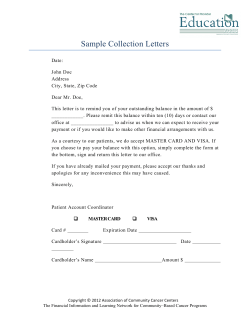

Merchant Agreement