SAMPLE MIDTERM – BUS 251

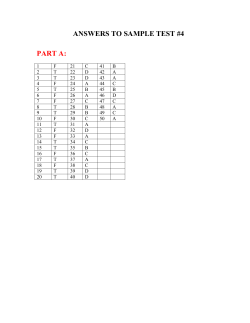

SAMPLE MIDTERM – BUS 251 Your midterm will also have theoretical questions where you will be asked to explain an accounting idea in words. You may want to review the sample ones on exam guidance or ones on mini-midterms. Section 1: THE ACCOUNTING CYCLE (40 MARKS = 40 MINUTES) Andy’s Yard Care Service Company Limited (AYC) Andy Smith has been operating for 3 years. The company provides lawnmowing, tree trimming and weeding services to private residences in the lower mainland. Andy incorporated the company on January 1 st, 1996 and contributed equipment with a fair market value of $50,000 to the business in exchange for common shares valued at $10,000 and a $40,000 loan, payable to Andy. The following is the trial balance for AYC at January 1st, 1999: Debit Cash $ 23,500 Accounts Receivable 18,000 Supplies Inventory (1) 1,000 Equipment (2) 50,000 Accounts Payable Wages Payable Loan Payable (3) Accumulated Amortization – equipment Common Shares Retained Earnings $ 92,500 Credit $ 6,000 5,000 40,000 30,000 10,000 1,500 $ 92,500 (1) Consists of fertilizer and topsoil, used in lawn care. (2) Contributed to the business January 1, 1996, estimated to have a 5 year useful life, with no residual value. (3) Shareholder loan payable bears interest at 10% annually. Interest on the loan is paid on June 30th and December 31st each year. Andy does not anticipate receiving any payments on principal until the business becomes better established. REQUIRED: (28 marks for journal entries, 12 marks for balance sheet) i) Prepare journal entries for the 1999 information provided on the next page, or explain why no entry is required. (Clearly label each account affected, but detailed explanations for each entry are not required). CLEARLY STATE ANY ASSUMPTIONS THAT YOU FEEL ARE NECESSARY. 1 ii) Prepare any adjusting entries required at March 31 st, 1999. It is not necessary to prepare an entry to close the accounts. iii) Prepare a balance sheet at March 31st, 1999, in good format. 2 INFORMATION FOR THE FIRST 3 MONTHS OF 1999 1. Services Revenue: The company billed customers $48,150 for work done between January 1st and March 31st. This included GST charged to customers of $3,150. (We did not cover GST so you can ignore) 2. At March 31st 1999 there was $6,000 owing from customers that had not yet been collected in cash. 3. Operating expenses (not including wages) incurred in the three months were $11,500. All operating expenses are initially on credit. 4. AYC paid $14,000 to suppliers between January 1 st and March 31st, 1999. 5. Wages earned by employees between January 1 st and March 31st, 1999 were $8,500. There were no amounts owing to employees at March 31 st, 1999. 6. Supplies inventory costing $1,500 was purchased for cash. A count in the storeroom on March 31st, 1999 showed that there were supplies costing $1,200 on hand. 7. Andy purchased three new ride-on mowers on January 1 st, 1999, for $6,000 each. He paid $10,000 in cash, and signed a note promising to pay the balance in nine months (the end of his busy summer season). There will be no interest paid on the note. The mowers are expected to have a 3 year life, with no salvage value. 8. On March 31st, 1999, Andy signed a contract to purchase a fourth new ride-on mower. This mower will be delivered to Andy in July, and will cost $8,000. 9. Andy estimates that approximately $3,500 of the accounts receivable at January 1st, 1999, which have still not been collected at March 31 st, 1999, will not be collectible. 10. Andy estimates that income taxes for AYC will be $12,000 for the 1999 year. These taxes will be paid in March in the year 2000. Due to high start-up costs in the first three years of operation, AYC has not had to pay income taxes before the 1999 fiscal year. 3 Section 2: MULTIPLE CHOICE (20 QUESTIONS = 40 MARKS = 40 MINUTES) 1. Not covered 2. Which of the following would require an adjustment to the cash balance in the company’s accounting records if discovered through the bank reconciliation process: a) Outstanding deposits b) Outstanding cheques c) Bank service charges d) All of the above 3. Which one of the following would NOT be recorded as an asset by a business? a) Land not currently being used, but held for future development b) Accounts due from customers who have received products from the company c) A five year employment contract with the President, who has improved the company’s performance significantly d) Cash owing to the business from employees 4. Working capital is a measure of the company’s: a) Cash b) Ability to pay long-term debts c) Resources available to produce inventory for the next year’s business d) None of the above (are accurate definitions of working capital) 5. Which of the following transactions would result in a decrease in assets and a decrease in shareholders’ equity? a) Paying dividends payable b) Purchasing land for cash c) Paying the monthly electric bill d) Receiving cash on account 6. Which of the following would NOT be included on the Cash Flow Statement? a) The declaration of a dividend in the year b) The purchase of capital assets for cash during the year c) The repayment of long-term debt d) The issuance of common shares 4 7. Transactions that can have an effect on the decisions of shareholders are referred to by accountants as: a) Material b) Completed c) Unqualified d) Reliable 8. How much information to show on the financial statements and where to report it, are issues of: a) Recording b) Adjusting c) Transactional analysis d) Disclosure 9. Not covered 10. The income statement emerged as a standard financial statement based on a demand for which of the following? a) Performance measurement information b) Cash flow information c) Internal management information about the efficiency of operations d) Information regarding changes in owners’ claims on assets 11. Making sales on account results in which one of the following impacts on the balance sheet? a) Increases cash and increases accounts receivable b) Increases sales and increases accounts receivable c) Increases cash and increases sales d) Increases accounts receivable and increases retained earnings 12. Not covered 5 13. Creations Limited started business on January 1st, 1999. On January 5th, 1999 a cheque for $3,000 was written, payable to the company’s landlord, and recorded as Prepaid Rent. The payment was to cover rent on business premises from January 1st to March 31st, 1999. Assuming no other journal entries were made, what adjusting entry would be required on March 31st? a) DR Prepaid Rent 3,000 CR Cash 3,000 b) DR Rent Expense 1,000 CR Prepaid Rent 1,000 c) DR Rent Expense 3,000 CR Cash 3,000 d) DR Rent Expense 3,000 CR Prepaid Rent 3,000 14. Not covered 15. Which one of the following is not an expense of the business in the current period? a) A deposit for equipment you will receive next year b) An estimate of the costs of warranties provided to current period customers c) Amounts owing to employees (but not yet paid) for work performed this period d) None of the above (all are expenses) 16. Not covered 17. Which of the following characteristics best describes why we use the accounts, bad debts expense and the allowance for doubtful accounts in the financial statements? a) Matching b) Materiality c) Relevance d) None of the above 18. An item of inventory, which cost $10 when purchased last year, is sold today to a customer, on account, for $25. Which of the following statements is true? a) ‘Gain on sale’ in the current year’s income statement will be $15 b) Shareholders’ equity increases this year by $15 c) The increase in cash this year is $15 d) All of the above 19. Which of the following journal entries should be used to write off an accounts receivable deemed uncollectible where the company has created an allowance for doubtful accounts? a) Debit bad debts expense, credit allowance for doubtful accounts b) Debit allowance for doubtful accounts, credit accounts receivable c) Debit bad debts expense, credit accounts receivable d) Debit allowance for doubtful accounts, credit bad debts expense 20. Excelsior Company had sales to customers during the year of $40,000. The company records a gross profit percentage of 60% [gross profit % = (sales revenue – COGS expense)/sales revenue]. The company’s cost of goods sold expense in the year was: a) Cannot tell from the information provided 6 b) $24,000 c) $16,000 d) None of the above SOLUTION Section 2 - MCQ 1. C 2. C 3. C 4. D 5. C 6. A 7. A 8. D 9. B 10. A 11. D 12. A 13. D 14. D * 15. A 16. C 17. A 18. B 19. B 20. C * Assumes the $250 cost of the inventory thrown away is not included in “Cost of goods sold expense “ on the I/S, it would be included in a ‘loss’ account. Section 1 – THE ACCOUNTING CYCLE DR CR CR A/R (A↑) Sales Revenue (SE ↑) GST Payable (L ↑) DR 48,150 45,000 3,150 Cash (A ↑) CR A/R (A ↓) [Jan.1/99 $18,000 + 48,150 – Mar.31/99 $6,000] 60,150 DR Operating expenses (SE ↓) A/P (L ↑) 11,500 CR A/P (L ↓) Cash (A ↓) 14,000 CR DR DR DR 60,150 Wages expense (SE ↓) Wages payable (L ↓) CR Cash (A ↓) DR CR Supplies inventory (A ↑) Cash (or A/P) DR 11,500 14,000 8,500 5,000 13,500 1,500 1,500 Operating expenses (SE ↓) CR Supplies inventory (A ↓) [Jan.1/99 $1,000 + $1,500 – Mar.31/99 $1,200] 1,300 DR 18,000 CR CR Equipment – mowers (A ↑) Cash (A ↓) Note payable (L ↑) 1,300 10,000 8,000 7 Transaction 8. No entry required as no exchange has yet taken place (signed contract only – no exchange of cash or delivery of equipment). DR CR Bad debts expense (SE ↓) 3,500 Allowance for doubtful accounts (XA ↑) 3,500 DR Income tax expense (SE ↓) 3,000 CR Income tax payable (L ↑) 3,000 [Accrual of income tax. Based on estimate $12,000 x 3/12, assumes income earned evenly over the year.] Adjusting entries DR Amortization expense (SE ↓) 2,500 CR Accumulated amortization – equipment 2,500 [$10,000 per year x 3/12] (XA ↑) DR Amortization expense (SE ↓) 1,500 CR Accumulated amortization – mower (XA ↑) 1,500 [$18,000/3 years = $6000 per year x 3/12] DR Interest expense (SE ↑) CR Interest payable (L ↑) [$40,000 x 10% x 3/12] 1,000 1,000 AYC Balance Sheet March 31, 1999 ASSETS: Current assets: Cash A/R $ 6,000 Less: Allowance for doubtful accounts 3,500 Supplies inventory Total current assets Non-current assets : Equipment $68,000 Less : Accumulated amortization 34,000 TOTAL ASSETS LIABILITIES & SHAREHOLDERS’ EQUITY: LIABILITIES Current liabilities: A/P GST Payable Interest Payable Note Payable Income tax Payable Total current liabilities Non-current liabilities : Loan Payable $44,650 2,500 1,200 $48,350 34,000 $82,350 $ 3,500 3,150 1,000 8,000 3,000 $ 18,650 40,000 8 TOTAL LIABILITIES $ 58,650 SHAREHOLDERS’ EQUITY: Common shares $ 10,000 Retained earnings ($1,500+12,200*net income) 13,700 TOTAL SHAREHOLDERS’ EQUITY $ 23,700 TOTAL LIABILITIES & SHAREHOLDERS’ EQUITY $ 82,350 * Net income = $45 – ($11.5 + 8.5 +1.3 +3.5 +3 +2.5 + 1.5 + 1) = $12.2 (in thousands) 9

© Copyright 2026