto Insurance: The Basics Automobile insurance consumers frequently ask “How much coverage do I need?” There is no one correct answer to this question because it depends on one’s personal situation. One important factor is: You need to be covered. Not only is having auto insurance important for the safety of you, your family and those around you, it is also the law. bills or property damage incurred by the injured party. With the volume of lawsuits filed in Louisiana, chances are you could find yourself named as a party in a suit. If you are underinsured, this could be a costly situation for you and your family. So, in order to protect yourself and your family’s assets, more coverage would be a wise decision. Louisiana law LRS 32:900 requires all motorists to carry liability coverage of at least $15,000 covering bodily injury to one person, $30,000 for more than one person injured in a single accident and $25,000 to cover damage to another person’s vehicle or property. Consider whether you want to purchase comprehensive and collision coverage. Collision coverage does just what the name implies. It covers damage to your vehicle if you hit another car or that pesky mailbox next to your driveway. In the same fashion, comprehensive covers other things that might happen to your vehicle like fire, theft, or vandalism. Even though auto liability is mandatory, not everyone has it. Individuals who drive uninsured should be aware of Louisiana’s “No Pay, No Play” law (LRS 32:866) which prohibits uninsured motorists from collecting the first $15,000 in personal injuries and the first $25,000 in property damages, regardless of who caused the accident. While only the minimum liability limits are required, there are other factors to consider when deciding how much coverage you need to purchase. Do you own a home? Are you a small business owner? What type of assets do you own? These are all important things to consider when determining how much coverage you need. If you are involved in an at-fault accident which injures another party, the minimum liability limits may not cover the medical The thought of purchasing insurance may give you budgeting nightmares, but when you consider the number of vehicles on the road at any given time, you can be sure that having auto insurance and the appropriate coverage will benefit you in the long run. So know your needs, know your coverage, and you will be ready when something unexpected happens. If you are still unsure of how much coverage you need or would like to learn more about the additional types of auto coverage, speak with a licensed insurance producer or contact the Louisiana Department of Insurance Office of Consumer Advocacy for more information. Source: LDI Monthly Consumer Advocacy Newsletter Member News Weatherspoon Named President of International Organization’s Baton Rouge Chapter Tawanda A. Weatherspoon, contract surety account manager at Wright & Percy Insurance, a division of BancorpSouth Insurance Services, Inc., was recently chosen president of Insurance Professionals of Baton Rouge. Weatherspoon previously served as the organization’s treasurer and state council sponsorship chairman. Also named were: • Carol Brown of LUBA Workers’ Comp, President Elect • Laura Molino of Wright & Percy Insurance, Treasurer • Jane Walker of LUBA Workers’ Comp, Secretary • Deborah Ledford of Wright & Percy Insurance, Parliamentarian and Board Member • Sylvia Thronson of Wright & Percy Insurance, Board Member Insurance Professionals of Baton Rouge is the local chapter of the National Association of Insurance Women, which operates as the International Association of Insurance Professionals. The organization has affiliated associations in more than 300 locations. October 2011 • Page 11 Partner News LWCC-Kids’ Chance Invitational Golf Tournament Raises $38,000 At the annual LWCC-Kids’ Chance Invitational Golf Tournament, held in September, Louisiana Workers’ Compensation Corporation (LWCC) raised $38,000 to go toward scholarships for dependent children of workers who have been killed or permanently and totally disabled in a work-related accident. LWCC presented a $38,000 check to the Louisiana Bar Foundation’s Kids’ Chance scholarship program during a September 26 awards ceremony immediately following the tournament, held at the Country Club of Louisiana in Baton Rouge. Kids’ Chance Committee Co-Chairman Gary Knoepfler accepted the check on behalf of the charity. During the eight years it has been held, the tournament has raised more than $267,000 for the Kids’ Chance program. The program is administered by the Louisiana Bar Foundation and is governed by a committee representing a cross section of the legal and workers’ compensation communities, including LWCC. The first Kids’ Chance program was founded in 1988 by the Workers’ Compensation Section of the Georgia Bar Association. Today there are programs in 28 states. “LWCC is honored to help provide financial assistance for these deserving young students,” said LWCC President and Chief Executive Officer Kristin Wall. “The Kids’ Chance scholarships pay for school tuition, books, fees, and general living expenses.” Kids’ Chance scholarships are available to Louisiana residents from ages 16 to 25 who demonstrate financial need and meet other qualifications. Any accredited Louisiana university; community, technical or vocational college; or state-approved proprietary school qualifies. LWCC Conference Focuses on Medical Treatment Guidelines Louisiana Workers’ Compensation Corporation (LWCC) spotlighted the state’s recently issued medical treatment guidelines for the care of injured workers during a conference attended by many of the company’s medical providers. Held October 14 and 15 at The Roosevelt New Orleans, the LWCC Provider Partnership Conference was jointly sponsored by the American Academy of Disability Evaluating Physicians. Among the guest speakers was Wes Hattaway, director of the Louisiana Office of Workers’ Compensation Administration (OWCA). The OWCA issued the medical treatment guidelines, and they went into effect on July 15 this year. In 2009, the Louisiana Legislature had passed RS 23:1203:1, requiring OWCA to develop the guidelines. Page 12 • October 2011 In his conference remarks, Hattaway reviewed the process of implementation, the roles of the OWCA Medical Advisory Council and medical director, and the criteria for developing the guidelines. He noted that they will be reviewed each year to incorporate the latest research for effective and efficient treatment of injured workers. As part of its goal to improve patient outcomes, LWCC has hosted six provider partnership conferences since 2002. Among other speakers at this year’s event was David Deitz, MD, PhD, Vice-President and National Medical Director for Liberty Mutual Insurance Group, who gave an overview of treatment guidelines and how they improve functional outcomes. Continued on page 19 Seven Ways To Kill Your Future Without Even Knowing It By John Graham N o one needs to be told that doing business today is dramatically different from even a few years ago. In spite of what may seem so obvious, many continue to cling to a familiar past with nothing less than stubborn tenacity. While it’s easy to spot others who have fallen behind, it takes almost desperate determination to drown out the noxious notion that we may be out of sync. We’re out of luck, however; there’s no more wiggle-room. There’s no pleading for a second chance. Now, it’s only playing for keeps. While we laud team effort, it becomes clear that individual players are expendable. Even if we’re good at what we do, we may be undermining ourselves without even knowing it. And, more often than not, it’s not the big stuff that sinks us. It’s the little telltale things that silently add up until there comes a tipping point. And then it’s all over. Most of the time we can’t figure out what happened. It wasn’t someone else who had it in for us; we did ourselves in. Before saying, “No one needs such a dark dose of pessimism,” consider several thoughts that may help quantify the idea that our wounds are selfinflicted. Here are just a few: 1. Little words. Big story. One business owner makes it a practice to ask job applicants to include a cover letter with submitting a resume. “I want to see how many times they use such words as ‘I,’ ‘me’ or ‘my,’” he says. “If these pronouns jump off the page, this may be a person who lacks self-awareness and quite possibly lacking in selfconfidence.” If’ you’re scratching your head and wondering if such an idea is totally off the wall (and even unfair), don’t be too sure. What the business owner came upon almost intuitively, James W. Pennebaker of the University of Texas at Austin, arrived at through research, as presented in his book, The Secret Life of Pronouns. John Graham, a marketing and sales consultant and a business writer, lives in Boston. He can be contacted at 617-774-9759 or [email protected]. It may be more productive to tune out the big content words (jargon, in particular) and pay closer attention to the “little words.” They may be telling us a “big” story. Just think of the times you’ve read letters littered with I, me and my. What do they say about the writer? 2.Inferred incompetence. If a test is needed, here’s a quick one to identify incompetence. Ask someone to prepare a report, develop a meeting agenda, arrange a meeting or write a letter and you’re pleased they embrace the task with interest and enthusiasm (which is what you want to hear, of course). “I’ll have it for you tomorrow,” they tell you. And that’s the end. Whatever the agreed upon schedule, nothing happens. Even two, three or more nudges fail to get a response. Tomorrow never comes. Eventually, it’s clear that nothing is going to happen. This is a classic case of “inferred incompetence,” a case of performance failure. It’s the perfect way to skewer your own future. 3. Optimism’s false positive. Entrepreneurs and salespeople shun negative thoughts faster than they do a skunk on the loose. As far as they’re concerned, it’s always a “done deal,” even though the order isn’t signed or buyer hasn’t said yes. Optimism keeps them going. They live on the upside. Unfortunately, that’s only part of the story. In describing a new product, the company official said, “Everyone will want it. This will be the biggest thing that ever happened to us.” Unfortunately, it’s no more than a poof of dust. It was all down hill from there. In a study reported in The Journal of Experimental Social Psychology(July 2011), researchers Heather Barry Kappes and Gabrielle Oettingen point out that fantasizing about something very positive, such as “hitting the numbers,” closing a huge account or reaching a particular goal can make us feel that we have actually done it. When October 2011 • Page 13 that happens, we tend to relax, let up and back off. The study suggests that too big a dose of optimism causes us to blank out the hurdles, everything that must be faced if we’re to reach the goal. 4. Blinded by success. Sydney Finkelstein, a management professor at Dartmouth’s Tuck School of Business, was asked what CEOs who made monumental mistakes have in common. “That unfortunate combination of believing they’ve got it all figured out while turning a blind eye to early warning signs.” One of Finkelstein’s examples is Andrew Mason, the CEO of Groupon, who turned down Google’s $6 billion offer for the company. Not only did he seem to discount the hundreds of mice nibbling away at his cheese, but it would seem he lost sight of the sick economy, and failed to recognize what consumers wanted next to light their buying imagination. By mid-2011, Groupon had lost up 50% of its sales and much of its value. $ 5. Dues paid in full. They say nothing in baseball history comes close to the September 2011 collapse of the Boston Red Sox. Amid the “howdid-it-happen” post-mortem speculation, Boston Globe sports writer Nick Cafardo may have come closest to the explanation. “This was a team that had no fire. It was a team that had no urgency….It’s a team that needs to be hungry again.” He then wonders how that happens with a team with monster paychecks Page 14 • October 2011 and incredible success. Whatever else it is, it’s the story of what happens to anyone who decides they’ve paid their dues and don’t need to put in a full day or step up to the plate. That’s just for the rookies. 6. Destructive delusions. If we believe our decisions are well thought out and unquestionably rational, we’re kidding ourselves. One morning a client, who is also the president of his company called and quickly began complaining about the new iPhone he had been issued. As a confirmed Apple devotee, I instantly found myself arguing with him. “How could anyone believe that?” I said to myself. After a few minutes of bantering, he said, “You’re an Apple person. There’s no discussing this with you.” He was right on both accounts. It happens all the time. In his book, The Believing Brain, Michael Shermer, Ph.D., suggests that the brain develops patterns that shape the way we perceive reality. But then something interesting occurs. We latch on to any information that confirms those beliefs and push aside whatever attempts to challenge them. And there’s the rub. Unless we constantly challenge our thinking, what we assume to be rational thought becomes little more than prejudice. Really, is it possible to believe the Android OS is totally without merit or even a much-disliked politician is without merit? 7. The ROI card. Businesses can either play or ignore the “ROI card,” depending on the situation. Almost always, they do it inappropriately. Does anyone believe that HP took the ROI into account when it splurged a billion plus bucks on Palm. It wanted a tablet product so much, it wrote the check and then scrapped the project less than a year later. That’s an instance when the ROI card should have been played. But that isn’t what the then CEO wanted to hear. It’s easy to “overthink” one’s importance in a culture where contrary views aren’t tolerated. There are other business situations when the “ROI card” deserves being ignored. A good example is a 43-store dry cleaning chain in the Northeast started an annual drive for winter coats more than 15 years ago. The company cleans 60,000 coats each fall at its own expense and supplies them to community agencies for distribution to babies, kids and adults. It also gives more than 250 schools and youth groups the chance to earn special rewards for collecting coats. More than 150 businesses and organizations also collect coats. Beyond all that, the company partners with a TV station, a nationally-known furniture company and several radio stations and 100 plus newspapers that help promote the program. Is such a program good business? Probably not, the cost is taken into account. Even so, some bold leader says, “It’s the right thing to do.” There are occasions companies are best served by failing to play the ROI card. Anyone of these seven examples can put the future of an individual or an organization in jeopardy, whether it’s looking beyond an idea’s ROI or moving forward blinded by our success. How to Stay Top-of-Mind with Insurance Clients and Prospects By Ted Janusz A dvertisers tell us that consumers regular, with the emphasis on regular, need to see a message five to seven e-mail newsletters. It’s far cheaper times before they will take action. But than sending anything in print. how can we insurance agents get our message out to clients and prospects in a timely and cost-effective way . . . Chris Chapin is the founder of Easy Insurance Newsletters.” View a quick video of that they will actually notice? his service at www.easyinsurancenewsletter.com For answers, we turn to insurance by clicking “Join Live Demo.” marketing expert Chris Chapin. 200 tons of third-class, bulk-rate mail each year. Especially if it has a “corporate” look to it, the kind they know are going out to thousands of others, those mailings are easy to dismiss. And many Americans sort their daily mail right over their kitchen garbage cans, without even opening it. What can I do to combat that? Ted Janusz is a professional speaker, author and marketing consultant who speaks at PIA conferences to demystify social media marketing for insurance agents. Contact Ted at www.januspresentations.com. Chris: Yes, it is easy for recipients of junk mail to throw away unwanted solicitations. The same holds true for e-mail. Ted: Insurance needs may not be topof-mind for many consumers, like the needs for a new washer, soccer camp, or braces for their kids. What are some ways that I as an insurance agent can keep my services in the forefront of my clients’ awareness? Chris: I have talked with insurance agents who do things in the community, whether at a school or some kind of community service. Clearly, that is a good marketing tool. The issue is that these tend to be onetime activities. The agents then have to think of something else to do. I focus on e-mail, and here’s why: just about everyone now has an e-mail account. So the easiest and most costeffective way to stay top of mind with a large number of people is to send When you do, be sure to have something of interest to them or is entertaining to the client. And as long as you have permission from the recipients to send the newsletter, you’re now in front of many people with minimal effort. As long as they are sent regularly, e-mail newsletters are a very smart way to stay in touch. Rotating topics to include the full spectrum of your offerings is a great way for your clients and prospects to get an idea of the breadth of your expertise. Weekly is probably too frequent and quarterly is not soon enough, so think of sending an e-mail newsletter as a monthly to-do. Ted: American consumers get nearly So the key is to ask for permission first, and to make the e-mail look like it’s personal for them. According to the CAN-SPAM act, anyone who does business with you has, in effect, already given you permission to send them e-mail communications. As long as you include a convenient and easyto-use unsubscribe feature, you are compliant with the act. But to have maximum impact, talk up the benefits of your e-mail newsletter with the new people you meet every day. The first thing you should look for on a new business card that has been handed to you is the e-mail address. If you see it there, ask for permission to send your newsletter. If it is not there, October 2011 • Page 15 ask to write it down and then ask for permission to send your newsletter. Once a new habit has been established in your routine, your e-mail list will grow quickly. Ted: Sending e-mails may be a faster, more convenient and cost-efficient way to reach my clients regularly. But, frankly, I don’t have a lot of my clients’ e-mail addresses. How can I get more of them? Chris: E-mail addresses are an amazingly valuable asset. At least they are if you have them. There is real value to having access to e-mail addresses for everyone you work with. It is well worth the investment to hire a college student, a retiree, or temporary staff person part time to call and obtain e-mail addresses from those clients or prospects for whom you are lacking e-mail addresses. This effort also affords the caller the opportunity to mention the benefits to the client or prospect of the regular e-mail newsletter that you send. Nobody necessarily wants to get a “newsletter,” but they do want to get the benefits the information can give them. So don’t just have them ask, “Do you want to get my newsletter?” communications I send to clients? Chris: Let me begin with what you shouldn’t put in . . . sales pitches. At least 90 percent of your content needs to be informational, entertaining and personal. Then the other 10 percent can be promotional. Remember what it is like to have an ordinary conversation with someone, like we are having now. To get things moving, you ask the other person a question. The result is: the other person starts talking. In e-mail newsletters, their “titles” are whatever is contained in the subject line of the recipient’s inbox. Include a question in the title of your newsletter. Along with the name in the “from” box, your recipient’s first glimpse of you is the question that appears in their inbox. If it is properly phrased, it will cause them to open the e-mail for a closer look. Now most busy insurance agents don’t have either the time or the inclination to both learn how to use the tool and then search for content. As a result, you should look for an e-mail marketing provider that specializes in the insurance industry who is able to provide you appropriate content for quick inclusion in your regular newsletter. Regularity is the key. It does you little good to send out monthly newsletters . . . twice a year. Your readers will see your efforts as being half-hearted and the benefits to both them and to you will be greatly reduced. If, on the other hand, you make a serious resolve to stay top-of-mind with your constituents, and you actually do it, your client retention will go up. And prospects will begin to turn to you, first with questions prompted by your regular outreaches, and then with requests for quotations. It’s a process, and it all begins with that first step to communicate. Ted: I am an insurance agent, not an author. But I want to communicate with my clients using e-mail. How can I do it? Once your client and prospect databases are up-to-date, you will never need to address this issue again, as you continue to update your e-mail addresses every day. Chris: There are a number of general purpose e-mail marketing companies, all of which offer terrific technologies. I am thinking of services like ConstantContact, iContact and MailChimp. Ted: What should I say in the e-mail The catch is that since these compa- Page 16 • October 2011 nies do not provide content, the user needs to create content themselves or find appropriate content on the Internet. October 2011 • Page 17 Advertise Today! 2012 CISR Schedule Contact Jody at the PIA office at (800) 349-3434. Personal Residential January 17: Shreveport January 18: Lafayette January 25: New Orleans January 26: Baton Rouge Commercial Property March 14: Shreveport March 15: Lafayette March 21: New Orleans March 22: Baton Rouge Register today at www.piaoflouisiana.com or call (800) 349-3434. Small Office Tenant Package Auto Physical Damage Commercial Property General Liability Inland Marine Cargo And More!!! 1-800-661-7905 Fax: 318-768-3025 PO Drawer 887 Ruston, La 71273 FOREST INSURANCE FACILITIES Commercial Wholesale Brokerage Wayne Forest Wayne Forest Jr. Matthew Forest Specializing in: • Property, Casualty, Inland Marine • Umbrellas and Packages Debbie Libasci Courtney Kelly Stacy Lauer 2901 N. I-10 Service Rd. E., Suite 300, Metairie, LA P.O. Box 7635, Metairie, LA 70010-7635 PHONE: (504) 831-8040 FAX: (504) 831-4499 Page 18 • October 2011 Continued from page 12 (Partner News) Two representatives of Midwest Occupational Health—Research Director Trang Nguyen, MD, PhD and David C. Randolph, MD, MPH—discussed the use of medical evidence to address treatment of low back pain and medically unexplained symptoms. 16514 Tapco Ad - Agent's Voice, Oct LWCC Medical Director Katharine C. Rathbun, MD, MPH discussed work limitations and drug authorizations. LWCC Medical Chiropractic Consultant Charles Herring, DC gave a presentation titled “The Biopsychosocial Patient: Functional Improvement and Applying the Louisiana 2011.pdf 1 9/14/11 2:32 PM Medical Treatment Guidelines.” In addition, a panel discussion featured comments by Rathbun, Herring, neuropsychologist Kevin Bianchini, PhD and Suzette Price of Mitchell International, Inc. Their topic was “The Application of Medical Guidelines to Improve Functional Capacity and Return-to-Work.” PowerPoint presentations on topics from the conference are available on the web at www.lwcc.com. Continued from page 10 (Errors & Omissions) In addition, in many states, the account cannot be placed in the E&S market if there is an admitted market willing to write the risk. It is essential that you comply with these regulations. What is served quicker than fast food? Restaurant & Deli coverage in a five-minute phone call Hard market or soft, E&S can be a tremendous asset to your agency While the E&S industry has significant uniqueness to it, you will need this side of the industry for certain risks. Establish a solid relationship with several wholesalers, as no one can do it all – and be on the lookout for the issues discussed above … because an ounce of prevention is worth a pound of cure. Call. Quote. Bind. Using TAPCO’s courteous and prompt call center, Restaurant & Deli coverage can be quoted, bound and delivered to your e-mail inbox quickly and accurately during one five-minute phone call. The TAPCO Service Pledge • “A”-rated non-admitted carrier • Competitive pricing • Fast policy turnaround • In-house financing available • Quick claims handling • $10 credit to your personalized TAPCO EZ Bucks Visa debit card with each policy • Visa, MasterCard and ACH payments accepted 1,000 Strong More than 1,000 classes of P&C business written under binding authority. 800-334-5579 www.gotapco.com October 2011 • Page 19 YIPs nd u o Ar Bowl-A-Thon e t a t S the Page 20 • October 2011 nd u o Ar te a t S the 2011 CISR Conferment Ceremony Attendees Brenda Bradley Cammi Smith Allison Hartdegen Patsy Wells Diana Schehr Pamela Lambert Laura Calcagno Marion Houston Catharene Jones Christine Midkiff Regina Diodene’ Amber McLin Deidra Lopez Suxanne Rogers Jessica Dixon Alexis DeJean Layla O’Brien Teresa Brose Lauralei Augustine Mark Abshire Alicia Brauer Loren Buscher Courtney Dupuis Emily Putnam October 2011 • Page 21 Continued from page 4 (President’s Message) Continued from page 8 (Passing It On) identical messages. If you receive a request to forward an e-mail to your legislator, please do. If you have time, customize it, and most importantly attend district events and voice your opinion. commodity. The research clearly shows that many of the areas in which you provide added value, as independent agents, have a high level of importance for the vast majority of customers. This is great news - customers want what agents have to offer. By using the results from this research, agents can proactively deliver what customers want. In my opinion, the most important event was Louisiana’s own Richard Clements being elected to the National Executive Committee as Secretary-Treasurer. Richie will be National President in 4 years. Richie is well respected in the PIA, as is the PIA of Louisiana. Did you know that Richie will be the 4th National President from Louisiana? The others include Dan Blum, Mike Grace, and Robert Page. In three of the meetings that I attended, Louisiana was used as a positive example. We have our Executive Vice-President, Jody Boudreaux, to thank, as well as all prior leaders of our PIA. However, the most important people in our organization are our members, without you we would not exist. And, a little more about the survey that was conducted. The research is national in scope and scientifically accurate with a confidence level of 95% and a margin of error of plus or minus 4%. This survey is extremely reliable and I think you’ll be pleasant surprised by the findings. If you ever wanted to know what your customers really thought, this is a great way for you to take a look. And what’s even better than that, is this process doesn’t end there. When you’re left wondering, “Ok, now what?” you’ll find this web site offers you tools to take the next steps to start taking advantage of what you’ve heard from insurance consumers. Again, check it out at www.agencytouchpoints.com. Make it an exercise for you and your staff today! And, we’d love to hear your feedback. Just a thought in closing: “Nobody cares if you can dance well, just get up and dance.” Page 22 • October 2011 First Premium® insurance GrouP, inc., cmGa We are your Mobile & Manufactured Home Specialists Mobile/Manufactured Home Insurance is a form of homeowner’s insurance that covers mobile or manufactured homes as well as tied down travel trailers. This policy is for units used as principal residences, secondary or seasonal residences, rentals, or as commercial offices. 190 New Camellia Blvd • Covington, LA 70433-7812 (800) 256-2171 • www.firstpremium.com “Serving Today’s Insurance Professionals Since 1973” October 2011 • Page 23 Did you know that PIA has defended the crop insurance program and agents who sell crop insurance from an attack on both? In an August 26, 2011 opinion article in the Grand Forks Herald (North Dakota), Eli Lehrer, a vice president for The Heartland Institute, argues that the U.S. crop insurance program is a waste of taxpayers’ money, and the $6.5 billion spent on it each year is an egregious example of welfare for business. Lehrer argues for the complete elimination of the crop insurance program. He goes on to say that agents who sell the policies get “enormous commissions” that serve to “reduce competition between the companies that write crop insurance.” Lehrer is a member of a coalition, GreenScissors, which has also called for the eventual elimination of the National Flood Insurance Program (NFIP). This unusual coalition includes representatives of the environmental group Friends of the Earth, Taxpayers for Common Sense and Public Citizen, an advocacy group founded by Ralph Nader. PIA National responded to Mr. Lehrer’s preposterous allegations, first in a statement to BestWire and then in an op-ed in the September 8 Grand Forks Herald. PIA will not allow such attacks to go unanswered. You can read Mr. Lehrer’s article and PIA’s response here: www.pianet.com/crop PIA fights for agents and the issues that are important to them everyday. If you are not a PIA member, please join today. To learn more about PIA membership, please give us a call or visit us online at www.pianet.com/AboutUs/JoinPia. National Association of Professional Insurance Agents 400 N. Washington St. Alexandria, VA 22314-2353 www.pianet.com [email protected] (703) 836-9340 Our Liability Coverage Also Covers Events That Are Behind You. Get free “tail” coverage with The Physicians Trust. With The Physicians Trust, you’re not only covered for the future, you’re covered for the past, too. That’s because our professional liability policies include tail coverage at no extra cost. You’ll also enjoy competitive pricing that only a not-for-profit organization can offer, plus accelerated underwriting for quick decisions. For a quick, no-obligation quote that could save you up to 20%, contact Karen Harrison at (225) 368-3825 or [email protected]. Administered by HSLI ThePhysiciansTrust.com | (225) 368-3888 4646 S he rwood C ommon B l v d. | B at on R ouge , L A 70816 Page 24 • October 2011 Louisiana Legal Updates Insurance The Fourth Circuit Court of Appeal, en banc, decides that a guest passenger, non resident, non relative, is entitled to uninsured motorist coverage, even though such passenger is not defined as an “insured” under the UM policy definitions. This finding is based on the fact that any person covered by liability coverage is also entitled to UM coverage. Since the guest passenger would be entitled to liability coverage under the omnibus statute, then the policy must be reformed to recognize that the passengers are also entitled to UM coverage. Several judges dissented from the majority ruling, and writs are certain to be filed to the Louisiana Supreme Court. Bernard v. Ellis --- So.3d ----, 2011 WL 4469822 La.App. 4 Cir.,2011. September 27, 2011 General Liability Alonzo v. Safari Car Wash, Inc. --- So.3d ----, 2011 WL 4469105 (La.App. 5 Cir. 9/27/11). Customer and his wife filed suit against car wash, seeking damages for personal injuries customer sustained when he allegedly slipped and fell in puddle of water outside car wash’s customer restroom, and customer’s wife sought damages for loss of customer’s love and affection sustained as a direct consequence of husband’s fall. The 24th JDC Judge Glenn B. Ansardi, granted summary judgment to car wash. Customer and his wife appealed. The Court of Appeal held that customer failed to establish the existence of a condition which presented an unreasonable risk of harm. The appellate court found that the record indicated that George Alonzo testified that he was unable to identify the condition of the floor in defendant’s premises on the date of the fall. Although plaintiffs cite to circumstantial evidence to overcome their burden of proof, we fail to find that plaintiffs’ claim that the floor must have been wet to be sufficient to meet plaintiffs’ burden of proof in this matter. Workers Compensation An employee challenged an employer’s conversion of indemnity benefits from TTD to SEB. At trial, the employer produced evidence that the claimant’s treating physician had approved the claimant to return to work, but only 2 jobs had been identified by the vocational rehabilitational counselor that were within the claimant’s restrictions. Noting that neither job had been offered to the employee, the court declared that while the employer had appropriately switched benefits to SEB based upon the employees release to light duty work, SEB payments needed to be made at the full rate, since there was no evidence of any earning capacity.Sharp v. Landscape Management Services, --- So.3d ----, 2011 WL 4579149 (La.App. 3 Cir.), 2011-0340 (La.App. 3 Cir. 10/5/11). When a consent judgment was timely paid, but the check issued had transposed two numbers, resulting in a $0.90 underpayment on a check that was supposed to have been for $14,708.70, the Third Circuit affirmed the decision of the workers’ compensation judge assessing the employer with a $3,000 penalty and an additional $3,000 in attorney’s fees over the 90 cent underpayment, for what appeared to have been nothing but an innocent error, noting that it was something within the control of the employer. Richard v. Culvert & Supply, Inc., --- So.3d ----, 2011 WL 4578592 (La.App. 3 Cir.) 2011-232 (La.App. 3 Cir. 10/5/11). The Third Circuit awarded 4 separate $3,000 penalties for 4 separate violations of the same consent judgment.Weldon v. Holiday Inn-Jennings, --- So.3d ----, 2011 WL 4578587, (La. App. 3 Cir.), 2011-203 (La.App. 3 Cir. 10/5/11). Employment An employee was terminated, then subsequently re-hired on a temporary basis. The employee filed an Age Discrimination in Employment Act (ADEA) claim against the employer, and prevailed at trial. The Fifth Circuit Court of Appeal reversed, finding that the ADEA’s 180 day limitation period for filing a discrimination charge with the Equal Employment Opportunity Commission (EEOC) was not equitably tolled during the period the employee was temporarily rehired, and that the 180 day time period ran from the date of initial discharge. Phillips v. Leggett & Platt, Inc., --- F.3d ----, 2011 WL 4375674 (C.A. 5 (Miss)). The Fifth Circuit held that ERISA imposes on the employerfiduciary the same responsibilities imposed on a fiduciary under the common law of trusts, and that the ERISA employer-fiduciary’s duty includes forwarding information to employees which the beneficiary knows the employee is not aware of but needs to know for the employee’s own protection. Finding that this duty was breached, the court concluded that an appropriate award was the loss and depreciation of the former employee’s profit sharing account between the date of the employee’s resignation and the date the employer was aware that the employee was seeking information about the profit sharing plan.Kujanek v. Houston Poly Bag I, Limited, --- F.3d ----, 2011 WL 4445993 (C.A. 5 (Tex.)). Source: Ungarino & Eckert, LLC October 2011 • Page 25 Member Benefit in Focus Index of Advertisers Accu-Auto……………………………..….....…...….....5 Emergency Restoration Inc. ....................….…....22 First Premium Insurance Group.............….…....23 Forest Insurance Facilities……………………….....18 Hull & Company, Louisiana………………….……...23 Imperial Fire & Casualty Insurance…………….....17 LEMIC Insurance Company………………...…......24 LUBA Workers’ Comp……………………..Back Cover LWCC…………………………………Inside Front Cover North Central Agency……………………….…….….. 18 Agency Management Tools offered to you by PIA National: Reaching Gen Y. Based on extensive focus group research with Gen Y age group insurance consumers, this online tool, developed by The Partnership, helps agents understand and reach this important age group. Beyond the research itself, this new online resource pro¬vides agencies with tools they can use to convert Gen Y age group prospects into loyal agency clients and customers. • Perpetuation Central. Developed by The Partnership, this hands-on inter-active tool is designed to guide agencies through the decision making, planning and implementation steps of agency perpetuation or ownership transfer. • Agency agreement review service. Free to members and carriers, PIA recommends changes to carriers and high-lights concerns for members so they can make informed decisions about the agreements they sign. Southern States General Agency.....................22 • Practical Guide to Successful Planning. This online tool, developed by The Partner¬ship, is designed to help agents plan for success within their own agencies. It also helps agents coordinate their own plans with those of the carriers they represent. Stonetrust...................................................7 • Online data backup and recovery services. Tapco Underwritters...........................................19 • Discounted producer licensing services. Available from Sircon and Central Licensing Bureau. Physician’s Trust ..............................................24 Progressive…............................Inside Back Cover The Timbermen Fund.........................................10 Find out more details on advertising in The Agent’s Voice by calling the PIA office at (800) 349-3434. • Employee profiling. Hire the right people with skills and personality testing from OMNIA. • Disaster recovery manual. • PIA credit cards from Bank of America. • Discounts on car rentals from Alamo, shipping with UPS, and calendar products from Mines Press. • Free subscription to Rough Notes magazine. Page 26 • October 2011 More Agents are Selling Preferred and Earning Higher Commission in Louisiana with the Signature Agent Program. ® Congratulations to the following agents who have joined the Progressive Signature Agent® program in July. Boswell Insurance Agency Shreveport Epperly Insurance Lafayette Stone Insurance, Inc. Mandeville Bourg Insurance Agency, Inc. Donaldsonville Emery & James, Ltd. Hammond TWFG Insurance Services Lake Charles Community Financial Monroe Grant C. Bennett Insurance Slidell TWFG Insurance Services Mandeville Courtney Insurance Hammond Integrity Insurance, Inc. Livingston Dupre Carrier Godchaux Opelousas Southern Costal Insurance Covington They join an elite group of agents already in the Signature Agent Program. A Foto Insurance Laplace Bruni Insurance Agency Morgan City Harlan Insurance Agency Alexandria Pam Price Insurance, Inc. Jena The Firm of Louisiana Lake Charles A Victory Agency, Inc. Bogalusa Castello Agency Zachary Insurance Network of LA Baton Rouge Pat Leboeuf Insurance Westwego The Hopper Agency Farmerville A Victory Agency, Inc. Mandeville Curtis Insurance Agency Lake Charles J. Everett Eaves, Inc. New Orleans Plescia Insurance Agency Slidell Thomson, Smith & Leach Lafayette ABC Agency Network Houma David Cordell Insurance Baton Rouge John Kelly Dabdoub Mandeville Pontchartrain Insurance Kenner Tim D'Angelo Insurance Agency Marrero Action Insurance, Inc. Lafayette DJW Insurance Agency New Iberia Liggio Insurance Agency Lafayette Premier Metro Group Metairie Total Insurance of Watson, Inc. Denham Springs Advanced Insurance Solutions Hammond Eagen Insurance Agency Metairie Louisiana Independent Insurance Metairie Quality Plus Lafayette Toups Insurance Agency Thibodaux Alliance Insurance Agency Metairie Gary Losey Insurance Baton Rouge Moore-Jenkins Bogalusa Riverlands Insurance Services Luling Warren Tibbetts Baton Rouge Barry Hebert Insurance Metairie Gendusa Insurance Agency Hammond Moore-Jenkins Franklinton Shaver Robichaux Agency Thibodaux Beasley-Keith, Inc. Bossier City Glenn Dean Insurance Agency Deridder Page & Sons Insurance Agency Houma Steve Teal Insurance Slidell SIGnATurE AGEnTS rECEIVE: 15/12 commission on preferred auto business. A $2,000 marketing allowance to co-op with Progressive on advertising or marketing materials. recognition as a Progressive Signature Agent in select advertising, along with special signage for your agency and identity items for your staff. Free one-year subscription to Progressive’s online directory listing program, ListAgent. You can join the program in January or July by writing an average of one preferred auto policy a week over the previous six months. Then, just keep writing one preferred auto policy a week throughout the year to maintain your Signature Agent status and benefits. Contact your account sales representative to learn more about how you can become a Signature Agent. ©2011 Progressive Casualty Insurance Company and its affiliates, Mayfield Village, Ohio. 09A00214.AP.LA2 (08/11) Prsrt Std U.S. POSTAGE PAID BATON ROUGE, LA PERMIT NO. 935 8064 Summa Avenue, Suite C Baton Rouge, LA 70809 YOU’RE NOT ALONE. Thanks to LUBA Workers’ Comp. With our online quoting, competitive r a t e s , a g g r e s s i v e c l a i m s m a n a g e m e n t , a n d a n A M B e s t r a t i n g o f A- Excellent, we can help you navigate around the potential obstacles you face whenever they occur, wherever you are. It’s our way of taking service to a whole new level. Visit lubawc.com. LUBA | Loo-buh | – Does the sound of good service ring a bell? 11LUBA019 Forest_PIA_7.5x6.indd 1 6/3/11 11:22 AM

© Copyright 2026