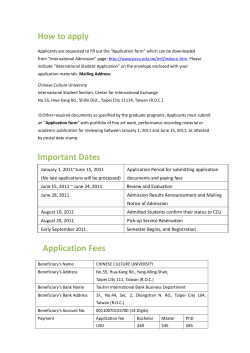

Expression of Interest For (EOI)