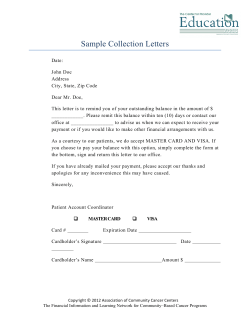

Our terms and conditions for Mer chant a