The simpler path to stable absolute returns is not

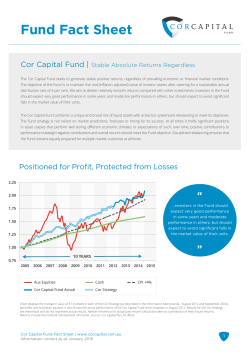

The simpler path to stable absolute returns is not easy. Davin Hood, Portfolio Manager, The Cor Capital Fund Level 19, 644 Chapel Street, South Yarra, Australia 3141 Email: [email protected] ; Tel: (61) 3 9823 6296 ; www.corcapital.com.au Intelligent asset allocators understand that human nature, intuition and a focus on immediacy rarely combine well for successful investing. It is also likely they understand the investment advice and management industry (with exceptions) to be more a massive exercise in group think and business risk management than anything else. Even armed with this knowledge, the consensus is such a strong force that few venture into the domain of contrarian investing and those who do often retreat soon after. The competitive marketing of investment products or ideas capitalises on investors’ natural desire to predict the best returning asset and then to concentrate investment towards it. It is much easier to sell the idea of reducing exposure to assets that have fallen in value and increasing it to assets that have risen in value. And gaining the benefits of these actions immediately is naturally preferable also. The consensus view will always remain an excellent place to look for opportunities for those with a counterintuitive temperament. However, many investors struggle with the discipline and emotional challenges required to profit from taking contrarian positions. In my experience positions are often too large and volatility too difficult to accept, regardless of how reputable the source of the idea may have been. One way to improve overall investment results, and particularly the emotional experience of taking contrarian positions, is through combining an alternative approach to portfolio structure with active rebalancing, which by its very nature is contrarian. The benefits of such a strategy are underappreciated and underutilised but valuable to those seeking stable absolute returns. Figure 1 : Stable Absolute Returns – no derivatives, no gearing, no short‐selling. 2.25 2.00 1.75 1.50 1.25 1.00 10 YEARS 0.75 12/2004 12/2005 12/2006 12/2007 12/2008 12/2009 12/2010 12/2011 12/2013 Aus Equities (before fees) Cor Capital Fund Actual (after fees) Bank Bills Cor Strategy (after fees) CPI+4% 12/2014 Source: Cor Capital, IRESS Page 1 of 4 12/2012 At your local brokerage or private bank a discussion about portfolio balance will include the subject of optimisation, which in simple terms means adjusting the weights in your portfolio for volatility and return. In my opinion it is backward‐looking and not overly useful given what is known about investor behaviour in the presence of volatility. For example, research by Dalbar Inc.1 concludes that the average US equity mutual fund investor achieved only slightly more than half the annual return of the S&P500 over 20 years due to bad timing, with the majority of that due to psychological issues. A portfolio that is optimised may leave investors with too much exposure when an asset surprisingly falls and not enough when one surprises on the upside. To achieve stability and be prepared for unpredictable events, without adding complexity by using derivatives or gearing for example, a portfolio must maintain absolute balance and diversification. This means having significant allocations to uncorrelated assets of equal or similar size. The Cor Capital Fund#, of which I am manager, maintains such an allocation and in the interests of liquidity it holds only cash, bonds, equities and gold bullion. All assets are domestic in nature and have performed differently during particular economic and financial market environments, or following changes in expectations about such environments. The positions are significant and equal in size (25 percent) which is where the mental challenges begin. Few mainstream advisers will recommend you have a quarter of your portfolio in gold bullion and are likely to warn that having less equities and more cash will eat into your returns. They may also point out that correlations change and that these assets sometimes move in sync. In my experience that is only the case for shorter periods and the inherent qualities of each asset dictate that it won’t last. The specific asset allocation we employ may appear simplistic but deviating from it implies assumptions about the future that we don’t wish to make. Many readers will know this strategic allocation as Harry Browne’s simplified permanent portfolio but it is only part of the story. To maintain stability, absolute balance must be maintained and I believe a more active approach to rebalancing will generate the best rewards when combined with discipline. Portfolio rebalancing as a strategy is no secret. What is underappreciated is that its benefits are enhanced with broader diversification and where constituent assets are uncorrelated, volatile and mean reverting. According to Bouchey et al2: “The excess return from volatility harvesting is not an expected arithmetic excess return derived from forecasting skill, security selection, or an informational advantage. Rather it is the excess compounded return generated from rebalancing volatile assets over multiple time periods. This excess growth is available in liquid markets with assets that have volatilities greater than zero and correlations less than one. However, only investors with the discipline to trade systematically will harvest this extra growth”. Discipline is the key and it is where many investors fall down. However, it is a lot easier to be disciplined when rebalancing than it is when opening or closing larger positions. When rebalancing a portfolio in this way you are selling assets that have become popular (more likely to be expensive) and buying assets that are unpopular (more likely to be cheap) and these changes are by definition contrarian. In the Cor Capital Fund we rebalance whenever any asset class is more than 1.5% above or below the initial 25% allocation. This is the system we have developed and we ensure it is sensitive to friction costs such as brokerage and tax. Without careful consideration these can destroy the value added by the strategy. I estimate that our system results Page 2 of 4 in 10 to 15 percent portfolio turnover, which is low. Having these relatively tight rebalancing bands means the benefits of volatility harvesting are maximised and that investor capital flowing in and out of the Fund is similar in exposure to the strategic allocation. In line with my comments above about consensus views and group behaviour, Bouchey et al2 discuss who is on the other side of the trade: “The ‘other trader’ is someone who buys after prices have gone up and sells after prices have gone down. There are a few possibilities: An investor who chases positive performance (greed) but becomes risk averse when returns become negative (fear); A quantitative trader who uses momentum to predict returns; An investment manager who prefers ‘winners’ to ‘losers’; An institution seeking downside protection through a dynamic ‘portfolio insurance’ trading strategy; An institution that receives new cash to invest in good economic times but requires liquidity from its portfolio in bad economic times;” The challenge to what I am proposing here is that mean reversion, or trend reversal, can take a long time to occur. The longer a trend persists, the greater the likelihood of underperformance with this strategy (although you will continue to benefit from the trend). Figure 1 above shows that equities surged up to the end of 2007 and an investment in the Cor Capital Fund appeared way too conservative. The same appears to be the case since 2011. Here I would highlight the comments above about volatility and market timing failures. If many investors significantly under‐perform the stock market index due to behavioural challenges, the benefits of the approach I am advocating become even clearer. You can be an investor who capitalises on volatility; you can’t be ruined by corrections or crashes; you are not reliant on specific outcomes for success; foreign currency risk can also be avoided depending on the chosen strategic asset allocation. Over time your results should be superior to the average with respect to returns and volatility. You will avoid complexity and have capital available for more active investments when opportunities arise. I would add a key point here; the biggest problem with investment management in the world today is the idea that performance is proof of skill, and therefore that it has something to do with future returns. Whether it’s with someone who predicted a currency collapse or last year’s best hedge fund, outside of a very long period of consistent results (or an acceptance of faith), an investment strategy should only be engaged if the logic behind it is understood. Separating skill from excessive risk taking is often impossible. Therefore, finding an approach grounded in relatively straightforward logic and discipline can increase the level of confidence and trust in investing and investment management. The question of whether an investor should attempt to employ such a transparent strategy themselves or invest in an appropriate mutual fund is almost answered for them. For many of the reasons outlined above, there are few funds in existence that invest this way. At the same time, individual investors tend to struggle with the discipline required even if they support the philosophy. This is particularly the case where they have a more active strategy operating to the side (technical trading for example) which may regularly contradict required contrarian portfolio changes. Transaction costs can be an issue for individual investors when higher volatility in constituent assets Page 3 of 4 causes increased rebalancing. I would also suggest caution when using exchange traded funds. It is only following a system shock or after something goes wrong that you will appreciate the more qualitative elements of professional strategy implementation. In the case of my investors in the Core Capital Fund, outside of the psychological challenges of executing the strategy, I would say their decision to use a manager is due to the opportunity cost of their time and a desire to be more active in other areas. They are happy to pay a fee for specialist management and then get on with the things they do best. There is great satisfaction in having a well thought out speculation rewarded. However, there is also a lot in knowing that nothing can harm your portfolio and that you are also capitalising on the human nature of the crowd. Note: Cor Capital employs its strategy using Australian domestic asset classes and gold bullion (unhedged). It has tested its strategy across many developed markets including the US, UK, Canada and Japan over multiple decades. The Cor Capital Fund does not use derivatives, gearing, or short‐selling. 1. Dalbar Inc. (2014). Quantitative Analysis of Investor Behavior 2. Bouchey, Nemtchinov, Paulsen, Stein. (2012) Volatility Harvesting: Why Does Diversifying and Rebalancing Create Portfolio Growth?, Journal of Wealth Management, Volume 15 No. 2. # Page 4 of 4

© Copyright 2026