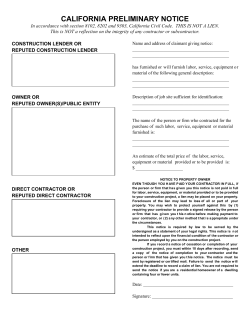

CONTRACTOR’S BUSINESS AND LAW REFERENCE MANUAL DIVISION OF BUILDING SAFETY