Document 109443

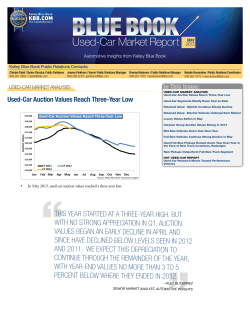

In This Issue: BLUE BOOK www.kbb.com Market Report NEW-CAR MARKET ANALYSIS Analysts Determine Improved Economic Indicator Levels Needed to Bolster Vehicle Sales Back to 15M With Gas Prices Sliding, Mid-Size Sedan Sales Surge at the Expense of Compacts; More USED-CAR MARKET ANALYSIS Drop in Gas Prices Drive Weakest Q2 Performance of Wholesale Values Since 2008; More JULY 2012 RESIDUAL ANALYSIS Reconsidering Fuel Prices Analysis from Kelley Blue Book’s Analytic Insights Team LATEST HOT USED-CAR REPORT Large Utility Models Make Up Top Five For June Kelley Blue Book Public Relations Contacts: Robyn Eagles | Senior Director, Public Relations 949.268.3049 | [email protected] Joanna Pinkham | Senior Public Relations Manager 949.268.3079 | [email protected] Brenna Robinson | Public Relations Manager 949.267.4781 | [email protected] Natalie Kumaratne | Public Relations Coordinator 949.267.4770 | [email protected] NEW-CAR MARKET ANALYSIS: Analysts Determine Improved Economic Indicator Levels Needed to Bolster Vehicle Sales Back to 15M - Alec Gutierrez, senior market analyst, automotive insights, Kelley Blue Book N ew-vehicle sales hit 14.1 million seasonally adjusted annual rate (SAAR) in June 2012, a 22 percent increase year-over-year. Through the first six months of the year, more than 7.2 million light vehicles were sold, keeping sales on pace to hit Kelley Blue Book’s projected forecast of 14.2 million units for the year. This would mark the first time sales surpassed 14 million units since 2007, and the third consecutive year of 10 percent or greater annual gains since sales hit a near 30-year low of 10.5 million units in 2009. The sales rebound predominately has been driven by a steady, albeit painfully slow, economic recovery since the real estate bubble burst in 2008. Strong demand from consumers in need of a replacement vehicle, improved credit availability, low interest rates and ample incentives are further aiding sales. Sales have remained strong despite a flurry of negative economic developments during the past few months, including a soft job market and four consecutive months of decline in consumer confidence. Although conditions in the economy have showed signs of weakness, Kelley Blue Book still believes that the economy is strong enough to keep sales steady through the remainder of 2012. Although industry sales are on pace to improve 11 percent in 2012, we may see industry growth stall in 2013. In order for sales to return to 15 million units per year, we will need stronger economic growth, specifically in both unemployment and consumer confidence. Unfortunately for those banking on an expedient recovery in auto sales, recent data suggests that it may be some time before the economy is healthy enough to support a return to 15 million annual sales. With both unemployment and consumer confidence headed in the wrong direction, Kelley Blue Book analysts examined the historical relationship between unemployment, consumer confidence and light-vehicle sales to determine how much overall economic improvement is necessary before sales once again approach 15 million units per year. Since 1976, light-vehicle sales have not surpassed 13 million units in a year where the unemployment rate averaged 8 percent or more. According to trend, unemployment will need to reach 6 percent or less before light-vehicle sales can sustainably achieve 15 million units per year or more. Similarly, consumer confidence needs to be at 80 or above before 15 million units a year becomes a reality. With the unemployment rate currently at 8.3 percent and consumer confidence at 62, we have a long way to go before the industry reaches a point where sales will return to their pre-2008 norm. 2011 10 11 12 13 Vehicle Sales vs. Confidence Consumer Confidence Index Avg. Unemployment Rate % Vehicle Sales vs. Unemployment 11 10 9 8 7 6 5 4 3 2 2012 (est.) 14 Annual Light-Vehicle Sales (Millions) 15 16 17 18 Source: economy.com 160 140 120 100 80 60 40 20 0 2012 (est.) 2011 10 11 12 13 14 Annual Light-Vehicle Sales (Millions) 15 16 17 18 Source: economy.com NEW-CAR MARKET ANALYSIS: continued With Gas Prices Sliding, Mid-Size Sedan Sales Surge at the Expense of Compacts G 250,000 200,000 150,000 100,000 50,000 Compact Car Mid-Size Car Jun-12 May-12 Apr-12 Mar-12 Jan-12 Feb-12 Dec-11 Oct-11 Nov-11 Sep-11 Jul-11 Aug-11 Jun-11 Apr-11 May-11 Mar-11 Jan-11 0 Feb-11 While compact sales have been unable to keep pace with the rest of the industry, mid-size sedan sales continue to flourish. Mid-size cars accounted for 18.6 percent market share in June, a 44 percent increase year-over-year. The surge in mid-size car sales can largely be attributed to the strength of the redesigned Toyota Camry, which posted more than 32,000 sales alone in June. The Chevrolet Malibu, Honda Accord, Nissan Altima and Ford Fusion also performed well, each selling more than 20,000 units due to strong incentives in anticipation of redesigns that are expected to arrive for each model later this year. The Altima, Malibu and Fusion currently are available with nearly $3,000 each in cash rebates and close to zero-percent financing for up to 60 months. In many cases, these deals are swaying consumers who otherwise would have considered purchasing a compact. Mid-Size Sedan Sales Surge While Compacts Stall 300,000 Monthly Light-Vehicle Sales as prices have dropped more than $0.50 per gallon nationally since April, and sales of compact cars have slowed significantly as a result. Compared to last year, sales were relatively flat, increasing a scant 1.4 percent, which is well below the 22 percent average increase for the industry. Fuel prices are expected to drop as low as $3.00 per gallon by year-end according to some estimates; a mark that will send compact cars sales tumbling further. Source: Kelley Blue Book Automotive Insights Alternative Energy Vehicle Sales Surge 164 Percent in June W 35,000 $4.40 30,000 $4.20 25,000 $4.00 20,000 $3.80 15,000 $3.60 10,000 $3.40 5,000 $3.20 $3.00 Jun-12 May-12 Apr-12 Mar-12 Feb-12 Gas Prices Jan-12 Dec-11 Oct-11 Nov-11 Sep-11 Jul-11 Aug-11 Jun-11 Apr-11 Mar-11 0 May-11 Alternative Energy Vehicle Sales Source: Kelley Blue Book Automotive Insights and Energy Information Administration (EIA.gov) Sales of alternative-energy vehicles typically fall rapidly after fuel prices peak, and although sales are down from the March 2012 high, they remain stronger than in previous years. - Alec Gutierrez 2 BLUE BOOK Market Report JULY 2012 National Average Fuel Price/Gallon $4.60 Jan-11 Sales of the Lexus CT200h also improved nearly 500 percent year-over-year. In addition, the Chevrolet Volt was a strong performer with sales improving more than 200 percent year-overyear. The Volt has outsold the Nissan Leaf nearly 3-to-1 so far this year, even though it has a higher manufacturer’s suggested retail price (MSRP) and is not considered a “true” all-electric from a purists’ standpoint. Meanwhile, the Honda CR-Z, Honda insight and Nissan Leaf all fell short of figures from just a year ago. Sales of alternative-energy vehicles typically fall rapidly after fuel prices peak, and although sales are down from the March 2012 high, they remain stronger than in previous years. 40,000 Feb-11 The Toyota Prius was the most significant driver of segment gains, with sales surging more than 300 percent from June of last year. The Prius has been in high demand since the introduction of the subcompact Prius c and wagon-esque Prius v. Sales numbers for the Prius also look especially strong due to the inventory shortages that plagued Toyota at this time last year. Hybrid Sales Fluctuate Along with Fuel Prices Monthly Light-Vehicle Sales ith gas prices declining, sales of hybrid and electric vehicles have remained surprisingly resilient. In fact, sales of dedicated hybrid and alternative-energy vehicles surged more than 164 percent in June. We could see hybrid and electric vehicle sales slow as well; however, today it appears as though the sales decline may be relatively mild. USED-CAR MARKET ANALYSIS: U sed-car values dropped more than 2 percent in June, the second consecutive monthly decline since values leveled off in early April. Through Q2, values slid more than 4 percent, the most pronounced quarterly decline since 2008. The market was especially soft this year due to an earlier-than-anticipated jump in fuel prices, which sent values of fuel-efficient compact and hybrid cars tumbling. Fuel prices topped out in early April, well before the typical seasonal decline that begins after Memorial Day weekend. Since vehicle values peaked early as well, now they have slipped below average prices seen in 2011. The average 1- to 3-year-old vehicle now averages $18,000 at auction, approximately 4 percent below the amount dealers were paying one year ago when used-car values hit an all-time high. Although values are now down from the height of last year, they remain 20 percent higher than the low point in 2009 and more than 10 percent above the average price paid from 2000 to 2008. With values still high from a historical perspective, Kelley Blue Book believes there is room for further softening through the second half of 2012. Change in Auction Value (MY20092011) Drop in Gas Prices Drives Weakest Q2 Performance of Wholesale Values Since 2008 Falling Gas Prices Lead to Weak Q2 4.00% 2.80% 2.00% 0.40% 0.00% -0.30% -2.00% -4.00% -4.30% -6.00% Q2 2009 Q2 2010 Q2 2011 Q2 2012 Source: Kelley Blue Book Automotive Insights Used-Car Values Projected to Drop 3.5 Percent in Q3 L ooking ahead, Kelley Blue Book expects used-car values to continue to decline moderately, especially as supply improves at auction. As it stands today, supply has improved slightly but still remains tight. Trade-in volume has increased alongside new-vehicle sales, which is alleviating inventory shortages plaguing dealers. In most cases though, dealers are opting to retain trade-ins, keeping trade volume low in the auction lanes. Off-lease volume is expected to remain tight until at least the first quarter of 2013, but even then, auctions may not see an increase in volume. In many cases, captive finance companies are selling their off-lease vehicles directly to franchised dealers, benefitting only those franchised dealers with access to upstream sales channels. With auction supply expected to remain tight through the third quarter of 2012, Kelley Blue Book projects values to drop 3 to 4 percent on average. This decline will be less pronounced than the 5.6 percent decline that occurred during the third quarter of 2011, since values started their decline earlier this year. Although values currently are down more than 4 percent year-over-year, we expect this gap to narrow as the pace of depreciation levels off in the months ahead. Change in Auction Value (MY2009-2011) Q3 Declines in Used-Car Values 2.00% 0.70% 0.00% -2.00% -1.30% -4.00% -3.50% -6.00% -5.60% -8.00% Q3 2009 Q3 2010 Q3 2011 Q3 2012 (projected) Source: Kelley Blue Book Automotive Insights 3 BLUE BOOK Market Report JULY 2012 With auction supply expected to remain tight through the third quarter of 2012, Kelley Blue Book projects values to drop 3 to 4 percent on average. - Alec Gutierrez USED-CAR MARKET ANALYSIS: continued Crossovers Underperform, Yet Values Retention Remains above Average D espite the fact that crossovers (CUVs) had the greatest percentage decreases in the second quarter, they continue to outperform the average vehicle in terms of retained value. Using model-year 2010 as an example, the average auction value for all vehicles is approximately 65 percent of the original MSRP, compared to 73 percent for the luxury crossover segment, and 66 percent for mid-size and compact crossovers. Declines in CUV values during the last three months are more of a return to normalcy than an identifier of poorly performing segments, as strong values for CUVs are unsustainable in a market with downward pressure on newvehicle prices and increasing affordability and credit. Another contributing factor to the drop in crossover values is the April peak in gas prices and subsequent decline through May and June. The popularity of crossovers largely is due to the periods of high gas prices driving many consumers away from inefficient SUVs. While crossovers continue to offer a good compromise between mileage and carrying capacity, their advantages are not as pronounced during periods of falling fuel prices, especially considering American consumers’ infatuation with sport utility vehicles. Declines in CUV values during the last three months are more of a return to normalcy than an identifier of poorly performing segments, as strong values for CUVs are unsustainable in a market with downward pressure on newvehicle prices and increasing affordability and credit. - Alec Gutierrez Crossovers Lead Q2 Declines Mid-Size Crossover Luxury Crossover Compact Crossover Mid-Size Sport Utility Mid-Size Car Luxury Sport Utility Minivan Full-Size Sport Utility Full-Size Car Full-Size Pickup Truck Average Full-Size Crossover Compact Car Luxury Car Mid-Size Pickup Truck Hybrid Car Compact Luxury Car Premium Luxury Car Sports Car Near Luxury Car Subcompact Car -7.2% -6.7% -6.0% -5.4% -5.3% -5.1% -5.0% -5.0% -4.6% -4.5% -4.3% -4.3% -3.1% -2.7% -2.6% -2.4% -1.7% -1.4% -1.2% -0.9% -0.8% Mid-Size Pickup Truck Hybrid Car Subcompact Car Luxury Sport Utility Near Luxury Car Compact Crossover Full-Size Pickup Truck Compact Car Mid-Size Crossover Average Full-Size Crossover Luxury Car Mid-Size Sport Utility Compact Luxury Car Minivan Full-Size Sport Utility Mid-Size Car Premium Luxury Car Van -20.0% -10.0% 0.0% 10.0% Change in Auction Value (MY2009-2011) Source: Kelley Blue Book Automotive Insights 4 BLUE BOOK Market Report JULY 2012 75.3% 72.7% 72.3% 71.6% 70.2% 69.4% 67.6% 66.3% 66.1% 66.0% 65.6% 64.7% 63.5% 63.5% 63.0% 62.5% 61.2% 59.7% 58.8% 58.7% 56.3% 55.9% Sports Car Luxury Crossover 0.3% Van Crossover Retention Remains High Full-Size Car 0.0% 20.0% 40.0% 60.0% 80.0% Auction Value/MSRP(MY2010) Source: Kelley Blue Book Automotive Insights USED-CAR MARKET ANALYSIS: continued Used Fuel Sippers Slide on Cheaper Gas C heaper prices at the pump continued the trend of weaker demand for fuel-efficient vehicles, which saw a drop of 2.5 percent in auction values since the start of June, more than the overall average of 1.9 percent depreciation for the market. As dealers remain wary of purchasing these vehicles at auction, Kelley Blue Book expects values to continue falling in line with fuel prices. The most significant declines will come from hybrid cars, which remain up 10 percent on a year-to-date basis. The 2010 Toyota Prius, which we noted was due for a price correction last month, continued its swift decline of more than $1,000 in June. Although Kelley Blue Book expects continued weakening, we should note that fuel-efficient vehicles remain among the top performers when it comes to value retention from original MSRP. The average 2010 model-year used compact car is worth 66 percent of its original MSRP, slightly better than the aforementioned 65 percent average for the industry. Subcompact and hybrid cars remain especially strong, currently holding 70 and 72 percent of original MSRP, respectively. Consumers that own a fuel-efficient vehicle should not be concerned with excessive depreciation. Today we merely are seeing a correction from the run-up in values that occurred while fuel prices increased early in the year. These vehicles are highly sensitive to fluctuations in fuel prices and as a result, there is a strong increase in values while fuel prices rise, only to be followed by a correction once fuel prices retreat. KBB Used-Car Valuation Index (1- to 3-Year-Old Vehicles) Consumers that own a fuelefficient vehicle should not be concerned with excessive depreciation. Today we merely are seeing a correction from the run-up in values that occurred while fuel prices increased early in the year. 125 Fuel-Efficient Segments (CY2011) Fuel-Efficient Segments (CY2012) 120 Market Average (CY2011) Market Average (CY2012) 115 110 CY 2011 105 100 95 CY 2012 90 Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Source: KBB Automotive Insights - Alec Gutierrez RESIDUAL ANALYSIS: Reconsidering Fuel Prices - Eric Ibara, director of residual value consulting, Kelley Blue Book A 5 BLUE BOOK Market Report JULY 2012 $12.00 $3.50 $10.00 $3.00 $2.50 $8.00 $2.00 $6.00 $1.50 $4.00 $1.00 $2.00 $0.50 Jan-17 Sep-17 May-16 Jan-15 Sep-15 May-14 Jan-13 U.S. All Grades Retail Gasoline Prices, ($ per Gallon) Sep-13 May-12 Jan-11 Sep-11 May-10 Jan-09 Sep-09 $- May-08 Jan-07 Sep-07 May-06 Jan-05 Sep-05 May-04 Source: Economy.com $- Natural Gas: ($ per MMBtu) Natural Gas price in Dollars per MMBtu $4.00 Jan-03 The technology that enabled this increase is called hydraulic fracturing, a technique that allows previously inaccessible oil and gas to be removed from the ground. This has resulted in a separation between gasoline prices, which have risen since 2008, and natural gas prices, which have dropped. $14.00 Sep-03 The commonly held notion that gas prices will inevitably rise, could likewise benefit from an occasional reality check. For starters, oil production in the U.S. is rising. In the first quarter of 2012, according to the Wall Street Journal, oil production in the U.S. averaged more than six million barrels a day, a level not seen since 1998. This has been a contributing factor to the recent drop in crude oil below $80 a barrel. Gas and Natural Gas Prices Diverge $4.50 Motor Gasoline Prices in Dollars per Gallon few decades ago, the scientific consensus held that dinosaurs became extinct when they failed to adapt to a changing world. In fact, it was common practice to refer to a person who refused to change as a “dinosaur.” Subsequently, more nuanced studies considered the layer of iridium-rich soil above which no dinosaur fossils have ever been found. Iridium, a metal not commonly found on Earth, is a footprint of meteorites, which led scientists to reconsider their hypothesis. RESIDUAL ANALYSIS: continued Another development currently underway is the increasing fuel efficiency delivered by new vehicles sold. This trend will continue as CAFE standards call for the average fuel economy across all vehicles sold by a manufacturer rising to an average of 34.1 miles per gallon by 2016. This represents an improvement of approximately 33 percent over the average of all vehicles sold in 2008. More fuel efficient vehicles require less gasoline for the same miles travelled, so demand will be lower for this second reason. So what does this mean for the automotive sector? For starters, if normal trends hold and no extraordinary event occurs, it is likely that gas prices have already peaked for the year. Gas prices at the pump have historically been lower when oil prices have been at their current level of around $80 per barrel. Prices of around $3 a gallon could be possible later this year. Judging by the events of 2008, this will likely be bad news for the fuel-efficient vehicles. From the peak of gas prices at the end of June 2008, to the bottom of the decline in prices in January 2009, compact and subcompact sedans lost an average of about 20% of their values. Hybrids lost even more, an average of 34 percent, or more than $8,000 per vehicle. Of course, this year’s run up in vehicle prices and subsequent decline is not nearly as volatile as it was in 2008. Still, softness in these segments is expected to accompany lower gas prices. While the rise in fuel price makes 2012 appear to be similar to 2008, there is one significant difference. In 2008, as gas prices plunged, fuel efficient vehicles dropped in value while large utility vehicles and trucks gained. In 2012, large vehicle values did not decline as gas prices climbed. This is because of a shortage of used vehicles across almost all segments. Therefore, a drop in gas prices this year is not expected to cause a further rise in prices among trucks and utility vehicles. For new car sales, consumers have preferred larger vehicles as long as gas prices are affordable. In 2008, gas prices rose during the first half of the year and then plummeted throughout the second half. That year, retail sales for fuel efficient vehicles (compact cars, subcompact cars, and hybrids) dropped by 29 percent from the first half to the second. Consequently, a decline in retail sales in these segments is expected for the second half of this year, but won’t be as severe as the 29% drop in 2008. Average and Projected CAFE 35.0 Combined City and Highway MPG A consequence of this gap is a shift towards more CNG-powered (compressed natural gas) vehicles. This is already evident in many municipal vehicles, such as city buses and waste collector trucks. Earlier this year, all three domestic manufacturers announced CNG versions of their full-size trucks, offering truck buyers an option that consumes less expensive fuel. This trend will likely continue and reduce the demand for gasoline. 34.1 32.6 31.3 29.7 30.0 30.5 27.3 25.0 24.7 24.7 24.7 24.7 24.7 24.8 25.1 25.3 25.5 25.7 25.9 20.0 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 Low gas prices will likely create an inventory imbalance as CAFE requirements for 2016 start to take hold. Manufacturers could be locked into producing vehicles that consumers don’t want but need to be sold in order to achieve CAFE targets. Conversely, fuel-inefficient vehicles would be produced in controlled numbers and their shortage could result in artificially high prices. In either event, without the proper incentives (monetary and non-monetary), consumers could be left unsatisfied if they have to settle for a vehicle that may not be their first choice. A further consequence of this market imbalance could be a hit to manufacturers’ bottom lines if they are forced to incentivize fuel-efficient models and are restricted in selling more high-profit, fuel-inefficient models. Over a long period of time, this could impact manufacturer’s research and design budgets. From a residual value perspective, if these trends materialize, they will likely present a few challenges to manufacturers. As the demand for a model wanes, manufacturers need to resist the temptation to direct excess volume to daily rental service. Balancing production with demand will be critical, along with a miserly application of incentives only when needed. For anyone holding a portfolio of vehicles, running an analysis of the residual risk at lower gas prices would be instructive. As stated above, there is little upside gain from larger vehicles this year to offset lower values for fuel-efficient vehicles. From the oil spike in 2008, many in the auto and financing industries are aware of the risks associated with rising fuel prices. At Kelley Blue Book, we believe higher gas prices five years from now is only one of several scenarios against which vigilance is required. Developments in the oil and gas industry, along with the CAFE requirements for 2016, will conspire to keep a lid on fuel prices. However, those same CAFE regulations and the current used-car inventory levels could create risk factors that did not exist in 2008 should fuel prices continue to drop. Considering what’s at stake, it seems prudent to have a plan that considers such a scenario. This commentary focuses on model years 2009-2011. The statements set forth in this publication are the opinions of the authors and are subject to change without notice. This publication has been prepared for informational purposes only. Kelley Blue Book assumes no responsibility for errors or omissions. 6 BLUE BOOK Market Report JULY 2012 HOT USED-CAR REPORT: Large Utility Models Make Up Top Five for June - Arthur Henry, manager of market intelligence and market analyst, Kelley Blue Book Kelley Blue Book’s Hot Used-Car Report captures monthly used-car shopper activity on kbb.com, including a list of the top and bottom movers in the same time period. Results are provided by the Kelley Blue Book Market Intelligence Team, in an effort to help dealers better understand which used vehicles consumers are looking at most each month. S ummer is officially here, gas prices continue to fall and it appears KBB.com shoppers are looking to perform some heavy-duty activities. Commercial or utility-oriented vehicles make up the top five segments with the greatest change in traffic share on KBB.com. The van segment, containing mostly commercial vans, has had the greatest change in share, jumping 13.2 percent month-over-month. Following the van segment is the full-size pickup segment, which has increased 9 percent during the last month. Highlighting this shopping trend is the heavy-duty 2008 Chevrolet Silverado. However, Chevrolet is not the only American brand to see a lift in its used-truck shopping activity, as Ford and Ram also had models with substantial increases. Leading the recreational utility charge is the full-size sport utility segment, driven by increased interest in the 2008 Chevrolet Tahoe. Gaining 24.1 percent in share, the Tahoe is the sole representative of full-size sport utility vehicles in the top 10 model gainers. Based on current economic and shopping trends, dealerships that focus on commercial vehicles could experience an increase in foot traffic in the coming weeks. Also, those dealerships that have a backlog of large utility vehicles can look forward to an opportunity to shed some inventory. Monthly Used-Car Shopping Activity Growth Top/Bottom 10 Models Monthly Used-Car Shopping Activity Growth Segments 2008 CHEVROLET SILVERADO 2500/3500 HD 25.6% Van 2008 CHEVROLET TAHOE 24.1% Full-Size Sport Utility 22.8% Full-Size Pickup Truck 2006 ACURA MDX 18.5% 2006 RAM DAKOTA 2008 FORD F250/F350/F450 SUPER DUTY 2006 NISSAN ALTIMA 2006 MAZDA MAZDA3 15.6% Mid-Size Pickup Truck Minivan 11.9% Luxury Sport Utility 7.1% 2006 CHEVROLET SILVERADO 1500 7.0% 6.4% 2006 VOLKSWAGEN JETTA -8.5% 2009 HONDA CIVIC 2009 BMW 3 SERIES -16.5% 2010 LEXUS RX -17.2% -17.6% 2009 VOLKSWAGEN JETTA -20.9% 2009 HONDA PILOT -23.0% 2009 AUDI A4 -27.8% 2010 LEXUS IS -28.7% 2010 BMW 5 SERIES -33.0% 2009 BMW 5 SERIES -35.2% 2009 VOLKSWAGEN CC -100% -50% 0% 50% 100% % Change in Share Month-Over-Month Information based on 2010 to 2006 model-year vehicles 9.0% Mid-Size Sport Utility 13.4% 2006 RAM 1500 13.2% 9.0% 7.5% 6.2% 3.0% 2.7% Full-Size Car 1.9% Compact Crossover 0.6% Sports Car 0.5% Mid-Size Crossover 0.3% Mid-Size Car 0.1% Subcompact Car -1.3% High Performance -1.7% Compact Car -2.5% Full-Size Crossover -2.6% Premium Luxury Car -6.7% Entry Luxury Car -7.7% Luxury Crossover -9.9% Compact Luxury Car -9.9% Premium Sports Car -10.5% Luxury Car -12.1% -13.5% Hybrid Car -30% -20% -10% 0% 10% 20% 30% % Change in Share Month-Over-Month Information based on 2010 to 2006 model-year vehicles About Kelley Blue Book (www.kbb.com) Founded in 1926, Kelley Blue Book, The Trusted Resource®, is the only vehicle valuation and information source trusted and relied upon by both consumers and the industry. Each week the company provides the most market-reflective values in the industry on its top-rated website www.kbb.com, including its famous Blue Book® Trade-In and Suggested Retail Values and Fair Purchase Price, which reports what others are paying for new cars this week. The company also provides vehicle pricing and values through various products and services available to car dealers, auto manufacturers, finance and insurance companies as well as governmental agencies. KBB.com provides consumer pricing and information on cars for sale, minivans, pickup trucks, sedan, hybrids, electric cars, and SUVs. Kelley Blue Book’s KBB.com ranked highest in its category for brand equity and was named Online Auto Shopping Brand of the Year by the 2012 Harris Poll EquiTrend® study. Kelley Blue Book Co. Inc. is a wholly owned subsidiary of AutoTrader.com 7 BLUE BOOK Market Report JULY 2012

© Copyright 2026