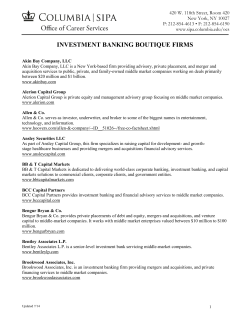

Understanding how to handle the acquisition process