ABC

docz

Explore

Log in

Create new account

Download

Report

law, govt and politics

Part IV- Items of General Interest Revenue Procedure 2003-35

WORK EXPERIENCE REQUEST LETTER EXAMPLE

California State University Study Abroad Insurance Claim Form

HOW DO YOU WRITE A LETTER OF APPLICATION?

*write the perfect cover letter Prepared by Prospectus

Acceptance & Rejection Letters Guide

Cover Letter Explanation Your address Phone Number Date

Crafting a Cover Letter: Career Guide

Writing an Effective Cover Letter

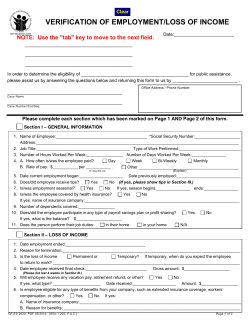

VERIFICATION OF EMPLOYMENT/LOSS OF INCOME

© Copyright 2026

About abcdocz

DMCA / GDPR

Report