Business Start Up And Expansion Presentation

Business Start Up

And

Expansion

Presentation

• Comparatively, Jamaica is considered to be very

entrepreneurial. Approximately 17% of the

population had an interest in conducting some

form of business according to a Global

Entrepreneurship Monitoring (GEM) report. The

report further highlighted that, “Jamaica’s overall

rate of entrepreneurial activity compares

favorably with countries such as New Zealand,

(2005 – 28.26%) considered among “the world’s

most entrepreneurial countries”. Further

comparison with nations with similar economic

structure, showed Jamaica ahead of nations like

Argentina, Chile, Mexico, South Africa, and

Venezuela based on the number of nascent

entrepreneurs who continued on to operate

sustainable enterprises 1.

• Entrepreneurship is one of the core pillars of developed

economies, particularly due to the fact that it enables

positive contribution to economic growth and is essential

in driving community sustainable livelihood.

• Studies have pointed to the fact that the establishment of

new and small business is an engine for job creation and

not necessarily the mega-corporations. Comparatively,

countries with greater entrepreneurship impetus

experience significant reduction in unemployment rates

5. Therefore, it is important that Jamaica take the

corrective actions to nurture this great potential to

creating culture of entrepreneurs.

• When one considering the Jamaican scenario, it

becomes more crucial to focus on the development of a

culture where young people are enthusiastic about

creating wealth and their own employment. It is evident

that young people are faced with several challenges.

The rate of unemployment for young persons is three

times higher than that of adults 6. Skill levels among

youth entering the labour force are significantly low over

70%, 7. Additionally, the youth cohort dominates those

most affected by poverty 8.

•

•

Create trust fund and finance programs for young

entrepreneurs

One of the greatest challenges for young people in

their quest to start a business is the deprived access to

start-up funds. That is one of the primary reasons

saving is a positive behavior which should be

vigorously promoted. However, if Jamaican youth are

to excel in the field of entrepreneurship, access to

start-up capital is a fundamental prerequisite. With the

risks and high failure rate in business, it is being

proposed that special funds be put in place that reduce

the requirement to access loans and also provide

grants for solid business ideas.

Simple Business Ethics and Research

•

•

•

Decide if you really want to be in business:

You will be putting some (not all, hopefully) of your net worth

at risk. You will run

the risk of becoming eccentric, meaning creating a life that is out of balance, with

working hours taking

away from other family or pleasurable activities. There may be levels of stress you

have not experienced as an employee.

•

•

Decide what business and where:

Once you have decided you have the characteristics of a successful entrepreneur

and that you definitely want to be in business, then you must decide which business

is best for you and where to locate that business.

•

•

Decide whether to start full-time or moonlight:

There are some interesting advantages and some pitfalls in starting as a moonlight

business. (That is, a business you start in your off hours while still working at your

current job.) More often than not, the advantages of starting as a moonlighter

outweigh the risks:

You avoid burning your bridges of earnings, including retirement, health and fringe

benefits and vacations.

Your full-time job won't suffer if you maintain certain conflict of interest disciplines,

including

•

•

• compartmentalizing your job and business into completely separate

worlds.

• You can avoid conflict of interest with your job by choosing a

business that is appropriate for moonlighting, such as: single

products, real estate, specialized food, e-commerce, direct

marketing or family-run operations.

• There are great advantages for operating a family business. The

family can run the business while you are at work. You have a builtin organizational structure. You can teach your kids the benefits of

being in business.

• But there are also some pitfalls to consider in starting a moonlight

business:

• There is a temptation to spend time at your job working on your

moonlight business. That is unfair to your employer and should not

be done under any circumstances. (You may need a family member

or some trusted person to cover emergencies when you are at your

job.)

• Another problem may be competing with your employer, which,

again, is not right. Think of how you would feel or handle this

employee if you were the boss.

• Any kind of conflict with your regular work can jeopardize your job

and your moonlight business.

• Overwork and mental and physical exhaustion can also become a

very real problem for moonlight entrepreneurs.

Selection Strategy

•

•

•

•

•

•

•

•

Selecting the wrong business is the most frequent mistake that start-up

entrepreneurs make. Here is a checklist to help you select a successful one:

Take your time and wait for the business that is just right for you. You will

not be penalized for missing opportunities. The selection process takes a lot

of planning and your experience and complete knowledge is vital for your

success.

Don't tackle businesses that may be too challenging. It is better to identify a

one-foot hurdle than try to jump a seven-footer.

Try to identify a business that has long-term economic potential. Follow

Wayne Gretzky's advice, "Go to where the puck is going, not to where it is."

A big mistake can be an error of omission. This means you may fail to see

an opportunity that is right in front of you.

Look for a business that will grow in today's and tomorrow's markets. Many

small retail stores are no longer in business because huge stores provide

more choices to the customer and often at a cheaper price.

Businesses to avoid are "commodity" businesses where you must compete

entirely on price and in which you must have the lowest cost to survive. As

Mr. Buffett has said, "In a commodity type business you're only as smart as

your dumbest competitor."

Most service businesses have pricing power.

• If you intend to manufacture a product, consider the pros and cons

of contracting out production to a low-cost supplier. In other words,

operate a "hollow corporation." A "hollow corporation" is a company

that subcontracts manufacturing and packaging.

• Things to Watch Out For:

• Impatience

• Do not let overconfidence short-circuit you from analyzing your

selection of businesses carefully. You must not fear of hearing the

negative aspects; it is much better to be aware of them and face

them early on.

• Be realistic. Do not become lured by high rewards. They will come if

you choose the right business and if you understand every aspect of

the business before you open its doors.

• Required Activities

• It is worth repeating again: The most common mistake and the most

costly one is not picking the right business to begin with. This is the

time for soul searching.

• How to Evaluate a Specific Business you have in mind.

• Here are some questions to help clarify your thoughts:

• Is it something I will enjoy doing?

My favorite activities are:

__________________________

I like to serve people by:

________________________________

• Will it serve an expanding need for which there is no

close substitute?

• Can I be so good at a specialized, targeted need that

customers will think there is no close substitute?

• Can I handle the capital requirements?

• Can I learn the business by working for someone else

first?

• Could I operate as a hollow corporation, without a factory

and with a minimum number of employees? ("Hollow

corporation" refers to a business where everything is

"outsourced," meaning you would subcontract

manufacturing and packaging to outside sources. )

• Is this a product or service that I can test first?

• Should I consider a partner who has complementary skills to mine or

who could help finance the business?

• Before you start, get completely qualified:

• The best way to become qualified is to go to work for someone in

the same business.

• Attend all classes you can on the subjects you need, for example:

accounting, computer and selling.

• Read all the appropriate "how-to" books you can.

• Don't be afraid to ask questions or seek help from the most

successful people in your intended business.

•

•

•

•

•

FOUR AREAS OF INTEREST IN STARTING A BUSINESS

Research

Investment/startup

Marketing

Savings/expansion

Research ideas when Starting a business

•

•

•

•

•

•

What service or product does my business provide and what needs does it

fill?

Who are the potential customers for my product or service and why will they

purchase it from me?

How will I reach my potential customers?

Where will I get the financial resources to start my business?

Self-Confidence

Entrepreneurs are self-confident when they are in control of what they're

doing and working alone. They tackle problems immediately with confidence

and are persistent in their pursuit of their objectives. Most are at their best in

the face of adversity, since they thrive on their own self-confidence.

Sense of Urgency

Entrepreneurs have a never-ending sense of urgency to develop their ideas.

Inactivity makes them impatient, tense, and uneasy. They thrive on activity

and are not likely to be found sitting on a bank fishing unless the fish are

biting. When they are in the entrepreneurial mode, they are more likely to be

found getting things done instead of fishing.

•

•

•

•

Comprehensive Awareness

Successful entrepreneurs can comprehend complex situations that may include

planning, making strategic decisions, and working on multiple business ideas

simultaneously. They are farsighted and aware of important details, and they will

continuously review all possibilities to achieve their business objectives. At the same

time, they devote their energy to completing the tasks immediately before them.

Status Requirements

Entrepreneurs find satisfaction in symbols of success that are external to themselves.

They like the business they have built to be praised, but they are often embarrassed

by praise directed at them personally. Their egos do not prevent them from seeking

facts, data, and guidance. When they need help, they will not hesitate to admit it

especially in areas that are outside of their expertise. During tough business periods,

entrepreneurs will concentrate their resources and energies on essential business

operations. They want to be where the action is and will not stay in the office for

extended periods of time.

Symbols of achievement such as position have little relevance to them. Successful

entrepreneurs find their satisfaction of status needs in the performance of their

business, not in the appearance they present to their peers and to the public. They

will postpone acquiring status items like a luxury car until they are certain that their

business is stable.

Interpersonal Relationships

Entrepreneurs are more concerned with people's accomplishments than with their

feelings. They generally avoid becoming personally involved and will not hesitate to

sever relationships that could hinder the progress of their business. During the

business-building period, when resources are scarce, they seldom devote time to

dealing with satisfying people's feelings beyond what is essential to achieving their

goals.

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

General Start-Up Activities

Determine the business you want to start and determine:

Your qualifications for the business.

The feasibility of making that business profitable.

Conduct research on your industry, target market and

competition.

Select a location and analyze it for traffic, parking, and customer

and delivery access.

Investigate all start-up procedures specific to your industry.

There is a lot to think about when you are starting your own business.

The following checklist will help guide you on:

Checklist for Business Start-Up

1

www.paopen4business.state.pa.us

Write a business plan that includes your strategies for

management, marketing, production and financial contingencies.

Develop a list of all potential monthly expenses.

Determine potential sources of financing for your type of

business.

Develop a list of all equipment and purchases required to

start your business. Identify the costs of each.

Research potential suppliers and investigate credit terms

with each.

Develop descriptions of all duties within your firm and

determine the person responsible for each. Identify future

educational needs.

Business Start-Up

•

Costs

Business start-up costs are the expenses you incur before

you

actually begin business operations. Your business start-up

costs

will depend on the type of business you are starting. They

may

include advertising, travel, surveys, and training. These

costs

are capital expenses, which are expenses you deduct over

a

number of years. However, if you never begin business

operations,

you cannot deduct start-up costs.

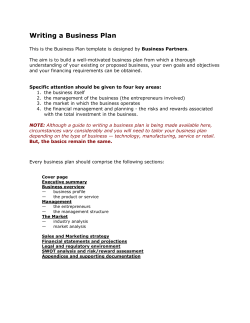

A business plan is a tool with three essential purposes:

planning, communication and management. Use the

advice here to create or update your business plan.

Gather additional advice from fellow entrepreneurs and

experienced business owners on our business Forums.

Planning. The business plan guides you through the

various phases of your business. Preparing a business

plan requires that you look realistically at almost every

phase of business because you must show that you have

worked out all the problems and decided on potential

alternatives before actually launching your business. A

thoughtful plan will help identify roadblocks and obstacles

to avoid and help you to establish alternatives.

• Communication. As a tool for communication, the

business plan is used to attract investment capital,

secure loans, convince workers to hire on and assist in

attracting strategic business partners. A comprehensive,

clearly-written business plan shows whether or not a

business has the potential to make a profit. Many

business owners share their business plans with their

employees to foster a broader understanding of where

the business is going.

• Management. As a management tool, the business plan

helps you track, monitor and evaluate your progress. It is

a living document that you will modify as you gain

knowledge and experience. By using your business plan

to establish timelines and milestones, you can gauge

your progress and compare your projections to actual

accomplishments.

• A business must have a business plan.

If there is no plan, then there is no

business.".

• The importance of a comprehensive,

thoughtful business plan cannot be

overemphasized. Much hinges on it:

outside funding, credit from suppliers,

effective management of your operation

and finances, promotion and marketing of

your business, and achievement of your

goals and objectives.

• to persuade someone to buy them. When you write your

business plan, consider yourself a salesperson. The

product you're trying to sell is your business idea. Your

customers are potential investors and employees. Since

you want your customers to believe in you, you must be

able to convince them that you know what you are

talking about when it comes to your business.

• Before you begin writing your business plan, consider

four core questions:

• What service or product does my business provide and

what needs does it fill?

• Who are the potential customers for my product or

service and why will they purchase it from me?

• How will I reach my potential customers?

• Where will I get the financial resources to start my

business?

• In order to answer these questions, you must become an

expert about your own business (or to fine-tune your

knowledge if you already believe you are one). You must

be willing to roll up your sleeves and begin digging

through information. Since not all information that you

gather will be relevant to the development of your

business plan, it will help you to know what you are

looking for before you get started.

• What part does you business plan play?

• The business plan often is called the blueprint for

success. Without a good business plan, you will find it

nearly impossible to obtain capital. The business plan

starkly exposes your business knowledge (or lack of it)

to lenders or investors. Preparing a business plan forces

you to think through your ideas and helps you

communicate

• them clearly. Not only does this help you obtain financing, it is vital

for successfully establishing your goals and managing your

business and employees.

Much of the information requested in other portions of this booklet is

necessary for completing the business plan. The business plan ties

together this and much more information into a document explaining

most things an investor or lender would want to know about your

business.

Preparing a business plan isn't easy. It takes time and money to

collect the necessary information, to analyze that information, and to

properly communicate your findings. This cannot be done

overnight. Successful entrepreneurs usually spend six to 10 months

researching and preparing their ventures. Ninety percent of them

utilize professional advisers, such as lawyers or accountants, while

almost 70 percent attend business seminars and regularly read

business material.

• Business Plan Outline

•

Executive summary (to be completed last)

– A broad overview of your company's activities, management and

objectives

– Distinguishing features of your products/services

– Attractiveness of your market

– Summary of historical financial results and financial projections

– Amount of money you seek, in what form and for what specific

purposes

Description of your business and industry

– Your business

– The industry, its history and its anticipated future

Features and advantages of your products/services

– Description

– Competitive advantage and market niche

•

•

– Proprietary position

– Future potential

You should consider including some products or sales literature as exhibits.

Market research and analysis

– Existing and potential customers and markets

– Critical customers (over 10% of sales)

– Market size and trends

– Competition and strategy for competing

Estimated market share and sales

– Marketing plan

– Marketing strategy

– Pricing

– Sales tactics

– Service and warranty policies

– Advertising, public relations and promotion

Product design and development plans

– Development status and tasks

– Difficulties and risks

– Costs

•

•

Operations plans

– Production or service delivery process (flow charts may be helpful)

– Geographic location

– Existing facilities and projected improvements for future needs

– Strategy and plans

– Labor force

– Product/service distribution

– Availability of material and supplies

– Dependence on critical suppliers

– Unique or novel processes used

Management team

– Organization and ownership (charts are helpful)

– Key management personnel (credentials)

– Management strengths and weaknesses

– Management compensation

– Board of directors

– Key business advisers

– Professionals retained (accountant and attorney)

Include personal financial statements of principal owners as exhibits.

•

Overall schedule

– Timing of critical activities before opening (obtaining funds, incorporating

the company, selecting the location, ordering supplies, hiring employees,

starting operations)

– Timing of critical activities after opening (expansion, product/service

extension)

Response to critical risks and problems

– Working capital shortage

– Price cutting by competitors

– Unfavorable industry-wide trends

– Design/operating costs over estimates

– Low sales

– Difficulty obtaining supplies, raw materials

– Difficulty obtaining credit

– High inflation

– Lack of trained labor

– Recession

Financial statements and projections

– Five years of annual historical financial statements (or from the period the

business has been in operation, whichever is shorter)

– Profit and loss forecasts for each month of the first full year and for each

of the first three years of operation

• Cash flow projections and an operating budget for each month of the

first full year and for each of the first three years of operation

– Pro forma balance sheet at start-up, monthly balance sheets for

the first year and at the end of each of the first three years

– Financial controls to be implemented

– Person responsible for finance and accounting matters

– Outside accountant or bookkeeper who will audit, review or

compile the company's financial statements

• Ownership structure

– Owners and how much they are investing

– Shareholder agreements

– Which owners are making personal guarantees

Proposed company financing sought

– Desired amount and terms of financing and form (equity, grant or

loan)

– Timing of required financing

– Proposed use of funds, scheduling

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

Simpler Outline

Executive Summary - summarizing key

points of the plan in one or two pages.

Overview - introducing the reader to your

company and the industry.

Description of products and services.

Analysis of the market in which your

business will compete.

Marketing strategy - summarizing the

product, promotion, pricing, and distribution

strategies of the business.

Operations plan.

Description of the experience, training,

and talent of your staff.

Schedule of activities outlining your

timeline.

Analysis of critical risks and problems.

Financial plan - including pro-forma

balance sheets, income statements and cash

flow statements. A balance sheet compares

what your business owns (assets) to what it

owes. A cash flow statement compares how

much money will be coming in to how much

you will be spending. An income statement

compares your revenues to your expenses to

see if you are going to make money.

•

•

•

Once you have worked through your business plan and have a good

product, you should work on your personal presentation. Remember, your

ability to effectively manage is being judged, as is your business plan

itself. Preparing key visual aids, developing responses for likely questions

and repeated practice are good strategies.

What are some sources of investment capital?

Many people interested in starting a business immediately look to

commercial banks for financing. This is understandable because of the

important financial role banks play in our society. However, banks are only

one source of possible financing; often a business combines several

sources. The following list of potential financing sources is presented for

your consideration.

Yourself

In addition to contributing your own sweat equity, you have to be willing to

put up a good share of the money. No lender will give you money if you are

not at personal financial risk. You may be asked to personally guarantee

repayment of any loans made to your business. As well as indicating your

commitment to the business, personal investment is one of your easiest

sells. If you can't convince yourself to invest, who can you convince?

Savings, mortgages, personal possessions and life insurance policies are

just a few sources of money that can get you started.

Relatives and friends

Again, these are people you should have a good chance of

• convincing to loan you money. They know

you better than any potential outside

lender. However, be careful. Make sure

your relatives and friends know the risk

involved and formalize the lending

arrangement with a promissory note or

loan agreement. Many personal

relationships have been ruined by small

business failure.

• Government-sponsored financing programs

State and local governments offer financing options for

your company, as well. Many have subsidized loan

pools that provide fixed-rate, below-market business

loans or grant programs. JBDC.

• Small business investment companies are private

companies that offer financing JNBS. Licensed by the

Small Business Administration, they provide debt and

equity capital to many small businesses. They will

undertake more risks but also demand greater rewards

through either higher interest rates or equity positions.

Commercial banks

Banks operate on a small margin of error and are

extremely wary of investing in a risky

business. Collateral to more than fully secure the loan including personal guarantees - is necessary to convince

a bank to lend you money.

THE END

© Copyright 2026